“Why get better when you can simply get bigger?”

-Peter Zeihan

I could go a lot of different ways with that quote, but I’ll stick to Global Macro this morning and go with the wood – America as the world’s superpower!

The aforementioned quote is another beauty from chapter 4, “Enter the Accidental Superpower” (pg 72) where Zeihan reminds us of simple, but very relevant, investment facts:

“From the Louisiana Purchase onward, the Americans have boasted the world’s most capital rich geography… It is the world’s largest agricultural, technological, financial, and based on how you collate the data, industrial power – and has been those things for fifteen decades.”

#timestamped

So why didn’t you think of getting yourself some bigger moneys under management for 0% down and buy some big time American brands like Kraft Foods, for $40 billion US Dollars this morning? Buffett says bigger is better, baby!

Back to the Global Macro Grind…

Maybe I won’t tell you to double down on a broken Old Wall Banker of America (BAC), but I can get you all bulled up on what is made in America and working, big time, in 2015 YTD – Housing and Treasuries!

Long-term Treasuries, that is…

It’s been hard enough to find some sunshine on my face during this Northeastern winter – and God knows this game is hard enough as it is, but on those two longer-term investment fronts, it was a damn good day in the USA yesterday:

- US Home Construction ETF (ITB) was +1.2% to +8.0% YTD

- Long-term Treasury Bonds (TLT) were +1.0% to +5.6% YTD

And that, my “folks” and friends, was fundamentally driven!

- US New Home Sales for FEB smoked the shorts at 539,000 (vs. the 465,000 consensus “estimate”)

- Consumer Price Inflation (CPI) came in at -0.03% year-over-year (despite Oil priced +7-8% higher in FEB vs March)

Does the bullish theme get bigger and better? Sure, why not:

- HOUSING: post the most snow in Boston since 1872, we’re calling for that to thaw this Spring

- RATES: lower-for-longer will remain firmly intact when the March #deflations are reported in April

I know, I know. These are some big calls based on some serious outdoor channel checks. That’s what makes us Canadians who do American macro sound so darn “smart.” #LiveQuotesAndWeather

Oh, and it gets better for the many, even though this is going to start getting painful (again) for the few.

The few that still think they should be overweight levered US Energy and Bank stocks, that is. The rest of us can sip on some all-time highs in American-made growth stocks like Starbucks (SBUX), which is +19.3% YTD, in the meantime.

Yeah, I can get as bullish as the next guy, right before I get run-over. How about you? I love hearing guys talk up their mojo when everything is working for them inasmuch as I enjoy the sweet-sound of spring #crickets, when it is not.

What wasn’t working in America yesterday?

- The poor bastard who is long the Ultra Short 20yr Treasury (TBT) is down -12.1% YTD

- Financial Stocks (XLF) were down more than the “market” (again) yesterday, -0.8% to -1.5% YTD

- Energy Stocks (XLE) were down another -0.7% yesterday to -3.8% YTD

“Poor bastard”? Oh yeah, in coming-to-America-man-with-no-money-terms, I’ve been one of those. Why do you think I have to get up every blessed day at 4:02AM? Being wrong in this business is easier than sleeping in.

America is not a poor country. And now the moneys are falling from centrally-planned-heavens for free. While I can’t reconcile why Swiss 10yr moneys cost -0.12%, why do I need to? Everybody should buy everybody now that global growth is slowing!

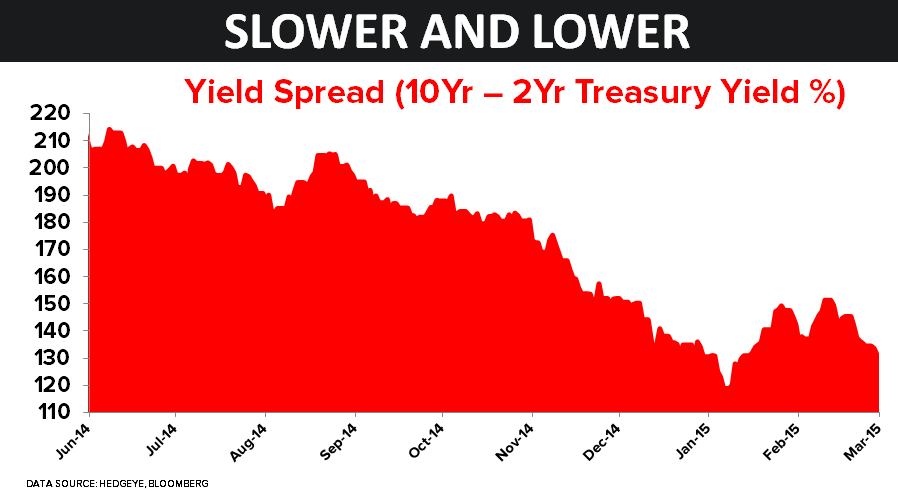

As you can see in the Chart of The Day, one of the great leading indicators that your un-elected Federal Reserve refuses to put on their navel gazing “dashboard” is called the Yield Spread. Leading indicator for the rate of change in US growth, that is…

While we remain bullish on #Quad1 for Q1 of 2015 (our year-over-year GDP forecast is higher than Wall Street’s), we were lower on Q4 and we’re forecasting slower in Q2 and Q3.

With the 10s/2s Yield Spread down to +129 basis points wide this morning, you’ll note that puts it right around its YTD lows (and the Q1 2012 lows). Oh, and Q2 starts 1 week from today – March turning into April is another big time macro call I’m definitely going to make!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.82-1.99%

SPX 2082-2117

RUT 1

VIX 12.79-15.88

USD 96.74-98.98

EUR/USD 1.04-1.10

Oil (WTI) 42.35-48.31

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer