Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note we added GS, EDV and UUP this week.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

GS

We added Goldman Sachs to Investing Ideas this week.

This new position is a profitable way to invest in what will be incremental uncertainty about the U.S. economy and also a more active Federal Reserve into 2016. After six years of releasing credit into the banking system, the U.S. central bank on the margin will be looking for adjust its half decade long policy and slowly be more restrictive in monetary policy. These adjustments will finally spur trading volume in both credit and equities on the biggest trading desks on Wall Street.

The investment banks are a cheaper way to capitalize on this trend versus the more expensive exchange sector. Goldman firstly should put up its first year-over-year gain in Fixed Income trading in 1Q15 since 2009, marking an inflection point in trading activity. In addition, the firm is mentioning incremental dividend and share repurchase activity signaling that it finally has a handle on the new Financial regulatory regime instilled since the Financial Crisis and can again engage in shareholder friendly activities.

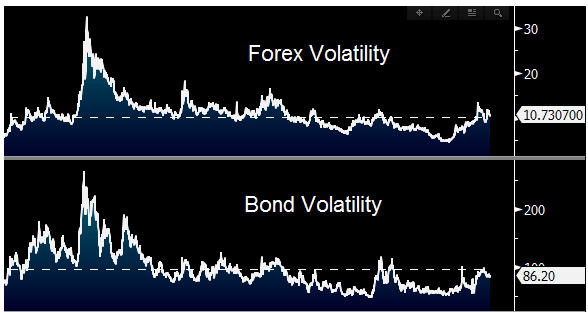

Only equity volatility remains stubbornly suppressed currently with FX, Bond, and Commodity volatility starting to percolate higher which will benefit the Goldman Sach trading desk throughout 2015 and beyond.

ITB

The Thaw

Housing was 3 for 3 in the latest week as Existing Home Sales improved sequentially, New Home Sales saw an epic acceleration and the high frequency purchase application data showed signs of thawing alongside the break in the weather.

To review the data: Sales of Existing Homes, which account for ~90% of the total market, accelerated to +4.7% YoY in February, marking the fastest rate of growth in 17-months. More impressively, New Home Sales (~10% of the market) hit their highest level since February 2008 rising +7.8% MoM to 539K. On a year-over-year basis, sales were up a remarkable +25% and should continue to look strong from a second derivative perspective as we traverse a 5-month period of (very) easy comparisons. Meanwhile, weekly Purchase demand, as measured by the Mortgage Bankers Association, showed some emergent mojo as well, rising +4.9% sequentially and accelerating +200bps to +2.7% on a year-over-year basis.

As we’ve highlighted, we expect a modest backlog of deferred housing consumption in conjunction with healthy organic demand trends to manifest in accelerating improvement in reported activity over the next 6-8 weeks. Indeed, the crux of our underlying thesis remains largely unchanged. Labor market strength + credit box expansion + easy comps should continue to support improving rates of change in housing demand over the intermediate term.

TLT | MUB | UUP | EDV

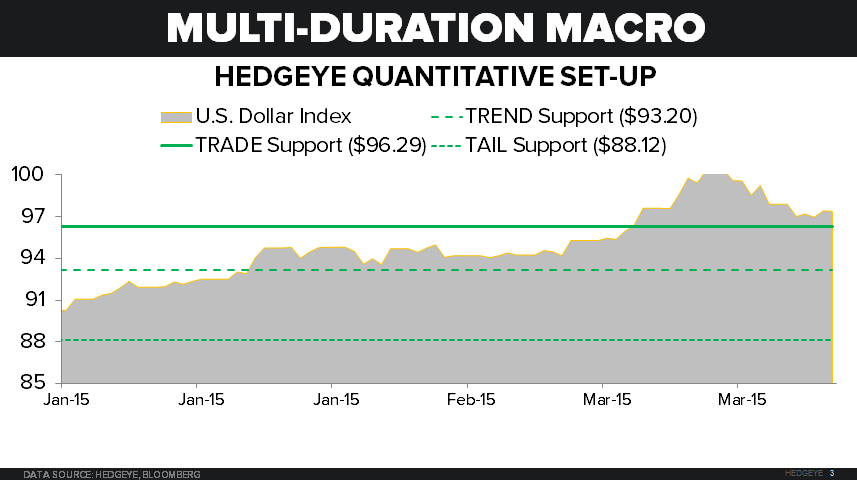

We added the U.S. dollar (UUP) and Long-Duration Treasury Bonds (EDV) this week for two additional vehicles to play growth slowing and deflation over the intermediate to longer-term.

