KEY POINTS

- WORST CASE SCENARIO? We recently learned of a research report suggesting that P could weather SoundExchange (SX) proposed rates by managing content costs to the 55% revenue floor through a listener cap. The analysis appears encouraging, but it's extremely sensitive to its rather optimistic underlying assumptions (e.g. revenues that are above street estimates). Small variances in either revenue growth or listener hours would be the difference between treading water and insolvency.

- THERE’S NO SILVER BULLET: If SX proposed rates prevail, P would be in a precarious situation. There wouldn't be much room to cut costs since the majority of its costs are tied to content & S&M, and any material cuts to the latter would put its revenues at risk. The only real option is cutting hours, and while a listener cap seems like the natural option, it may not be enough, especially if revenues fall short. We suspect management would take more drastic measures to proactively preserve its cash, potentially exiting unprofitable US markets altogether (both users and its local sales reps).

- WEBCASTER IV = POWDER KEG: If Web IV settles somewhere in the middle, P remains in a precarious setup. P’s prospects would still be tied to its ability to maximize revenue while limiting listener hours, which essentially means taking price and/or increasing per-user ad load (sell-through). The latter may prove more challenging given a growing wave of competitive threats for listener hours. We’re not sure how Web IV unfolds, but ultimately a compromise may not be good enough.

WORST CASE SCENARIO?

