This note was originally published at 8am on March 04, 2015 for Hedgeye subscribers.

“The best investment you’ll likely ever make is in yourself.”

-Cullen Roche

That’s one of the better quotes from the latest book I am reviewing: Pragmatic Capitalism, by Cullen Roche. While the book has underwhelmed me so far, there’s usually something positive to see in people – if you look hard enough.

This week is a big stressor for me in that we are holding tryouts for our Mid Fairfield and CT Junior Rangers hockey programs. The hardest thing to do isn’t reporting who are the best players on the ice; it’s evaluating which ones have the most potential.

That’s not unlike how I think about investing. Anyone on mainstream TV can tell me what’s worked. What I really need to get right is what’s going to start working next.

Back to the Global Macro Grind…

The biggest risk management question I’m thinking about right now is whether or not the phase transition (from late-cycle bullish at this time last year, to bearish now) of Global #Deflation is going to accelerate to the downside.

If you look one screen past the commodity headlines (Oil and Gold), this is what you were looking at yesterday:

- Orange Juice -7% on the day to -16.9% YTD

- Coffee prices down another -6.6% on the day to -24.2% YTD #crashing

- Hogs (as in pigs) -2.4% on the day to -18.7% YTD

Mortimer! Get me some #deflation in my breakfast already!

Will you see that #deflation on your local diner (or SBUX) menu? Of course not. At least not in real-time. Companies that had food cost accelerating to the all-time highs (2012 was the all-time high for corn prices as Bernanke was devaluing USD) are finally seeing some of those cost pressures alleviate. Local dinner guy’s healthcare and other costs, not so much…

But what about the poor bastard who is selling pigs?

Yes, this whole #deflation thing has winners and losers. #Deflation pays the conservative consumer, whereas it punishes the levered-up debtor whose revenues and cash flows are pinned on higher inflation expectations!

Q: What horse does the Wall Street have in this consumer vs. debtor debate?

A: higher inflation expectations + leverage + banking fees generated by both

In other causal Global #Deflation news, don’t forget that the two most important live quotes on your screen continue to tick this morning. Those are, of course, currency quotes:

- Burning Euros

- Burning Yens

In order to get the rate of change in Global #Deflation right, you need to get the US Dollar right. And… in order to get the US Dollar’s rate of change right, you need to front-run the devaluation policies of its major competing currencies, alright?

- Euros (vs. USD) are being blown up to fresh YTD lows this morning (-7.3% for 2015) at $1.11

- Yens (vs. USD) can’t find a bid after Japan reported the worst Services PMI in the world overnight

Services PMI? Yep. It’s one of the many monthly macro economic data points we pop into the Hedgeye Predictive Tracking Algorithm (the model we built that helps us front run bond yields, central planners, etc.) … and voila, le rate of change appears!

- Japanese Services PMI slowed to 48.5 in FEB vs. 51.3 in JAN

- Italian Services PMI slowed to 50.0 in FEB vs. 51.2 in JAN

- German Services PMI was 54.7 in FEB vs. 55.5 in JAN

“So”, Italian stocks are up on that (German stocks are down) to +15.8% YTD. #lol

It’s funny, sort of, but sad … all at the same time. The worse the Japanese and Southern European economies (i.e. the most levered debtor countries) get, the better their stock markets get, as the entire world front-runs their central planners burning their respective currencies in response.

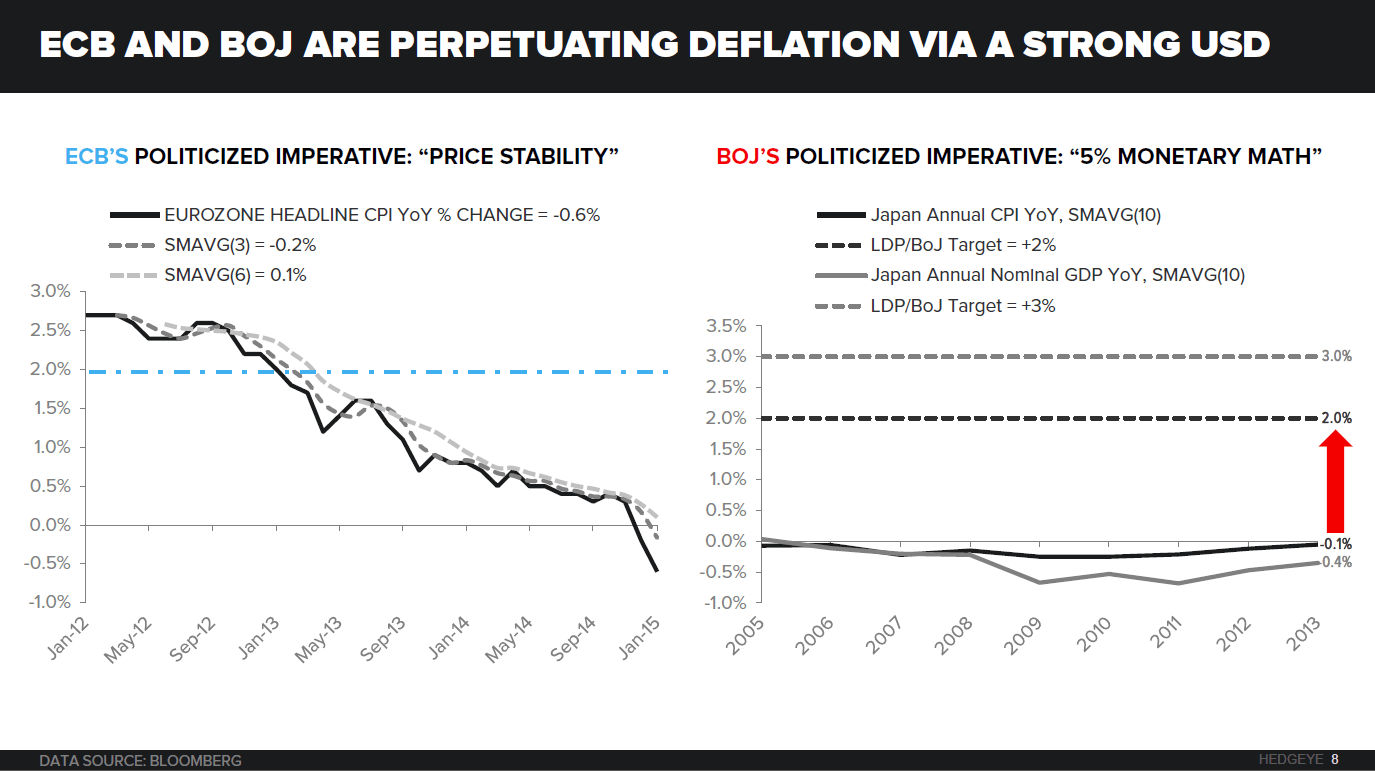

The inverse correlation of burning Euros and Yens to their respective country stock markets is surreal (inverse meaning when FX drops, stocks rip higher). And, as you can see in the Chart of The Day (this is slide 8 in our current Global #Deflation deck), we continue to see it as mathematically impossible that either Draghi or Kuroda will achieve their monetary-math “inflation” targets.

That’s a lot to noodle over as you try to invest in your own noodle. But setting aside what we get right and wrong both in markets and on the ice, that’s the best way to invest in yourself in this good life – to educate yourself empowers your progress and potential.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.88-2.17%

SPX 2083-2121

Nikkei 18601-19005

VIX 13.03-16.33

USD 94.51-95.94

EUR/USD 1.11-1.13

YEN 118.54-120.36

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer