EVENTS TO WATCH

COMPANY HIGHLIGHTS

AdiBok, NKE, FL, FINL - Adidas won't bid on NBA apparel deal

(http://espn.go.com/nba/story/_/id/12493645/adidas-pursue-extension-nba-apparel-deal)

Takeaway: This is exactly how a brand should NOT behave. If Herbert Hainer was the CEO of a US company instead of being domiciled in Germany, he'd have been fired years ago. We understand that a company has to look hard at the ROI when it comes to endorsement deals, and it's pretty obvious that the $36mm and change the company coughed up per year to put it's logo on NBA jersey's wasn't making adequate returns as the company continued to shed market share in the basketball category. But, how would NKE have handled this situation? Look no further than the Man-U negotiation where Nike stepped away from a 13-year kit deal with the club only after bidding up the annual fee by 3.2x from £23.5mm per year to £75mm. Now it's a one horse race for the NBA deal which means Nike will pay far less to sponsor a category that it already dominates than it otherwise would had AdiBok played its cards closer to the chest. Who else could compete for this deal? UA needs to be in the conversation, and maybe a Chinese player like Li Ning, though we doubt the NBA would go that route. Let's say the new deal comes in at $45mm per year, that's just 4.5% of NKE's existing endorsement budget, for UA it's 50%.

Now AdiBok wants to focus on NFL and MLB athlete endorsement deals. We'll give the company the benefit of the doubt for this exercise that it knows what it is doing. Think about what that means for Adi's existing wholesale partners. Those are not categories that translate to more floor space. Which means NKE, who already accounts for around 70% of purchases for FL and FINL, becomes even more dominant in it's assortment. The best possible environment for an athletic retailer is when the major brands are heavily competing for shelf space. FL and FINL want nothing more than to have a strong staple of contenders looking to take a few points of share. That's not gonna happen.

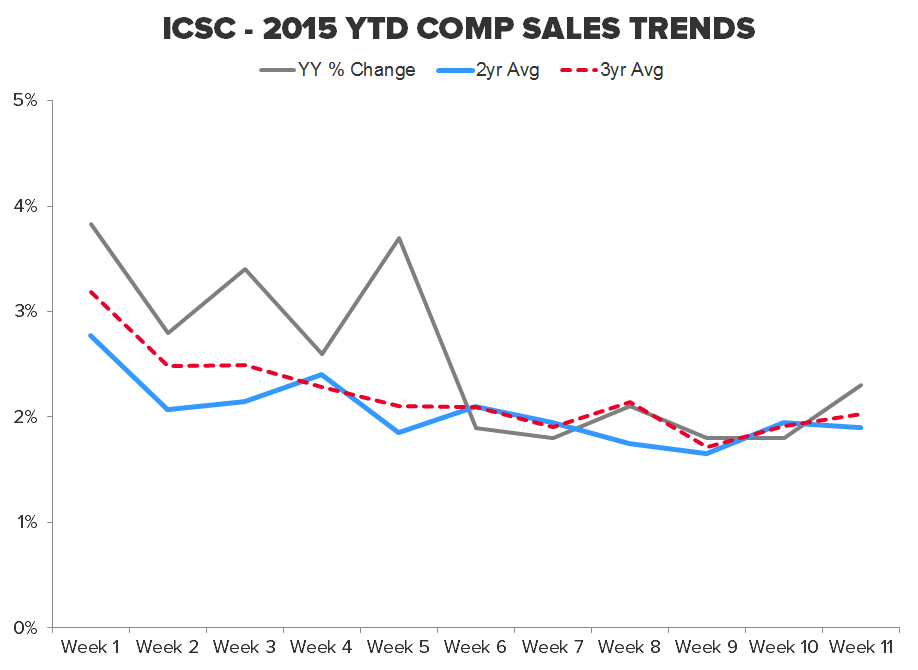

ICSC RETAIL SALES (80 General Merchandise Stores)

Takeaway: Two relatively positive data points from the ICSC to start March, though on a 2-yr basis we saw a slight deceleration for the week ended 3/14. Not the type of strength we would have expected given the easy compares from last year. Two more weeks for retailers to make up some lost ground before comps get much tougher through Spring and Summer.

OTHER NEWS

DG - Dollar General will expand hours, not wages

(http://www.chainstoreage.com/article/dollar-general-will-expand-hours-not-wages)

JCP - JCPenney CMO Debra Berman Departs Company

(http://adage.com/article/cmo-strategy/jcpenney-cmo-debra-berman-departs-company/297608/)

AMZN - Amazon expands in Canada with move to new Toronto skyscraper

Permira to Shed Remaining Hugo Boss Shares

(http://wwd.com/business-news/financial/permira-to-shed-remaining-hugo-boss-shares-10097301/)

Elizabeth Wood to Head HR at Levi Strauss & Co.

(http://wwd.com/business-news/human-resources/elizabeth-wood-to-head-hr-at-levi-strauss-co-10096779/)

UA - Under Armour Releases Kevin Plank’s Earnings

(http://wwd.com/business-news/financial/under-armour-releases-kevin-planks-earnings-10096270/)