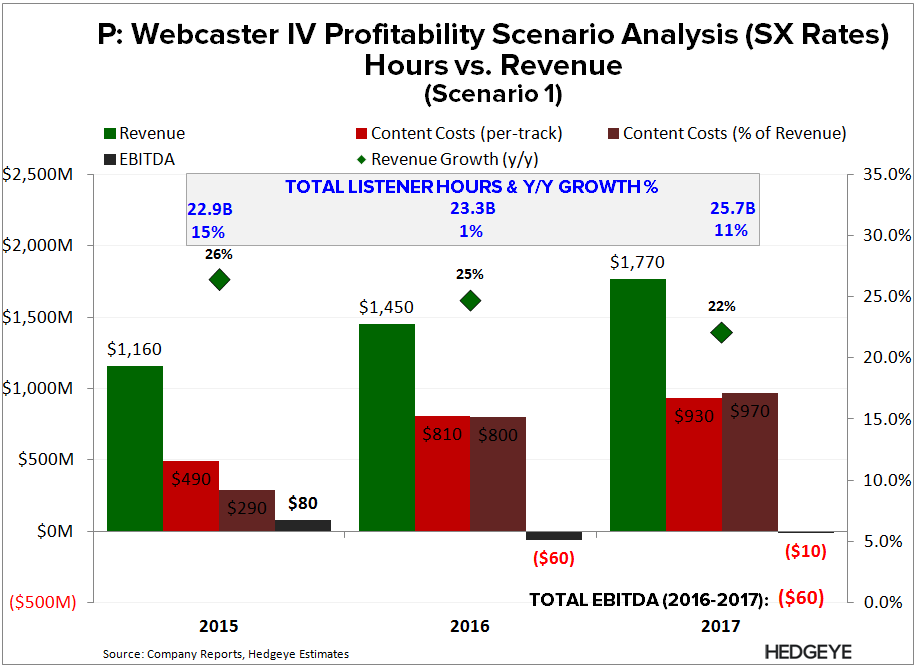

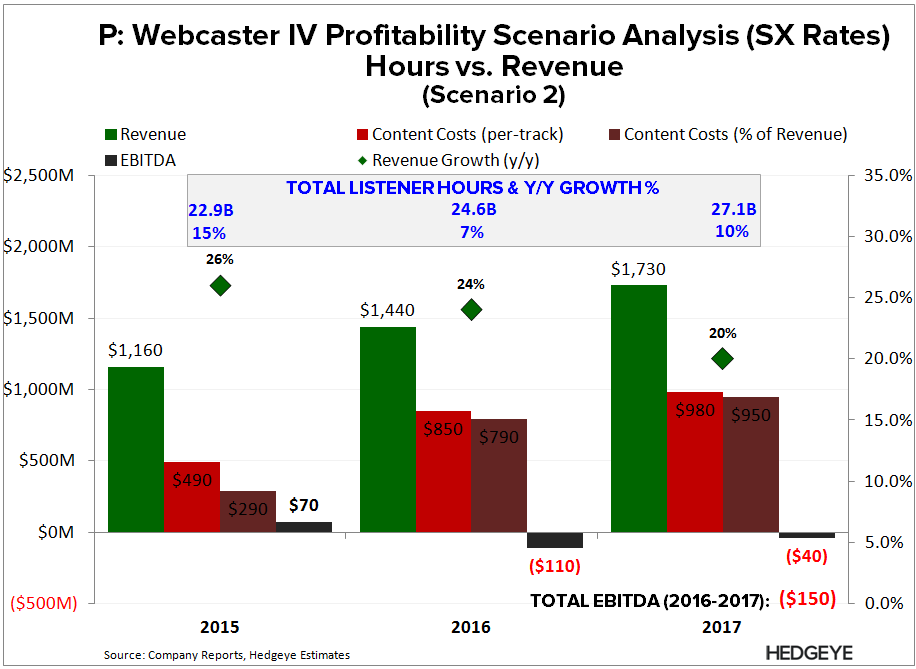

We recently learned of a research report suggesting that P could weather SoundExchange (SX) proposed rates by managing content costs to the 55% revenue floor through a listener cap. While the analysis appears encouraging, it’s extremely sensitive to its underlying assumptions, which are rather optimistic (particularly revenues, which are above street estimates).

The key thing to consider is the trigger. Under SX’s proposal, P will pay the greater of 55% of revenue or the per-track royalty rate. So if revenues are too light, or listener hours are too high, the higher per-track rate would apply. Assuming P could seemingly manage those two dynamics to trigger the 55% floor is not the worst-case scenario under SX’s proposal, it’s the best case.

For example, if revenue growth is off by only 2-3 percentage points and/or the listener cap doesn’t curb usage to the magnitude expected, then the 55% floor wouldn't apply.

Below are a two charts illustrating P’s cash burn under small changes in revenue and listener hour assumptions; the takeaway is that very small changes in either metric paint drastically different pictures, and the underlying assumptions in each are still fairly optimistic.

THERE’S NO SILVER BULLET

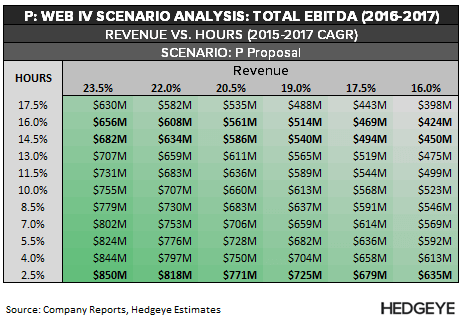

If SX rates prevail, P’s cash flows would become very sensitive to small variances in revenue growth or listener hours. There won’t be much room to cut costs since the majority of which are tied to content, and any material cuts to its next largest line item (sales & marketing) would put its revenues at risk.

The only real option is cutting hours. While a listener cap would be the most likely option, it may not be enough if revenue growth falls short. Below is an scenario analysis for total EBITDA through 2017. We’re flexing revenue and listener hours (both on a 3-yr CAGR) under SX proposed rates. Note consensus is calling for 23.5% revenue CAGR through 2017.

The takeaway from above analysis is that P could face an escalated level of cash burn over, which could ultimately lead to insolvency within 2-3 years. Note that P still isn't generating positive FCF, has only $355 million in cash, with a $60M revolver.

That said, we suspect management would take more drastic measures to proactively preserve its cash if SX rates prevail, regardless of its internal expectations for revenue growth or listener hours. The risk of getting it wrong would be too severe. We suspect that means exiting unprofitable US markets altogether (both users and its local sales reps).

WEBCASTER IV = POWDER KEG

If SX gets there way, P will need to drastically alter its model (see point 2). If P’s proposed rates prevail, P would see a massive reprieve in content costs over the next two years that would drive considerable ramp in cash flow growth.

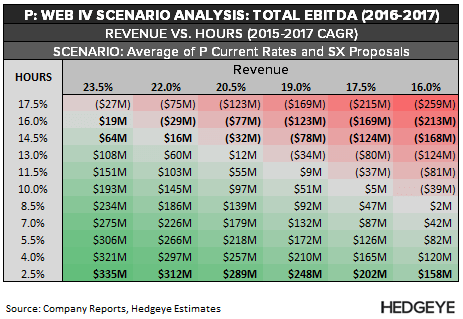

If Web IV settles somewhere in the middle, P still remains in a precarious setup. Below are two additional scenario analyses. The first is the midpoint between the two proposals, the next the midpoint between P's current rates and SX proposed rates. We believe the variance between the two seemingly-similar situations illustrates how sensitive the situation is.

Ultimately, P’s prospects would still be tied to its ability to maximize revenue while limiting listener hours, which essentially means taking price and/or increasing per-user ad load (sell-through). The latter may prove more challenging given a growing wave of competitive threats for listener hours.

We’re not sure how Web IV will unfold, but ultimately a compromise may not be good enough.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet