Gas prices are due to become a headwind for gaming markets all over the country, having been a massive tailwind for much of the past year. Some markets will be hit much harder than others.

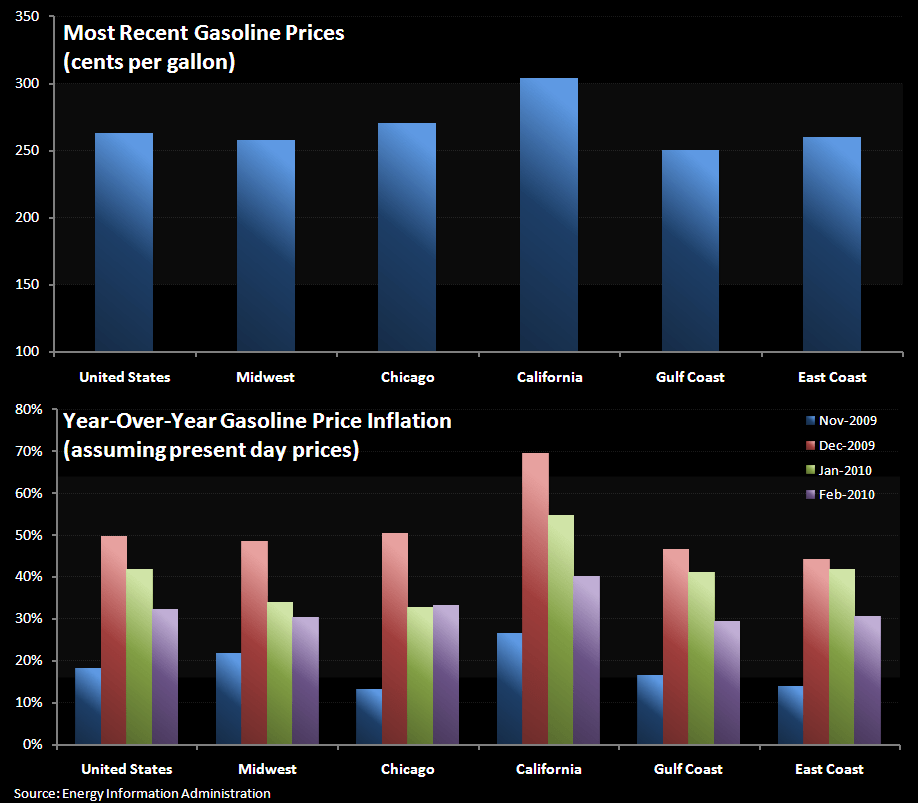

We’ve proven that gasoline prices are a statistically significant variable in driving gaming revenues. While the coming surge in year-over-year gas prices will negatively impact gaming markets around the United States, some markets are worse off than others. The chart below illustrates the spread between the respective areas and the national average price of gas. The most notable outlier is California and it’s big.

If current gas prices stay constant, California will be hit far harder by the year-over-year growth in prices than other areas of the country. As the second chart (below) demonstrates, December would bring a 70% y-o-y hike in gas prices in that state. Gas prices are highly significant in influencing consumer behavior. California has its own tribal casinos which will no doubt be impacted. California also provided 28% of the visitation to Las Vegas in 2008, with Southern California being the origin of 24% of visitors in the same period. Despite the economy, car traffic from California has been positive every month since March due in part to huge YoY declines in gas prices.

It is clear that all gaming markets in the United States will be hit by the effects of the gas price inflation in the back end of this year and the beginning of next year. The East Coast and Gulf Coast markets will have more moderate increases in the price of gasoline, but the increases of 47% and 44% respectively are certainly not to be dismissed.

On a relative basis, Las Vegas’ auto-traffic should suffer more than other gaming markets. Even given the steep sequential drop off in the monthly year-over-year increases in gas prices, the increase in California’s February gasoline prices will still be almost an average of 10% higher than the other markets depicted in the chart above.