Tickers: MPEL, RHP

EVENTS

- March 26: Macau Legend 4Q conf call 8:30-9:30pm (EST)

- March 27: CCL F1Q, 10am -

COMPANY NEWS

MPEL - CEO Lawrence Ho said in a letter that it would give a 5% salary increase to eligible non-management staff. The letter was published online by the labour activist group Forefront of the Macao Gaming.

The percentage rate mentioned in the memo is in line with awards previously announced by other Macau operators. The first monthly payment of Melco Crown’s increment is to be given in April. It did not specify how many workers were eligible for the salary increase.

Takeaway: Salary increase of 5% is the norm

Aristocrat - Investor Day presentation

Genting - Resorts World LV will break ground on May 5th. The $4 billion project will include 3,000 rooms, a combined 3,500 slots+tables, a 175,000-square-foot casino, and a Chinese theme designed by architect Paul Steelman.

The company still will need to apply for a full gaming license before Resorts World Las Vegas can open. Construction is expected to take place over multiple years and include at least two or three phases.

Genting - Resorts World at Sentosa has executed an agreement for syndicated senior secured credit facilities worth S$2.27 billion. The new facilities will be utilised primarily for refinancing RWS's existing facilities of S$4.1925 billion obtained in 2011. The five-year facilities comprise a S$1.75 billion syndicated term loan facility, a S$500 million syndicated revolving credit facility and S$20 million bank guarantee facility, provided by DBS Bank and OCBC.

In an announcement to the Singapore Exchange, Genting Singapore said the new facilities will enable RWS to extend the tenure of its existing facilities to 2020 and also offer the firm better repayment terms which enhance its balance sheet strength and financial flexibility.

RHP -

- The company has repurchased all of the common stock warrants associated with its previously outstanding 3.75% convertible senior notes, which matured on 1-Oct-14. No warrants remain outstanding following these repurchases.

- The aggregate amount paid to the warrant counterparties in consideration for the repurchase of the remaining 4.7M outstanding common stock warrants during Q1 of 2015 was $154.7M, funded with cash on hand and borrowings under the company’s credit facility.

- Due to the change in the fair value of the warrants between 31-Dec, 2014 and the settlement date, the company expects to record, in its financial statements for the quarter ended 31-Mar-15, an approximate $20M loss on this change in the fair value, which will be included in other gains and losses, net.

Carey Watermark - acquired the landmark Westin Pasadena hotel. The acquisition price was $142.5 million. The full-service hotel includes 350 guestrooms and is located in downtown Pasadena, California.

Takeaway: Average price per key: $407k for this UUP property in a tier 1 market.

INDUSTRY NEWS

Japan- Liberal Democratic Party politician Takeshi Iwaya, a member of a group of pro-casino lawmakers, said they decided to submit the casino bill by next Tuesday, the last day of the fiscal year.

"We have decided to submit it before the end of the fiscal year," Iwaya told reporters, adding that having the bill on the table by March 31 meant local governments considering casino resorts could continue funding research on the topic in the coming year.

Takeaway: Still a long shot

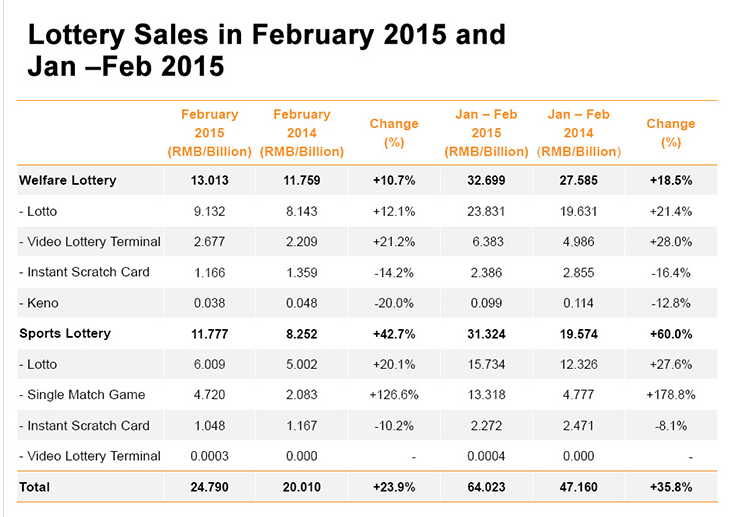

China lottery sales (Feb 2015) - Total lottery sales in February 2015 increased 23.9% YoY to RMB 24.79 billion. Sports lottery sales increased 42.7% YoY to RMB 11.777 billion. However, instant scratch cards fell YoY.

Tunis attack impact - “I think it’s too early to tell,” said Dwain Wall, former general manager of the CruiseOne/Cruises Inc. division of World Travel Holdings and now co-president of YLLY.com, an online travel agency in Beijing. “It hasn’t had any effect on our bookings as of yet. … It’s so hard to tell how consumers are going to respond.”

UK cruising - Kennedy Cree, general manager of Scotia Travel said, " The fall in passengers doesn’t surprise me. The market reached a frenetic peak about two years ago and I didn’t think that would be sustained. There was a huge assumption that first-time cruisers would be cruisers for life, and I’m not sure that’s proved to be the case so far. They still want to go on land-based holidays so are not booking cruises every year." He added that he was unsure how cruise lines would be able to reverse the fall, and said that despite the industry’s best efforts, discounting was still a problem.

“It’s hard to see what cruise lines can do that they aren’t already doing. Prices are good and if they are going up a bit, the lines are including a drinks package or onboard spend so the customer is getting better value. They have done this to discourage discounting but it’s not worked and there’s still discounting across all the star categories. I think the cruise market will start growing again, but just a bit slower than they thought it would.”

Statistics from Clia UK and Ireland show that the number of British travellers taking a river cruise grew by almost 8,000, taking the total number to 139,400 in 2014. Europe remains the most popular region for UK travellers, accounting for 85% of all passengers. In particular, the river Danube’s popularity remained strong, growing 41% while cruises on the Danube and the Rhine grew 37%.

Takeaway: UK pricing is not as robust as before. Cannibalization could be a risk here.

MACRO

Macau CPI - February 2015 increased by 5.30% YoY and 0.90% MoM.

Hedgeye Macro Team remains negative Europe, their bottom-up, qualitative analysis (Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates) = Europe Slowing.

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015.