“A smile is a curve that sets everything straight.”

-Phyllis Diller

Oh, you’re not smiling this morning? Then you didn’t buy and cover everything within 3-6 minutes of the Fed statement yesterday. Consensus Long Bond Bears were not positioned for that!

Rather than rehash the who said what and when in yesterday’s epic Global Macro move (Dollar Down, Rates Down à Everything Reflation and Yield Chasing Up), here’s the replay of the LIVE coverage I did:

https://app.hedgeye.com/feed_items/43018-replay-fed-coverage-hosted-by-hedgeye-ceo-keith-mccullough

In the spirit of trying to “ESPN Finance” (i.e. provide live coverage and analysis from pros instead of journos), I figured I’d put myself and my analyst, Ben Ryan, to the real-time test. I’m glad we did. Evolving this profession is a big growth opportunity.

Back to the Global Macro Grind…

The thing about ESPN is that they became the world’s curator of what mattered in sports (replays!). After yesterday’s macro market game was played, you know the score – and I highly doubt you want to watch 25 minutes of me analyzing, post game…

So go to minute 13 of that video, and I get to the highlight that mattered most. Apologies in advance for my tone and choice of words – when it’s game time, I care less about style, and more about results.

From an immediate-term perspective, “the call” yesterday was simple – buy everything.

Ok, maybe not everything – in immediately acknowledging the statement as dovish, you obviously wouldn’t have bought the US Dollar or TBT (Ultra Short 20yr Treasury ETF)… but you could have bought damn near anything else!

To review:

- Not only did Janet Yellen NOT make a Policy Mistake (signaling explicit rate hikes)…

- She masterfully pushed out the “dots” on both the timing and pace of hikes (if there will be any at all)

In doing so, she basically crushed whoever was betting on “rate liftoff” and may very well have put the guys who trade on inside information out of business too!

Can you imagine you had what you thought was the river card in hand (that she was going to remove the word “patient”) and put on a massive Long USD, Long Rates position with Utilities and REITS on the short side?

She removed the word alright – and then said “but that doesn’t mean we’ll be impatient.” Ha! Inasmuch as I am no fan of central planning, that was one of the best one-liners of the year. Bravo Janet – and shame on you insider-trading-bro!

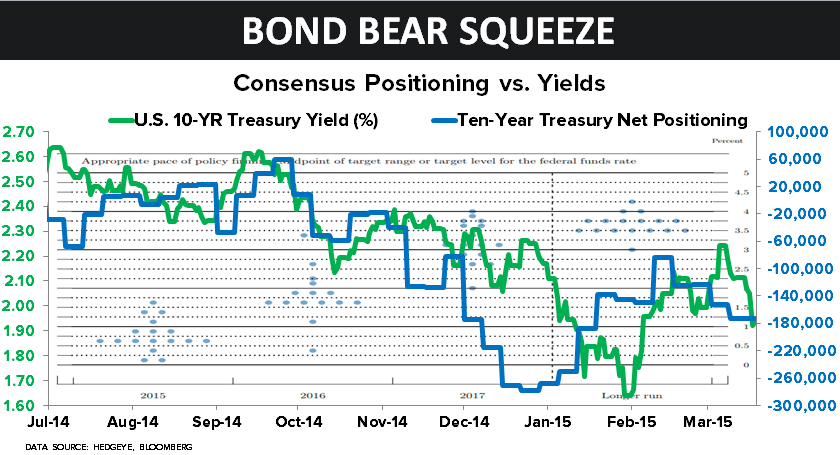

In order to get these big macro moves right, you have to know where consensus is positioned in levered terms (in order to monitor that, we look at CFTC Non-Commercial futures and options positioning):

- US Dollar Bulls hit YTD highs at +81,210 NET long contracts at the beginning of the week

- Euro Bears hit all-time highs with a net SHORT position of -185,661 contracts

- SP500 (Index + Emini) net SHORT position was at YTD high of -39,891 contracts

- Russell 2000 net SHORT position hit a YTD high of -40,793 contracts

- Long-bond Bears ramped the net SHORT position in the 10yr Treasury to -173,194 contracts

Therefore, the call to “buy everything”, in the moment was more like a call to do the opposite of how the crowd was positioned. This job is not easy, but that’s why it was an easy call to make.

Context is the most important thing when making a high conviction “call.” I don’t make them frequently.

Ok ESPN guy - now what?

I’m just going to go back to doing what we always do – executing on our process. While the Fed could have changed everything yesterday, it did not. The USA has another month left in #Quad1, then moves back into #Quad4.

Yellen’s decision keeps our non-consensus view of lower-rates-for-longer on the table (US Treasury 10yr Yield smoked back down to 1.94%, German 10yr Bund Yield at all-time lows of 0.19%, etc.) and she reiterated our #deflation call.

With commodities having crashed again in March (and Oil’s Down Dollar Viagra bounce from yesterday fading, fast), reality is that Janet’s Fed is going to get more, not less, #deflation data when the March data gets reported in April.

As a Long Bond Investor (total Return of TLT up approximately +5% YTD vs SP500 +2%), you can smile this morning. If you’re still long the Russell 2000 (IWM), Healthcare (XLV), Consumer Discretionary (XLV), and Housing (ITB) stocks, you can smile too.

Thanks Janet, for keeping everything less-straight!

Our immediate-term Global Macro Risk Ranges are now (intermediate-term TREND views in brackets):

UST 10yr Yield 1.88-2.05% (bearish)

SPX 2076-2105 (bullish)

RUT 1 (bullish)

DAX 11811-12239 (bullish)

VIX 13.51-16.12 (bullish)

USD 97.39-100.93 (bullish)

EUR/USD 1.04-1.09 (bearish)

Oil (WTI) 41.32-46.34 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer