Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

The risk environment looks much the same as last week with intermediate measures in our heatmap slightly more negative. In Europe, even with Greece sending its draft of economic overhauls to creditors, the process has been so dragged out that investors' concerns and uncertainty remain heightened.

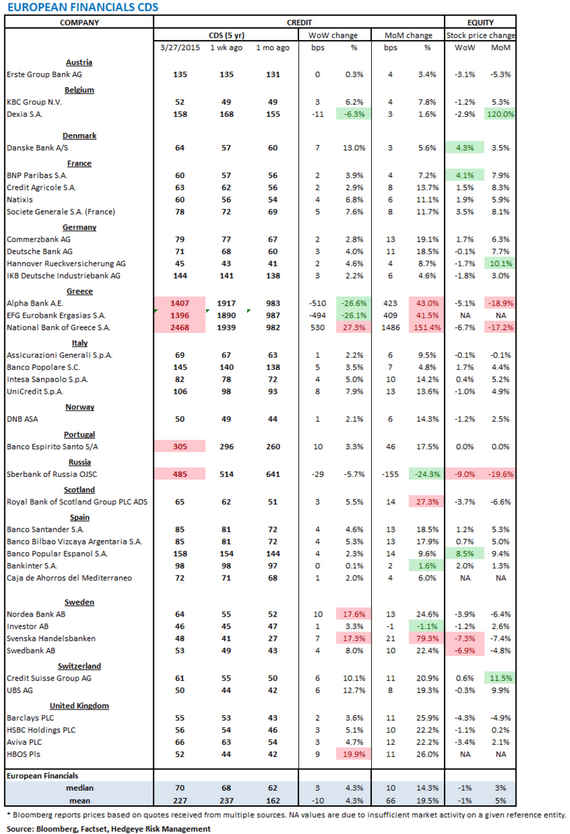

European Financial CDS - Swaps mostly widened in Europe last week. Greek bank swaps are putting up diverging performance, but the main takeaway for Greece is continued uncertainty. Even with Greece sending a draft list of its economic overhauls to its creditors, this progress was delayed by contentious discussions between Greece and EU finance ministers. Given how discussions have gone so far, investors rightfully see a smooth process going forward as unlikely. Separately, Russia's Sberbank saw further tightening as its swaps retreated -29 bps to 485 bps.

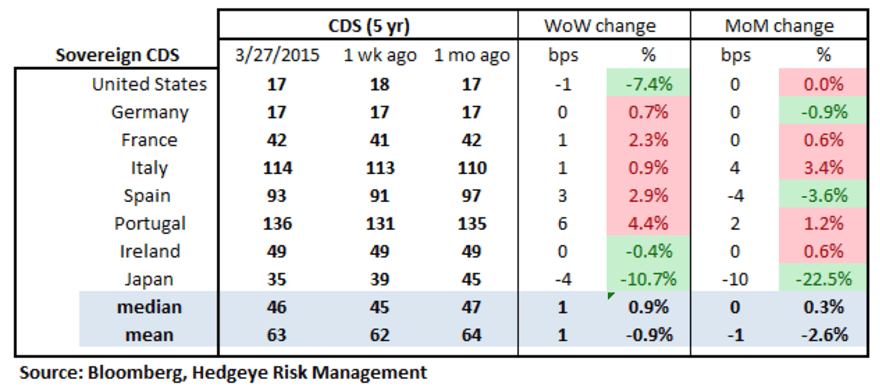

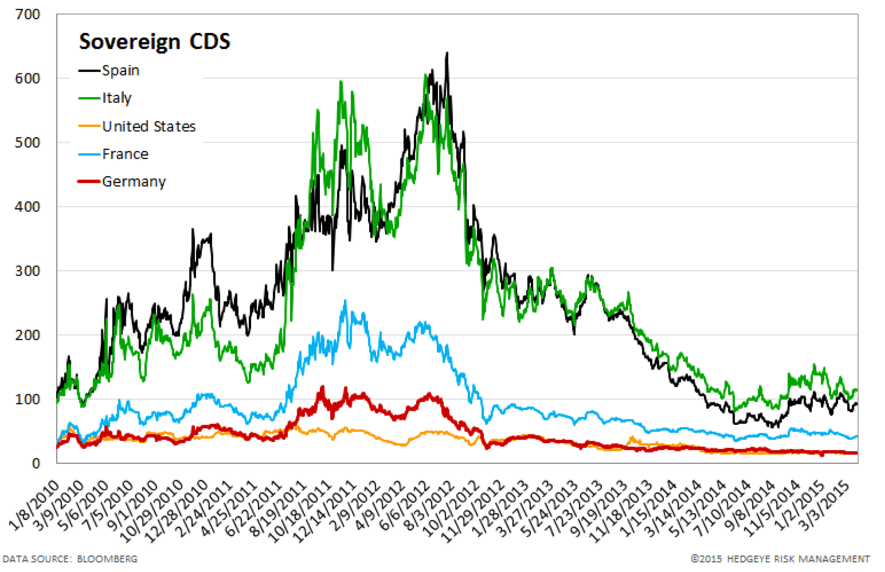

Sovereign CDS – It was a fairly quiet week for developed market sovereign swaps, which widened modestly vs last week. Portuguese sovereign swaps widened by +6 bps to 136, while Spanish swaps widened +3 bps to 93 bps.

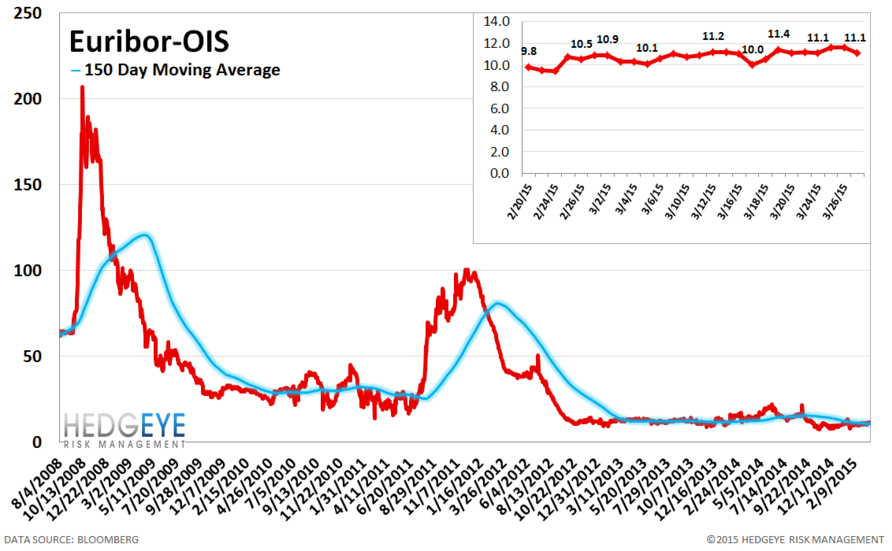

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 11 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst