This note was originally published at 8am on March 12, 2015 for Hedgeye subscribers.

“You are right not because others agree with you, but because your facts and reasoning are sound.”

-Benjamin Graham

That’s one of the concluding quotes in a great book I’ve been citing for the last few weeks, The Outsiders, by William Thorndike. It comes from the final chapter, “Radical Rationality – The Outsider’s Mindset” (pg 197). I love that mentality.

I also love getting big Macro Themes right. After beating myself up daily in this forum throughout February as inflation was having a counter-TREND bounce, I’m happy that March looks a lot more like January – Global #Deflation continues to dominate.

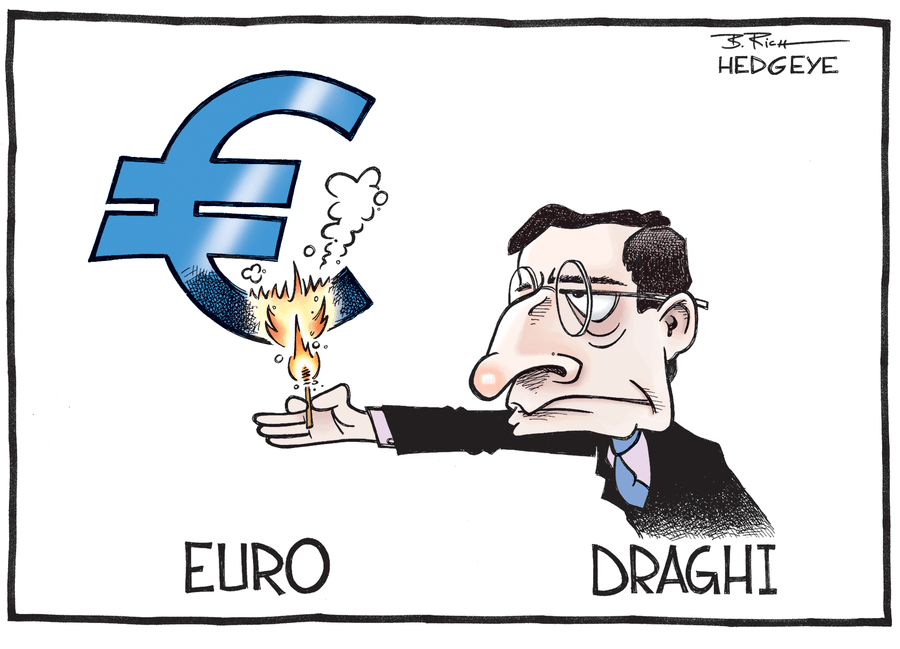

Was our early January reasoning on an intermediate-term TREND target for the Euro of $1.05 sound? Yes. In stark contrast to how many are describing US Dollar strength today, we started with the most basic premise of all – that Draghi would burn the Euro at the stake.

Back to the Global Macro Grind…

Burn baby burn. And now what? Now that they have centrally planned both their stock and bond markets to all-time highs (German DAX +20.2% YTD; German 10yr Bund Yield 0.21%), what’s next?

Our reasoning is mathematical, so bear with me:

1. European growth and inflation data will continue to slow well into Q3…

2. Draghi’s growth and inflation targets will be missed… and… drum-roll…

3. Then he’ll need to provide more #Cowbell, burning the Euro further

That’s been our intermediate-term TREND call. In the very immediate-term (i.e. this morning) the US Dollar is finally signaling overbought at 99.99 on the US Dollar Index (which is what implies our $1.05 EUR/USD target).

Meanwhile, the European “inflation” data remains deflationary:

1. Spain’s Consumer Price Index (CPI) for FEB was still -1.1% year-over-year

2. Germany’s CPI bounced to a whopping +0.1% year-over-year

That’s right. After the counter-TREND bounce in things like commodities in FEB, that’s all the Germans got out of Draghi in reported economic terms, a 0.1% inflation reading which isn’t in the area code of the 2% “target” most central planners are hoping for.

Hope, as we like to say @Hedgeye, is still not a risk management process. And with March’s reversion to the mean of #deflationary forces firmly intact, the Federal Reserve’s hope that #deflation in Oil and Energy markets is “transitory” is going to look wrong (again).

Being right with sound reasoning is one thing. Being wrong, over and over again, on both your growth and inflation forecasts – but representing yourself as right (using stock markets as your validation) is entirely another.

NEWSFLASH: centrally planned stock markets should not be confused with economic realities

That is, of course, how this gigantic and ideological experiment ends. With central planners attempting to bend and twist economic gravity and ending up right where they started – with both Global growth and inflation slowing.

“So”, with European equity and sovereign bond prices pinned up here this should be fun to watch.

It’s also been a hoot to watch the Weimar Nikkei, which took it’s inverse-correlation queue from Burning Yens and ramped another +1.4% overnight (+8.9% YTD) to a 15 year high. Yep, that’s crushing the SP500 (which is -0.9% YTD).

Oh, you don’t like when I contextualize the almighty US stock market that way? You mean you didn’t tell your clients you were buying the living daylights out of failed Abenomics and shorting the US stock market on the other side of that?

What is wrong with you? You definitely don’t deserve 2 and 20 unless you had that reasoning! #kidding

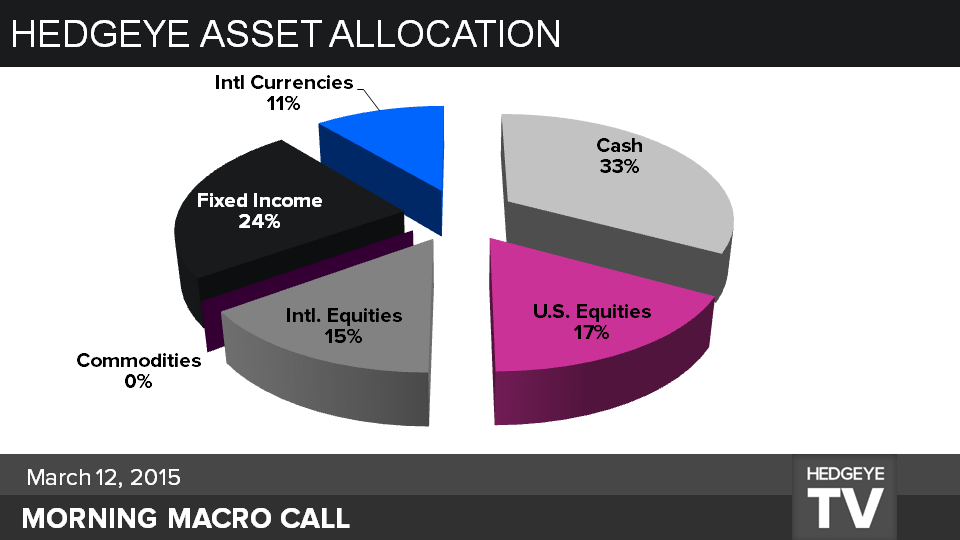

But I’m not kidding in telling you that I have my US equity asset allocation (see our dynamic and daily Hedgeye Asset Allocation model in the bottom of this note for how I’d be allocating capital or raising cash after macro moves) at YTD highs, on red.

From this time and price, I like US Consumer Discretionary (XLY), Housing (ITB), and the Russell 2000 (IWM) – in that order. I also like Healthcare (XLV) stocks, but in looking for a beta bounce on accelerating US consumption (US Retail Sales are going to be reported this morning), I think there’s more upside in the aforementioned order.

If everything that punishes those levered to commodity and/or debt #Deflation doesn’t pay the people in America who have been pulverized by US cost of living, my reasoning will prove to be wrong. Oh, and so will any US GDP forecast that doesn’t look recessionary.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.24%

RUT 1194-1235

Nikkei 18715-19009

USD 96.98-99.99

EUR/USD 1.05-1.08

YEN 119.35-121.91

Oil (WTI) 48.01-50.22

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer