Recent Notes

03/16/15 SHAK: NYC is Not the Center of the Universe

03/16/15 Monday Mashup

03/17/15 DRI: Expectations of Hope and Change

Events This Week

Monday, March 23rd

- Telsey Advisory Group Spring Consumer Conference: DPZ

Tuesday, March 24th

- Telsey Advisory Group Spring Consumer Conference: DENN

- SONC earnings call 5pm EST

Wednesday, March 25th

- Telsey Advisory Group Spring Consumer Conference: DRI

Thursday, March 26th

- CIBC Retail & Consumer Conference: QSR

- COSI earnings call 5pm EST

Recent News Flow

Monday, March 16th

- RRGB promoted Denny Marie Post to Executive VP and Chief Concept Officer and appointed Lee Dolan Senior VP and Chief Marketing Officer.

- JMBA filed a form 12b-25 to extend the filing date for its 2014 Form 10-K. The company plans to report in this 10-K that, at the end of 2014, material weakness existed in its control over financial reporting due to insufficient finance and accounting resources in the organization.

- BLMN appointed Gregg Scarlett as Executive VP of Bloomin’ Brands and President of Bonefish Grill. Stephen Judge plans to leave the company, after a transition period, to pursue other interests.

Tuesday, March 17th

- BJRI upgraded to outperform at Wedbush Securities with a $63 PT.

Wednesday, March 18th

- SBUX announced that its Board of Directors declared a two-for-one stock split and will begin trading on a split-adjusted basis on April 9, 2015.

- SBUX and Tingyi Holding entered into an agreement to manufacture and expand the distribution of Starbucks ready-to-drink products throughout mainland China.

Friday, March 20th

- TAST initiated buy at Dougherty & Co. with a $10.50 PT.

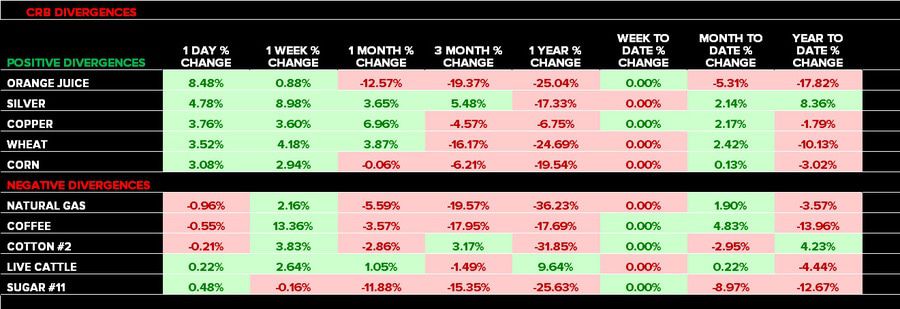

Commodities

Sector Performance

The SPX (+2.7%) outperformed the XLY (+2.1%) last week. Both casual dining stocks and quick service stocks, in aggregate, underperformed the SPX.

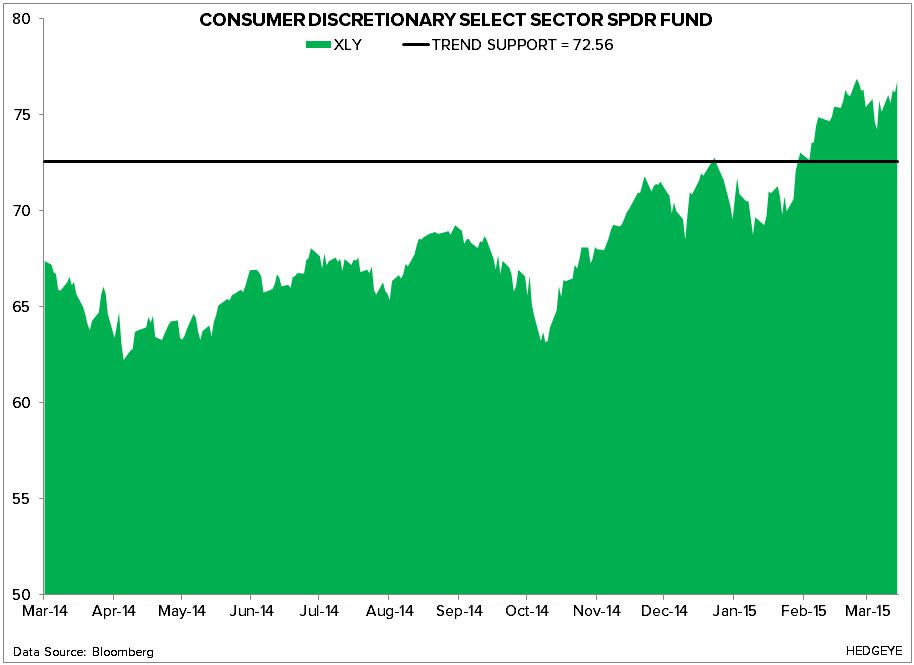

Quantitative Setup

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

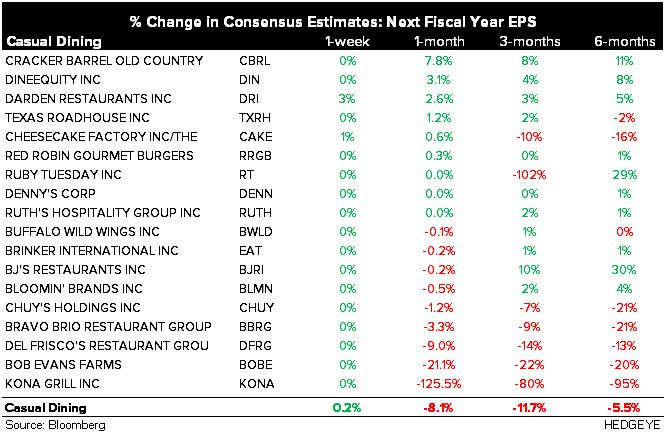

Casual Dining Restaurants

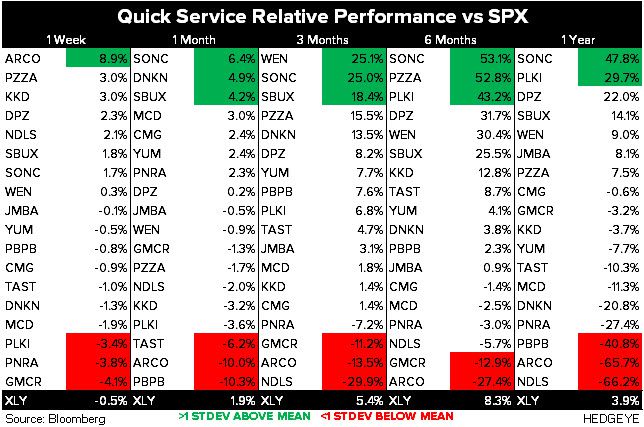

Quick Service Restaurants