Conclusion: If there is a reason to own FL, we did not find it at the company’s analyst meeting. There were no major changes to the strategy – which we don’t think anyone expected (including us). But there were tweaks that we think make this absolutely uninvestable at $61, except perhaps for a Trade on the near-term extension of strong business trends – a case that can be made for a dozen other zero-square footage growth retailers right now. We’re going to hold off in adding FL to our Best Idea list on the short side until the research on the immediate-term signals us accordingly. But to be clear, if we owned FL we’d sell it immediately.

Here are two points that we found interesting on the margin.

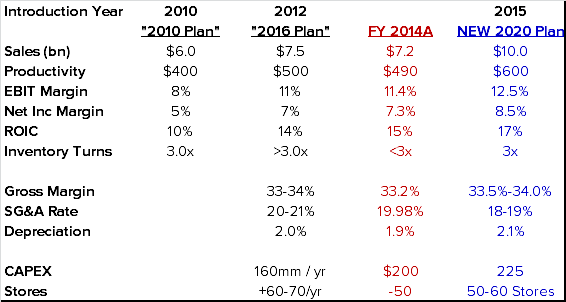

1) New Financial Plan. FL’s prior goals were all about dramatic improvements in productivity and occupancy leverage by way of pulling capital out of the model (closing stores, changing banners, and eliminating working capital). But now FL is guiding to the following…

- Net square footage growth of 2%+ and mid single digit comp growth on top of that.

- Even with an uber-long-term target year of 2020, the goal is only to take Gross Margins 30-80bp above current levels. That’s not even 10bps a year. The point is…gross margins are peak.

SG&A is expected to come down from 19.9% to 18-19%. That’s extremely aggressive. We’ve never seen a retailer sustain a sub-20% level of SG&A – especially not one that will need to spend aggressively on e-commerce, growth in a new concept (six:02), and broaden its international reach. We’ll assume that the company will, in fact, be spending in these areas. But it is banking on a mid-high single digit comp to drive its SG&A ratio lower. We’re not comfortable making that bet.

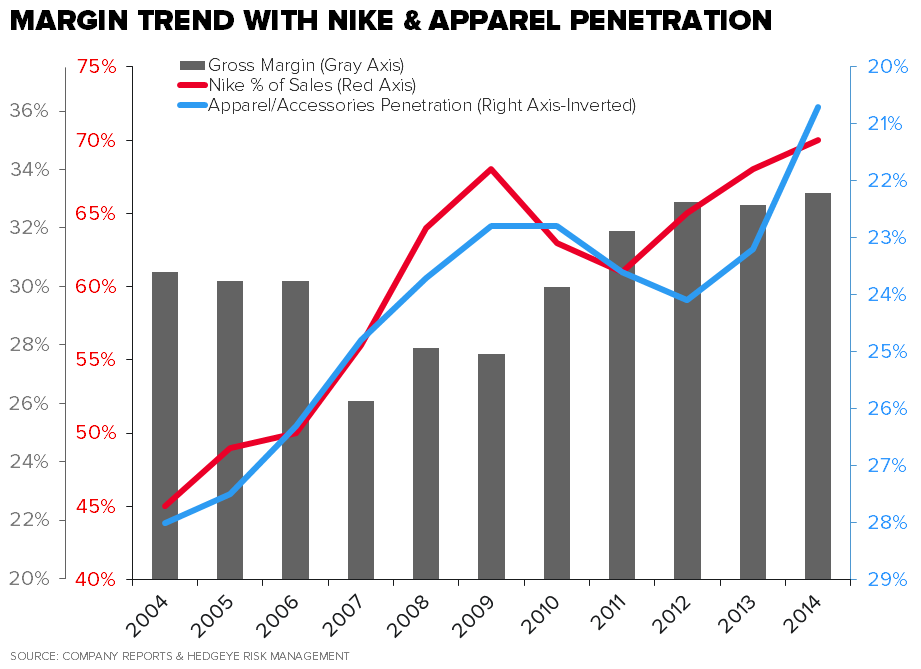

2) Nike + Apparel + Margins. If there was one single chart that we think encapsulates the day, it’s this one.

- FL is making a much more concerted effort in apparel. In fact, the company said that it would like to ‘get back to 2004 levels by 2020’. That means taking apparel from 21% of the mix up to 28% of the mix over that time period.

- What’s interesting is that the same time period that took apparel down to 21% of sales saw Nike’s percent of the business go from 45% to 70%.

- That’s also the same time that gross margins went from trough to peak – swinging from 26% to 33%.

Our point is that Apparel going higher alone presents gross margin pressures, and it’s also a category where Nike is less dominant. So IF FL hits its goal, Nike footwear will naturally become a smaller part of the mix, which is absolutely a negative margin event for FL.

The Bottom Line

FL is healthier company today than it has ever been in the history of the company. Management deserves credit for that. But unfortunately, the low hanging fruit has been picked, and then the ‘tough to reach’ fruit was picked, and now we need to reach for those last few apples on the top of the tree. This might be a healthier company, but there’s almost no room for error, and at this valuation it is a far less defendable stock. IF the company achieves its financial goals, it will be growing EPS in the low double digits, that is a mere quarter of the 45% CAGR it has printed over the past five years when it saw its’ multiple go from 11.5x trough margins/earnings, to 15.5x peak margins/earnings AND it will take increased capital spending to get there, which we think will result in a lower-return model. And all of this ignores the risk of vendors going increasingly direct to consumer, the move we think we’ll see towards free shipping, higher retail labor costs in 2H, and the need for a 12-year ASP cycle (which is decelerating) to turn into a 13-year cycle, then 14, then 15…

Here are Some of our Notes From the Analyst Meeting (No Particular Order)

Core:

-Remodels - Currently at 20% remodeled at Footlocker, 25% at Champs. Targeting 33% for each this year. Expect 45% remodeled by 2017 (including Footaction). Roughly 50-60% by 2020, never plan to hit 100% as sometimes investment will not be worth the return.

-Expand Vendor partnership concepts: Plan more Flight 23, House of Hoops, Kicks Lounge, Nike Yardline, Puma Labs, A-Standard (adidas). No mention of UnderArmour. Testing these concepts and growing them.

-Investing in Marketing content, with a focus on digital.

-Developing systems - Quantum System allocation tool to be done by 2Q 2015, Order planning tool by late 2015 early 2016. Then need to learn how to use them – which will happen over time.

Kids: Develop kids business globally

-Have 21 Kids Foot Lockers in 5 markets outside US.

-Grow to 50 by 2017

-100 or more by 2020

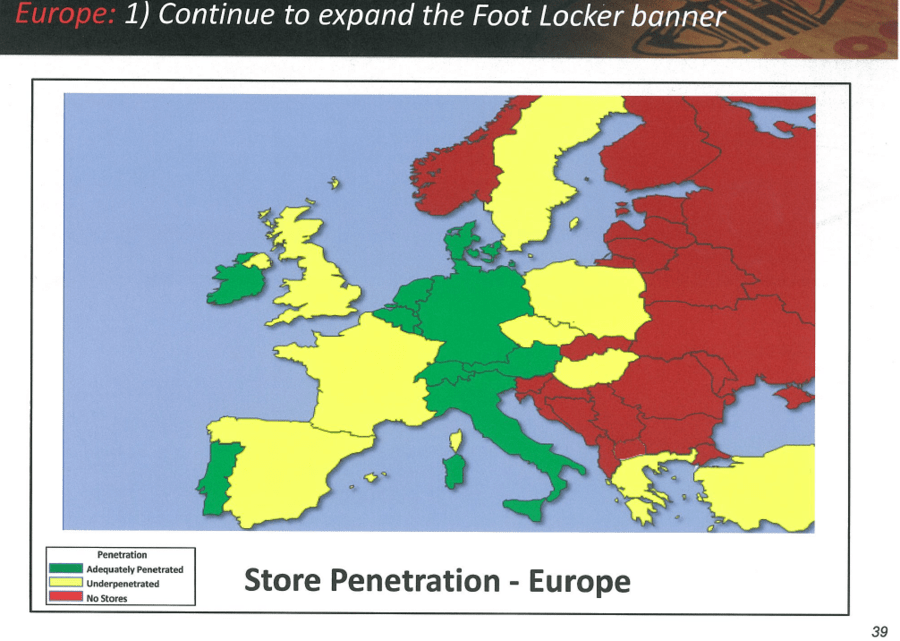

Europe:

-Grow Footlocker and Kids Footlocker

-Rebuild Apparel

-Multi Banner Strategy at RPG with Runners Point (Running), Footlocker (Performance/Lifestyle/US heritage) and Sidestep (Lifestyle)

Here’s a comparison of the company’s 2012 Analyst Day Presentation vs 2015:

2012 Analyst Day

2015 Analyst Day

Biggest Callout: Runners Point purchase helped fill out Western Europe

Apparel: "need to think more like an apparel company" (Nike said this for 20 years before they got it right).

-Increasing premium apparel

-"Our futures model struggles to compete with fast fashion"

-Building private label sourcing to increase speed to market

-Create better assortment and better responsiveness

-Seeing "lift" in remodeled stores, no specifics, but expect that to help.

-Work with vendor partners for merchandising ideas

-“Ken (Hicks) would be happy if we fix this“ (but if it were easy to fix, wouldn’t Ken have done it? He did the opposite – more footwear = higher margin).

Apparel was part of FL’s 2012 plan too…. This is the result – down 400bp as a percent of total.

Digital: Invest in technology

-Estimate that 90% of FL online traffic will come from phone/tablet in 2018. (that sounds high to us…but interesting callout)

-New order management system within a year or two.

-New app to be developed. (everyone else is developing apps too).

-Leverage omnichannel capabilities (BOSS - buy online ship from store, BORIS - Buy online reserve instore), stock locator been in place for years, same day delivery.

-Eastbay Team Sales growth doubled past few years, expand field reps and evolve catalog to increase female presence.

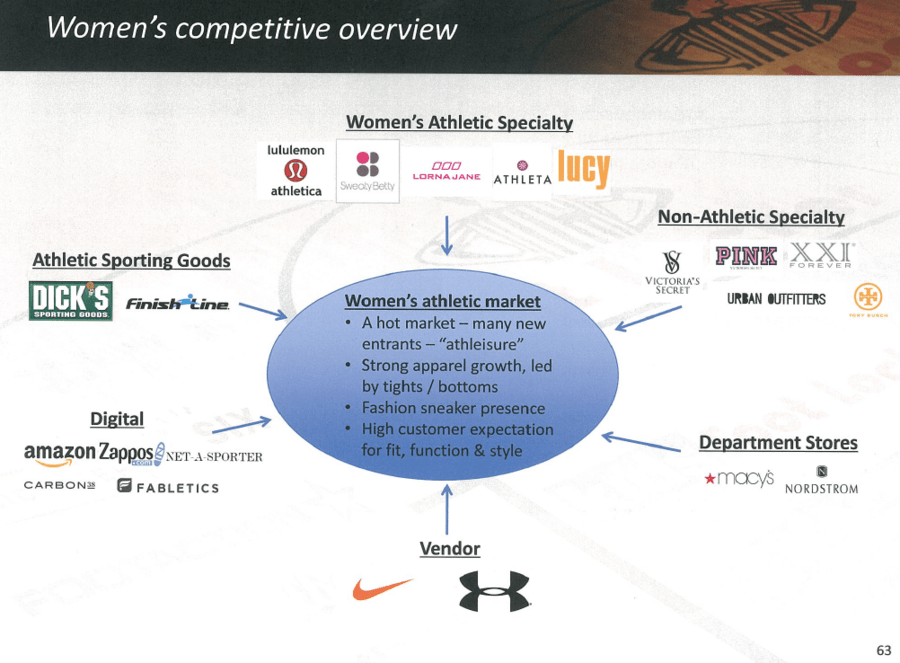

Women:

-six:02 is the way forward. (2 years old)

-A competitive Space

-Targeting total of 35 stores in 2015, then more in 2016, 2015 is still testing phase

-six:02 customer: Her name is Grace, mid 20s to 30s, active, cares about fitness, wants the whole outfit, likes our store set up, likes collections, is an omni channel shopper, and values the digital experience

-from Q/A Lady Foot Locker becoming less of focus and opportunities to close stores will be leveraged.

-Appears Lady Footlocker will be phased out as six:02 ramps up and LFL leases come due. They cannot be converted due to insufficient store size. (Lady =2200, six:02=3200)

Main question topics in Q/A:

Apparel - what is penetration target? Strategies?

-Nothing specific, but would like to be back around 2004 levels by 2020

-Think more like an apparel company.

-Speed to market and responsiveness

Lady FL/Women six:02 - Store strategy

-Been redoing Lady FL, will take advantage of closing opportunities when leases come due.

-Lady stores will not be converted to six:02 as they are not the right size (Lady =2200, six:02=3200)

-10 year leases (sounds long given that FL’s average throughout the chain is closer to 5)

-Unsure about LT target store count

Remodels - trying to get color on remodel success metrics

-No specifics just seeing "Lift"

Relationship with partners (they gave the obvious diplomatic answer)

-Have a great relationship with our vendors

-Pursuing partnered store concepts

-Recognize in they will be competitors, but working on growing the market together

-Believes they can co-exist as they have been

-(question about why no concepts with UA) Considers them strong partner.

Gross Margin- Drivers?

-Higher apparel penetration

-Allocation tool = fewer markdowns.. Then order planning system

-Expect Europe productivity increase

-Women’s to help

EPS/Growth cadence? -

-Assumed to be smooth

-Remodels and apparel driving intermediate term growth

-Women driving longer term growth

Capital plan- buybacks?

-remain flexible, no specifics

Acquisitions?

-nothing built into the plan

Ultimately, Spending Increases - if serious about the growth strategies:

Remodeling stores.

Adding new stores.

Increasing Digital Tech, (new app)

Increasing Marketing investment.

Trialing/Developing new store concepts.

Investing in systems for stores/DTC.

Developing customer interactive content.

Adding EastBay Field Reps.

Our Previous Note on FL from 3/6/15

03/06/15 01:00 PM EST

FL – A Best Idea (Almost)

Takeaway: FL put up the best EPS growth we'll see for a very, very long time. As great as stock looks today it will appear radically different in 1yr

Conclusion: If the company were not hosting an analyst meeting on 3/16, we’d probably add it to our Best Ideas list on the short side today. But we’ll look forward to getting better information from management, and a closer look into their strategy before we act. In all likelihood, in 4Q and FY14, FL just put up the best EPS growth we’ll see from this company for a very very long time. While we’re getting cute on near-term timing, we think this is a multi-year short where you don’t have to wait multiple years to get paid.

We sat here this morning in the wake of FL’s quarter debating whether to add FL to our Best Ideas list on the short side. We’ve been vocal about our short call, and are looking for the right time to go all-in. When a company crushes expectations by 11% and prints a 10% comp, that’s hardly akin to ringing the dinner bell for a new short position. But…as great as this story looks today, we think it will appear radically different in another year – which should take its multiple down a notch or two in addition to eyeing a lower earnings base.

We outline the longer-term factors below, but here are a few things in the quarter that beg the question as to the sustainability of this model.

1. Store Base Growing: The company will add 100 stores this year, but will only close 80. As such, there will be net store openings for the first time since 2006. This matters because of point 4 below, that so much of the model was driven over the past six years by subtraction. Removing and repositioning stores helped drive productivity and margins – while taking capital away from the balance sheet. That took RNOA up to 30% from 5.5%. This growth is coming in Europe, Kids and SIX:02, which probably makes sense. But the real key here is that there are very few bad stores to take out of the model anymore.

(modeling note, on the 4Q11 call, management said "We plan to open 82 new stores and close 75 stores in 2012, which would be the first time in many years that we open more stores than we close." The company ended closing net 34 stores that year. In other words, as business deteriorates, there are more closure candidates.)

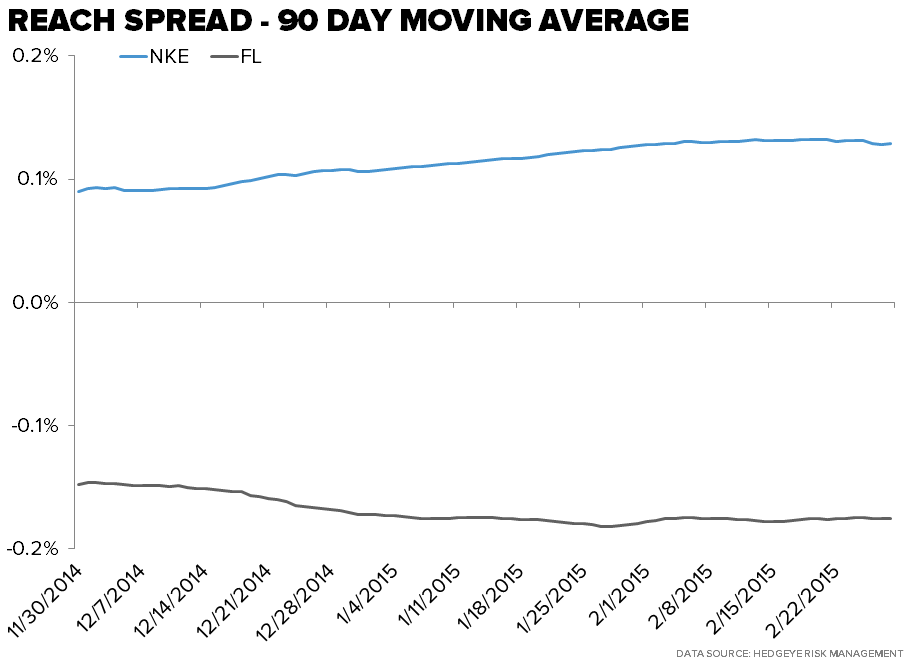

2. E-commerce slowing. While it may be a stretch for us to beat up FL on a 30% growth rate in e-commerce, the fact is that it was up 40% last quarter, and is now growing less than half the rate of Nike. Sorry folks, but that matters big time. Check out the chart below that shows the quarterly e-commerce ratio between Nike and FL. That’s great if you’re Nike. Not if you’re Foot Locker.

3. ASPs in Check, For Now. FL makes it sound like a vendor-love-fest with Nike on ASPs and innovation. True, their futures are connected at the hip. But where do you think Nike’s sweet spot is online? It’s sneakers over $120. It is going to capture a significant portion of the growth in that price zone. While FL is comping 10%, they’ll take Nike’s promises (which we think are intended to be genuine) at face value that NKE will drive FL’s business going forward. But if the environment erodes even slightly, then there’s more of an ‘every man for himself mentality’ and that’s when you see who is really getting the best product.

4. GM at All-Time High. This quarter two different trends became very clear to us. On the one hand we have margins which finished the year at 33.2% -- all-time highs. But the underlying trend on a 2yr basis has been flat over the past two quarters, and that isn’t something to celebrate with a company comping in the HSD-LDDs. The run over 33% was driven in large part by FL taking capital out of the model and a rationalization of its store footprint. Now the company has very little bad left to pare from the portfolio and is actually guiding to 20 additional units which are bigger properties in better locations (six:02 is strictly an ‘A’ mall concept). We’ll see what the company can do without any low hanging fruit. Add to that ongoing IMU pressure its vendors (vendor) and Fx and we think it’ll be very hard to leverage this line during the year.

5. SG&A is Not Sustainable. This quarter SG&A came in 19.98% of sales. Retailers simply don’t get to a SG&A ratio with a 1-handle. We understand that FL is a lean company with a very efficient model. But at an operating margin of 11.3% and long term top line growth guidance of mid to low single digits we don’t think that it will be able to hold on to such a low level of SG&A. In order to maintain top line growth, it needs constant investment in dot.com – in all 23 countries it flies a Foot Locker banner. That’s not cheap…not the systems, and definitely not the people, the design, the advertising, and marketing. (and vendors are paying for less and less every year).

The punchline is that we think this print is likely to serve as the final ‘blowout’ growth quarter for FL, and the factors associated with this industry and model will change dramatically a year out. The stock is having a nice day, but in fairness, one might think that a company that blows away numbers like FL just did would be up more than 4%. We think finding the incremental buyer for FL for anything more than a trade will be tough.

If the company were not hosting an analyst meeting on 3/16, we’d probably add it to our Best Ideas list today. But we’ll look forward to getting better information from management, and a closer look into their strategy before we act. This is a multi-year story where you don’t have to wait multiple years to get paid. We’re looking for our precise entry time and price. Stay tuned.

Our Previous Note on FL from 3/4/15

03/04/15 07:56 PM EST

FL - Why We Think FL Is A Short

Takeaway: Our FL Short Call has a lot of layers that we expect to play out systematically throughout ’15. $20 down/$6 upside.

Conclusion: The biggest pushback, by a long shot, on our FL short call is timing, and how long we have to wait for it to play out. While FL is unlikely to completely melt down this week on the print, especially 2-weeks ahead of an analyst meeting, we definitely think that the building blocks of our thesis will be incrementally evident in the quarter to be reported on Friday (as well as in the meeting on 3/16). But this is a complex call with many layers that will peel off one at a time systematically as 2015 progresses, resulting in downward revisions and revealing a down year in 2016. Ultimately we think it will result in consensus estimates coming down meaningfully for the first time in six years, and we’ll see both lower estimates and multiple compression. We get to $20 downside, and $6 upside.

FL remains one of our top short ideas, but it is also perhaps the most complex. It’s not just about Nike, or about Ken Hick’s leaving, or about e-commerce threats. It’s about this company just having come off a six-year run that was driven by a ‘perfect storm’ (the good kind) of …

a) Margins: economic expansion and margin tailwind,

b) The Hicks Era: a new stellar CEO taking capital out of the model while simultaneously taking productivity and margins to new peaks, and adding 2,000bp to RNOA (RNOA to 25% from 5% pre-Hicks),

c) Nike Penetration: FL taking NKE to 70% of its inventory purchases from 56% – which has meaningful positive implications for gross margin,

d) ASP Cycle: Nike driving a 12-year ASP cycle which accrued to the retailers (like FL) just as much as it did NKE.

e)e-Commerce: Growth in e-commerce without meaningful brand competition.

But today, those factors have changed for the worse... (Here’s the links to our recent Black Book deck and audio presentation where we outline these factors in more detail.)

Call Replay: CLICK HERE

Materials: CLICK HERE

a) Margins: The post-recession margin tailwind is over. We need raw top line growth and productivity improvements to boost margins.

b) The Hicks Era:

1. Ken Hicks is gone. His team is still there. But we think that one of the highlights of the analyst meeting on March 16 will be how the company will be spending to grow. That’s fine, but keep in mind, it has just come off a period where it grew without spending and boosted returns by 2,000bps. Big difference – especially when it’s still sitting at a peak 15x p/e.

2. Also, there’s no more capital to pull away from this model. We outlined in our Black Book how the fleet is largely optimized, and perhaps with the exception of some Lady Foot Locker stores, there’s little left to close or ‘rebanner’.

c) Nike Penetration: Is the next move in Nike as a percent of total higher, or lower? It’s lower. And, quite frankly, it’s HEALTHY for Nike to be a smaller percentage. It’s just probably less profitable. We actually have people tell us “I called Nike and they said the Foot Locker is a really important customer – and that your thesis is wrong’. That’s what Nike HAS TO say. They fight their battles in private, and win where it matters -- on the P&L and the balance sheet. At a minimum, Nike not going higher as a percent of total sales is a negative, as the tailwind that’s existed for half a decade has been underappreciated.

d)ASP Cycle: We’re in a 12-year ASP cycle. Chances are, there will be a year 13. And probably a year 14. This is a space where the tail wags the dog. As the brands spend up in R&D, they drive prices higher. But the difference is that we’re at a point where the higher prices will start to accrue disproportionately to the brands. They (especially Nike) finally have the infrastructure and the product tiers in place to grow their DTC businesses aggressively.

e)e-Commerce: And we’re already seeing this part of the story play out. The charts below show the yy change in reach for FL vs NKE (reach spread is defined as the percent of people using the internet that are using Footlocker.com/Nike.com today versus last year). This will accelerate. What this does is maintains the mid-upper price business for the retailers, but allows Nike to dominate the $160-$225 business on its own site. That’s a problem for FL as its ASP increase has not been broad based. It has been because the retailer added a better mix of shoes at extreme price points.

The biggest pushback we get on any of this is “yeah that’s great guys, but am I going to have to wait another three years before seeing this? Show me the near-term catalyst and roadmap.” Fair question (and trust us, it comes from 80% of the people we talk to). When all is said and done, though FL is unlikely to melt down this week, we definitely think that parts of our thesis will be evident in the quarter to be reported on Friday. But this call has many layers that will peel off (usually) one at a time systematically as 2015 progresses, and ultimately result in consensus estimates coming down meaningfully for the first time in six years.

We’re about in line for the quarter at $0.91 and 6% comp, but are 5% below the consensus for 2015. And by the time we look toward 2016, we’re at $3.46, 17% below the Street.

So what’s this worth? Not 15x earnings, we’d argue. But we’re not going to make a multiple contraction call. But the call we will make is one for lower earnings and growth, and once that is apparent to the Street, the multiple will follow. We think that 12-13x $3.60 in EPS by year end 2015 is realistic as the story plays out, or a $45 stock (20% downside). Looking into 2016, and the likelihood of a down year ($3.46 despite the Street's $4.17) we think we're looking at 11-12x $3.46, or a stock in the high $30s. All in, we're looking at about $20 downside over the next two years, with about $10 per year.

That's about 4.9x EBITDA and a 8% FCF yield, which seem fair for a zero square footage growth retailer with earnings that are shrinking. If we're wrong, we're looking at about $4.25 in EPS power. Keeping today's peak 15x p/e, that suggests a $64 stock. That's about $6 upside versus $20 downside. We think the path of least resistance is on the downside.