We re-shorted the US Dollar via the UUP etf again yesterday. The most asked question in my inbox was “isn’t that consensus?”

I don’t mean to demean the question. At this stage of the Burning Buck game, it’s the only one to answer. At the same time, you have to ask yourself if asking about consensus, is consensus?

After making enough mistakes (with real ammo) trading markets, I have come to conclude that you can either be Bullish, Bearish, or Not Enough of one of those two things. When it comes to the Burning Buck, I shorted it’s strength yesterday because I don’t think the newly awakened US Dollar Bears are Bearish Enough.

To be truly Bearish Enough requires some reading beyond your latest tweet. You can listen to the Johnny-Come-Latelys on CNBC, who are now running segments with lead-ins like “When Nixon abandoned the Gold Standard in 1971” (sound familiar?) to truly appreciate that consensus still has no idea how to analyze this fundamentally.

Niall Ferguson at Harvard is who I would call Bearish Enough. He’s looking for a -20% drop in the price of the US Dollar (FROM HERE) in the next 6-12 months. That would put the US Dollar index at $60!

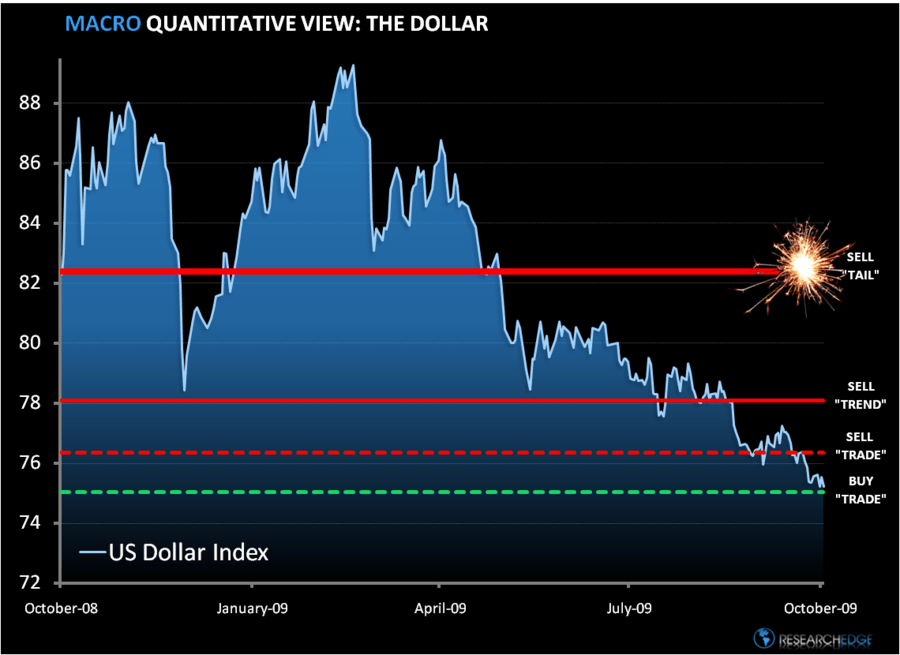

Required reading from Fergusson would be his book titled the Ascent of Money. This fantastic economic history read was all part of the studying we did to make this Burning Buck call 9 months ago, but that doesn’t matter anymore. What matters is the here and now. Now all that matters are my risk management levels. I have outlined them in the chart below. The US Dollar remains in what we call a Bearish Formation.

The Buck is Burning to lower-lows again today (down another -0.5% to $75.19). Alongside that, the SP500 is chasing to higher-highs.

Questions about consensus, can also be consensus…

KM

Keith R. McCullough

Chief Executive Officer