This note was originally published at 8am on March 17, 2015 for Hedgeye subscribers.

“The problem was sight.”

-Peter Zeihan

That quote is not alluding to the Fed’s decision tomorrow. Peter Zeihan was describing what I am sure all of your FOMC day previews are writing about this morning - 14th century macro strategy.

“In the world before 1400, true ocean transport was a rare thing, being neither quick nor reliable nor safe… once line of sight to the land was lost, you had to more or less guess.” (The Accidental Superpower, pg 24)

Guess? When I was first hired on the buy-side, sometimes I’d guess. Then I’d lose lots of other people’s money and my boss, Jon Dawson, would tell me not to guess. “We don’t do open-the-envelope investing.” It was a great risk management lesson.

And it’s one that has stuck with me for the 14 years since he taught it to me. That’s why I’ve been taking down my asset allocation to long-term Treasuries on the recent bounce. I can’t guess what Yellen says tomorrow. I’d rather raise cash and react to it.

Back to the Global Macro Grind…

This is not to suggest that what super “smart” people on the Wall Street refer to as an ‘educated guess’ can’t make you a lot of money. As I implied in my intro, the smartest of those types have figured out to bet big with other people’s money!

Will Janet Yellen remove the word “patient” from tomorrow’s Fed policy language? Will she replace it with another scrabble word score? Will she leave the word in there and be “data dependent”? Will a ramping US Dollar find its way into the language? How about the dirtiest word she’s ever whispered publicly, #deflation?

You can buy-pass the whole seeing thing if you just have answers to the aforementioned questions in advance. It’s called inside information. Some pay a lot of dough for it! If you’re a little Mucker in Stamford, CT – you’re going to have to wait and watch.

Sorry.

Since we said buy both stocks and bonds before they started bouncing last week, now we can sell some of what we bought, raise some cash, and sleep soundly. Chasing beta by levering up your bets after markets bounce is no way to live.

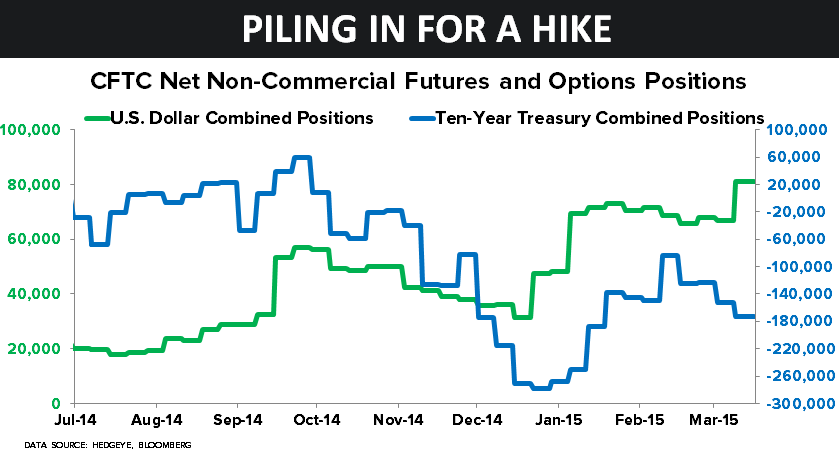

Bets? Yes, people in this profession bet. Before yesterday’s US stock and bond market ramp, here’s where consensus macro bets were leaning, from CFTC Non-Commercial futures and options perspective:

- SP500 (Index + Emini) net SHORT position hit a YTD high of -39,891 contracts

- Russell 2000 net SHORT position hit a YTD high of -40,793 contracts

- Long-bond Bears ramped the net SHORT position in the 10yr Treasury to -173,194 contracts

- Crude Oil Bulls remained pervasive with a net LONG position of +294,609 contracts

- US Dollar Bulls hit YTD highs at +81,210 NET long contracts

And, guess what? Every single one of those Consensus Macro positions was wrong on the day:

- After 3 straight down weeks (yes people get bearish after corrections), SP500 popped +1.35%

- Russell 2000, which has been our favorite of the US major indexes, tested an all-time high

- 10yr UST Treasury Yield dropped to 2.07% (TLT was up +1% on the open)

- Oil continued to crash with WTI closing -2.3% on the day at -17.7% YTD

- US Dollar Index had one of its biggest down days of 2015, -0.76%

“So”, what does this mean?

- You should pay attention to modern day mind-maps like futures and options positioning

- Wall Street is begging for Janet to devalue Dollars and keep rates lower for longer

- If Yellen delivers #dovish tomorrow, you’ll see a lot more of Consensus Macro bets being wrong

I personally don’t like being wrong. That’s why, especially heading into an open-the-envelope event day like tomorrow, I lower the probability of being wrong by raising cash.

Do I have an opinion on what the Fed should do? Of course. But that and a bus ticket will get me a swift beating at a men’s league hockey game in northern Quebec. What the Fed should and could do are two very different things.

Since we’ve had a good run here in March, I’d rather cling to my cash (US Dollars) than pretend to see something I have absolutely no edge on. And I’ll let the clairvoyant vision of the Federal Reserve rule another non-free-market day.

Today we’ll be hosting a Macro Call on the US Employment Cycle at 11AM EST (ping sales@Hedgeye.com for access). Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.01-2.14%

SPX 2053-2112

RUT 1222-1243

VIX 13.72-17.39

USD 98.50-101.17

Oil (WTI) 43.05-47.36

Gold 1131-1169

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer