A Message From Hedgeye CEO Keith McCullough

With the stock market back to its all-time-highs, I’m erring on the side of caution and capital preservation right now. As you know, all-time is a long time, so I think it’s as good a time as any for investors to reduce some of their higher-beta equity exposure.

Since Warren Buffett taught me Rule #1 of Investing (“Don’t Lose Money”), I’ve always had a deep respect for cash, liquidity, and flexibility. There is a time to protect capital so that we can invest in names on the next correction.

In looking at what I call our “bench” of research ideas, we have at least a dozen names on the bench that I will be looking to bring back to Investing Ideas when opportunities (lower prices) present themselves.

Now that the Fed’s decision is out of the way, the best longer-term position to protect against both Global #Deflation and #GrowthSlowing remains Long-term Bonds.

Have a great weekend,

Keith

* * * * * * *

Below are Hedgeye analysts’ latest updates on our five current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*Please note we removed PENN and OC this week.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

ITB

A TALE OF TWO REALITIES

(False) Reality: Monday and Tuesday conjured fears of an organic slowdown in housing activity as Builder Confidence retreated for a 3rd consecutive month in March and New Home Starts in February saw their biggest month-over-month decline since January 2007. We think the underlying reality is more sanguine with the preponderance of the weakness in the reported February data largely attributable to weather.

As it relates to builder confidence, the Current Traffic component of the index led the weakness in the composite reading, which is consistent with a severe weather related drop in the flow of active buyers. The NAHB also cited supply chain concerns, particularly in terms of labor supply. Residential construction employment saw its largest monthly increase in employment in nearly 10 years in January and employment at the industry level continues to run in the high-single digits. There is clearly strong demand for labor in the sector, however, wage growth has yet to really accelerate according to BLS data so it remains equivocal whether rising labor demand is, in fact, driving accelerating builder cost pressure and/or labor supply shortages at the aggregate level. Further, while labor supply constraints may serve as a drag to builder confidence, presumably it is rising demand trends that are driving tighter conditions in the resi employment market. All else equal, we’d view improving demand as a net positive.

On the New Construction side, while the sharp drop in Housing Starts captured most of the headlines, we believe the real story was in the 3% gain in permits. The 57% collapse in starts in the Northeast drove the bulk of the headline decline, again consistent with unusually cold/severe weather weighing on activity. Ever try to dig and pour a foundation in negative degree temperatures. We'd expect to see a big rebound in the next two months in housing starts as the data plays catch-up to the thaw.

Reported Reality: The reported results for 1Q15 out of the Builders LEN and KBH on Thurs/Friday were as auspicious as the Monday/Tuesday data was ominous. Both companies beat sales and earnings estimates while reporting strong pricing and accelerating orders growth. Further, they talked down the weakness in reported Starts in February and guided to incremental margin improvement over the balance of the year with the expectations for continued, ongoing improvement in the demand environment.

We’re not particularly inclined to take management’s word for it, but with the labor market strengthening, the top-down environment inflecting positively alongside marginal credit box expansion we would agree with the positive, intermediate term outlook.

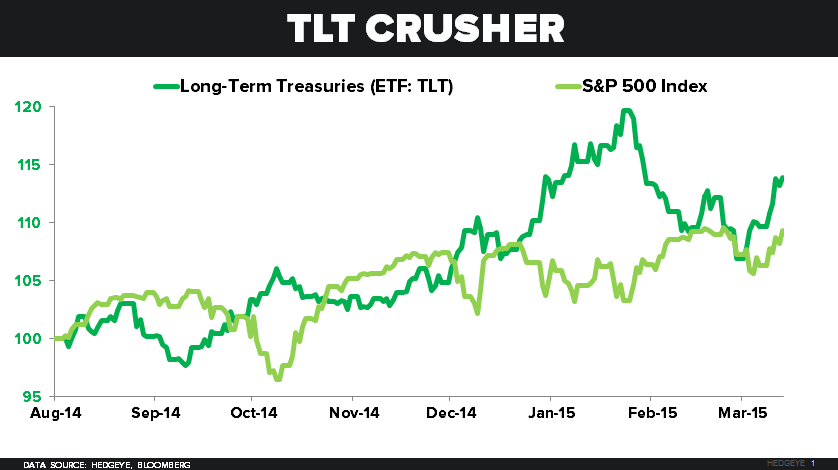

TLT | MUB

Both TLT and MUB continue to grind higher over the intermediate-term, despite some shorter-term pullbacks we’ve seen since adding TLT to Investing Ideas back on August 4th 2014. We have been on the correct side of rates and sitting in TLT has been an alpha-generating trade for the last 6 months.

Scoreboard since August 4th:

- TLT: +15.1%

- S&P 500: +8.7%

Investors who were positioned for a rate hike moving into the biggest macro catalyst of Q1 on Wednesday were caught on the wrong side of the trade. That included a big chunk of consensus macro.

Consensus Positioning:

- Short Treasuries: -173K contracts

- Short RUSSELL 2000: -41K contracts

- Long U.S. Dollars: +81K contracts

- Short S&P 500: -40K contracts (2015 high)

U.S. Treasury 10-YR Positioning:

By the end of the day, we received more confirmation that we want to stick with TLT and MUB.

1) Consensus macro was wrong; 2) growth and inflation are both surprising to the downside; And 3) the Federal Reserve will not be hiking rates anytime soon.

- Lower for Longer: Targeted Fed Funds Rate for December 2015 was reduced to 0.625% vs. 1.125% with the prior forecast

- Growth Slowing: Full-Year 2015 GDP estimate downwardly revised to 2.3-2.7% from 2.6%-3.0%

- Inflation Slowing: Full-Year 2015 range for PCE Inflation downwardly revised to 0.6-0.8% from 1.0-1.6% previously

The U.S. Dollar moved sharply lower, interest rates flattened (TLT UP), equities and commodities both popped. The same story of the market reacting to the relative policy of the Fed will roll-on and as long as consensus macro is positioned on the wrong side of growth and inflation decelerating, we’re sticking with our long TLT and MUB call.

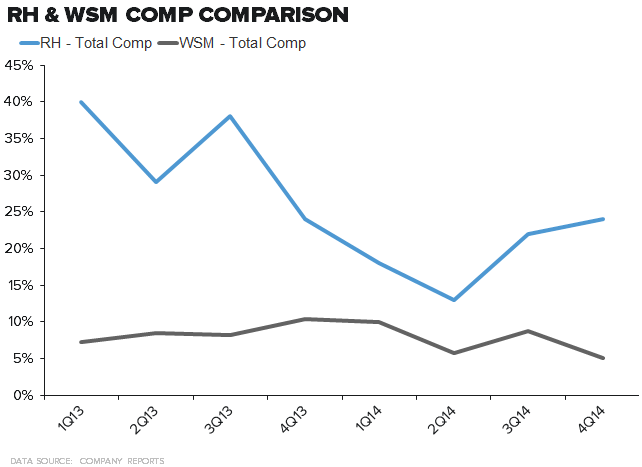

RH

This is pretty much the only WSM chart we really care about.

The 4Q WSM comp was uninspiring at face value at 5.1%, though to be fair the 2-year trends held steady across every concept except for PB Teen (only 6% of rev). But the key for us is that comps trended down for WSM, and trended up for Restoration Hardware (which already preannounced the quarter it will report next week). These two names are often mentioned in the same sentence. But keep in mind that one of them (WSM) grows square footage at 2% on its best day and is comping mid-single digits. The other has square footage growth accelerating to 25% by the end of 2015, and just comped 24% (the second best comp in all of retail behind Kate Spade’s 28%).

WSM took down 1Q guidance, which was almost entirely due to the impact of the West Coast Port issues. The Street will probably look through this, and it should. We certainly will. But the question about the impact on RH from labor issues has already come up in the hours since the WSM call.

Could RH see some impact? Yes. It definitely could, and we expect there to be mention of it on the call. The company is far less mature than WSM and therefore has less experience dealing with issues like this. But keep in mind one important factor…the business that is at risk of being lost forever is what we’d call ‘cash and carry’. That means that the consumer goes into the store, and walks out with the merchandise in their hands. If it’s stuck on a container ship, the consumer is likely walking away empty handed. Consider the following…

1) An apparel company (which is near 100% ‘cash and carry’), that has delayed containers, gets the merchandise several weeks into the season – after the consumer has already made full price purchases. The goods ultimately get sold, but at a deep discount. That’s problematic.

2) By our math, WSM is closer to 30-40% ‘C&C’. Far from optimal, but the nature of its category carries less risk than apparel, footwear, or some other non-durable category.

3) RH, however, has an estimated 5% of its business that walks out of the store with the consumer on the day of purchase. Could some of that be lost? Yes, and some will. But the remainder of the impact should come down to an extension of the time it takes to deliver product. Maybe it takes 12-weeks on a custom order instead of 7-8 weeks, and yes, that could push revenue into 2Q. If anything, this will simply come down to when the revenue is recognized. When all is said and done, we’d argue that RH is structurally more insulated from lost revenue than any other type of retailer. It will probably come down to a matter of timing.

MTW

Recent nonresidential and nonbuilding construction data remains firm for 2015.

The Architecture Billings Index (a survey of architects) typically leads nonresidential and residential construction spending by approximately 9-12 months. More importantly, the ABI Index leads Manitowoc Crane Orders by 2 quarters.

This suggests Manitowoc's crane sales should see a pickup in the first half of the year.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

#emerging outflows round ii march 2015 update

We reiterate our bearish bias on Emerging Markets, a view we have held since late September.

mcd: ripe for a trade on the short side

Consistent with our short thesis, MCD gave an uneventful presentation this morning at the UBS Global Consumer Conference.