COMPANY HIGHLIGHTS

To see our note Retail – Our 2015 Quarterly Playbook please CLICK HERE

KSS - Kohl’s Delivers New Active and Wellness Solutions to Families Nationwide

(http://phx.corporate-ir.net/phoenix.zhtml?c=60706&p=irol-newsArticle&ID=2030859)

Takeaway: KSS put out a fancy press release this morning outlining its new health and fitness initiatives. Most of which the company has been talking about for some time. But, let's keep the new launches in perspective. KSS, like most retailers, adds new brands to its arsenal every year, and it cycles out the unproductive ones. The brands associated with this year's fitness flavor -- Nike, Adidas, Asics -- are much more likely traffic drivers, but they are also brands KSS has carried for years. Yes, the floor allocations will probably march higher as KSS tries to catch up to the competition in its athletic/sportswear offering. But, we think it's important to remember that a) these national brands come in at a lower gross margin, and b) as e-comm becomes a bigger part of the puzzle the need to compete on price and or shipping $ becomes even more important.

WMT, TGT, AMZN - Wal-Mart Canada to drop unlimited free shipping as competition eases

Takeaway: 1) This is genius. WMT moved to free shipping in 2013 to compete with the TGT openings in Canada. Now as Target is set to close its final doors in Canada, WMT hikes rates back up because it can. It's what everyone fears (I guess 'everyone' here would refer to regulators) AMZN will do in the US. 2) This is an interesting case study for US retail where the gamesmanship online is just heating up. AMZN has forever set the pace for the industry when it comes to shipping hurdles, but TGT made a market share place by dropping it's free shipping from $50 to $25 earlier this year. We expect more retailers to use this an offensive weapon, forcing the rest of the industry into free shipping and returns all day every day. The interim move to Free Shipping should be felt by the retailers in 2H15.

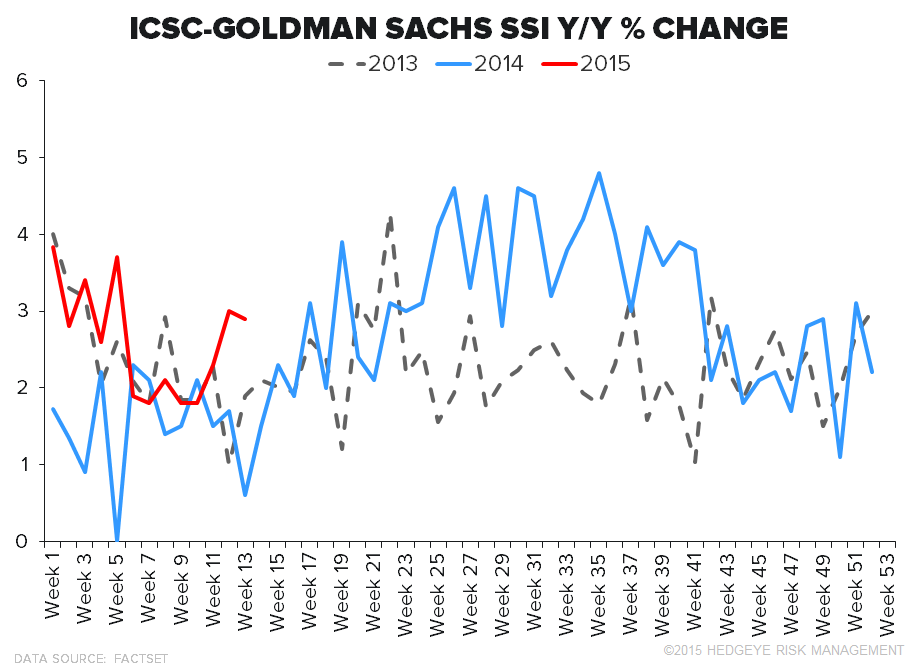

WEEKLY RETAIL SALES (ICSC -- 80 General Merchandise Stores)

Takeaway: Today we're looking at about 3% growth -- on top of a very easy (sub 1%) week last year. The important takeaway is that as March comes to a close, sales comps for the rest of the year get very difficult. Heading into 2Q, growth normalizes – this should be the most ‘normal’ of all the quarters through the year. If you want to see what a company like KSS, M or RL is really capable of, this should be it (we can’t wait). It should also be a quarter where reported earnings growth decelerates by at least 500bp to the high single digits.

OTHER NEWS

ICON - Iconix CFO Resignation

(http://www.sec.gov/Archives/edgar/data/857737/000119312515112037/d898611d8k.htm)

KER - Puma and FIGC Sign New Deal

(http://wwd.com/business-news/marketing-promotion/puma-figc-sign-new-deal-10104860/)

WMT - Wal-Mart Hits Back in Converse Case

(http://wwd.com/business-news/legal/wal-mart-hits-back-in-converse-case-10104330/)

GPS - Banana Republic Unveils New-Look Flagship

(http://wwd.com/retail-news/specialty-stores/banana-republic-unveils-new-look-flagship-10102865/)