While day-to-day timing isn’t a focus for the longer-term investor, a big counter-TREND move in the U.S. dollar (pullback within a BULLISH TREND set-up) presents a buying opportunity.

After the Federal Reserve revised their growth and inflation expectations downward last week, a short-term rout in the USD has manifested as the market front-runs the currency-devaluing policy effects and discounts the expectation of an interest rate hike near-term.

Most importantly in contextualizing the market’s reaction, all of our key risk-management levels have confirmed our fundamental macro thesis: The dollar has more upside through the back half of this year as deflation remains a global reality moving forward:

- TRADE Support (3 Weeks or Less): $96.29

- TREND Support (3-Months or More): $93.20

- TAIL Support (3-Years or Less): $88.12

The long-end of the bond market has continued to prove its legitimacy as a proxy for forward-looking growth, and forward-looking growth can slow with inflation going both ways….

Look no further than the USD reversal over the last couple of weeks. The reactionary monetary policy from the Fed to “the data” last week succeeded at shifting global currency markets and the yield curve still moved lower. The forward-looking expectation for the dollar can shift, but the bond market continues to tell the same story: lower highs for long duration yields (higher lows for TLT, MUB, and EDV) with more pain for those levered to inflation expectations.

RH

Editor's Note: Shares of Restoration Hardware finished Friday's trading up 4%.

There was no shortage of moving parts in the Restoration Hardware print. Though the after-hours stock reaction immediately suggested otherwise, we think that the story is squarely on track. Actually, we know it is. We’re making slight changes to our quarterly estimates, but are not making any material changes to our annual numbers, which remain materially above consensus.

We would still take advantage of whatever weakness we see. Even though the stock closed up on the day, we’d still buy it here.

We think the road map to a $150 stock at the end of the year is intact.

MTW

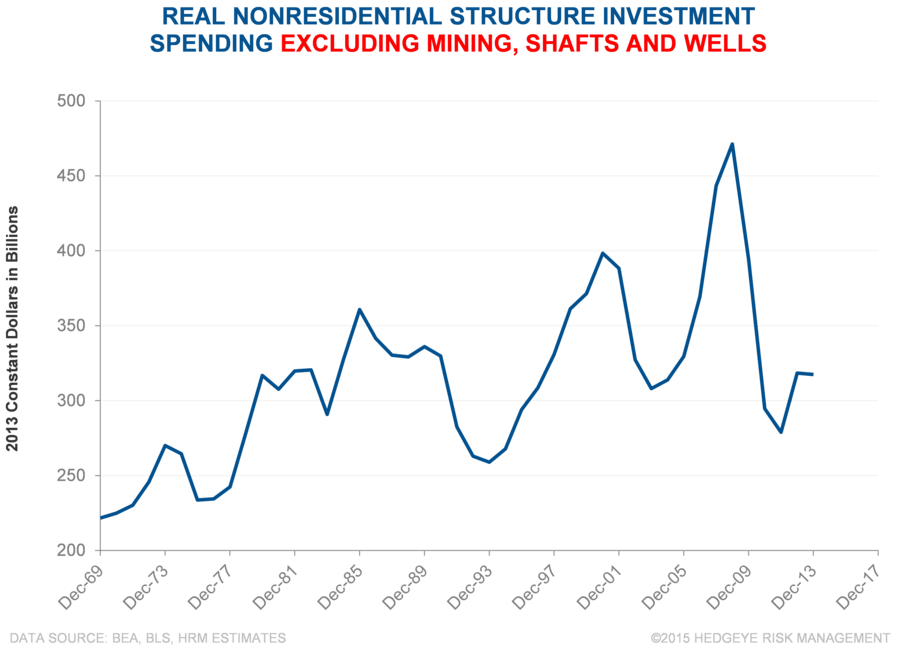

Improving public and residential construction activity amid continued private nonresidential construction spending growth has helped push the Dodge Index back toward peak 2005-2006 levels, while touching its highest growth rate since 1983.

It is worth noting that real nonresidential spending, excluding mining, oil & gas, has performed very poorly since the financial crisis, but still retains its cyclical rebound potential. So. as the Dodge Index and other construction indicators show signs of life, Manitowoc should receive a helpful tailwind.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

china economic update: will the "beijing put" be enough to offset the slowdown?

Our updated, detailed thoughts on the Chinese economy and its financial markets.

just charts: commodity unwind vs construction

Improving public and residential construction activity amid continued private nonresidential construction spending growth has helped to push the Dodge Index back toward peak 2005-2006 levels.