“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to heaven, we were all going direct the other way - in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.” –Charles Dickens, A Tale of Two Cities

Despite being a knucklehead hockey player, I have found time over the years to read a few classics, and Charles Dickens’ A Tale of Two Cities is one of them. The longish quote above is, of course, the well known first paragraph of this book. The book was set in Paris and London during and before the French revolution and would go on to become the most printed original English book with over 200 million copies.

I won’t endeavor to make too many parallels between investing, and Dickens’ classic, but I do think the opening paragraph is an apt description for what we have seen in the oil and U.S. dollar markets in the year-to-date. For oil bulls, it has been the best of times, while for U.S. dollar bulls it has been the worst of times.

Our Lead Desk Analyst, Andrew Barber, prepared the chart below, which outlines the performance of oil, the U.S. dollar index, and the U.S. dollar versus the Canadian dollar over the past three years. We referenced the chart at 100 to start and then graphed the performance of all three over the past three years. Not surprisingly, the peak of oil last summer coincided with the trough of both the U.S. dollar index and the strength of the Canadian dollar versus the U.S. dollar. This is a theme that we have been harping on consistently all year, but was really set in motion in 2008 with the meteoric rise, and then crash of oil.

Interestingly, both the U.S. dollar index and the Canadian and U.S. Dollar exchange rate are once again near the extremes of last summer when the oil hit its all time highs. In fact, on a weekly basis the U.S. dollar index is 87.73 as of Oct. 20th and the Canadian Dollar to U.S. Dollar ratio is 91.687 as of Oct. 20th. These are close to the all time lows for both ratios, which imply a weak dollar. In fact, when oil peaked in July of 2008, the U.S. dollar on both ratios was at very close to the same place. Oil, on the other hand, was north of $140 per barrel versus its current price of just under $80.

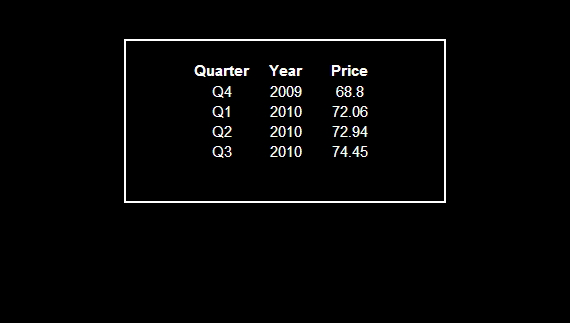

In our Oil Black Book from September, we cautioned about using expert projections for Oil, as collectively they tend to converge around the current month price and project that forward based on recent price action. The consensus projections for the spot price of crude oil in early September were:

Obviously based on where we are today, those price targets seem way off. And likely they will be adjusted upwards if they haven’t been already. Now the point is not to highlight that 35+ experts in aggregate were way off (although that is important to remember), but rather just to emphasize that consensus itself can be way off, and in a much shorter period of time than anyone could have imagined.

A question we often get is whether the U.S. dollar is a consensus short. While its weakness may be well known and the reasons for that weakness as well, the question remains, even if consensus is bearish, is it bearish enough? While we have shorted oil recently and are currently off sides, our longer term view is that oil price has an upwards and to the right trajectory, primarily for supply reasons.

When I look at the U.S. dollar market and oil market over the last three years, I am certain of one thing, they will move together and the move will be on a larger scale than anyone expects. So, if your thesis is that oil will retest its July 2008 highs in the coming months, a primary factor will be the U.S. dollar and in the scenario of parabolic oil prices, no one is currently bearish enough on the U.S. dollar.

Daryl G. Jones

Managing Director