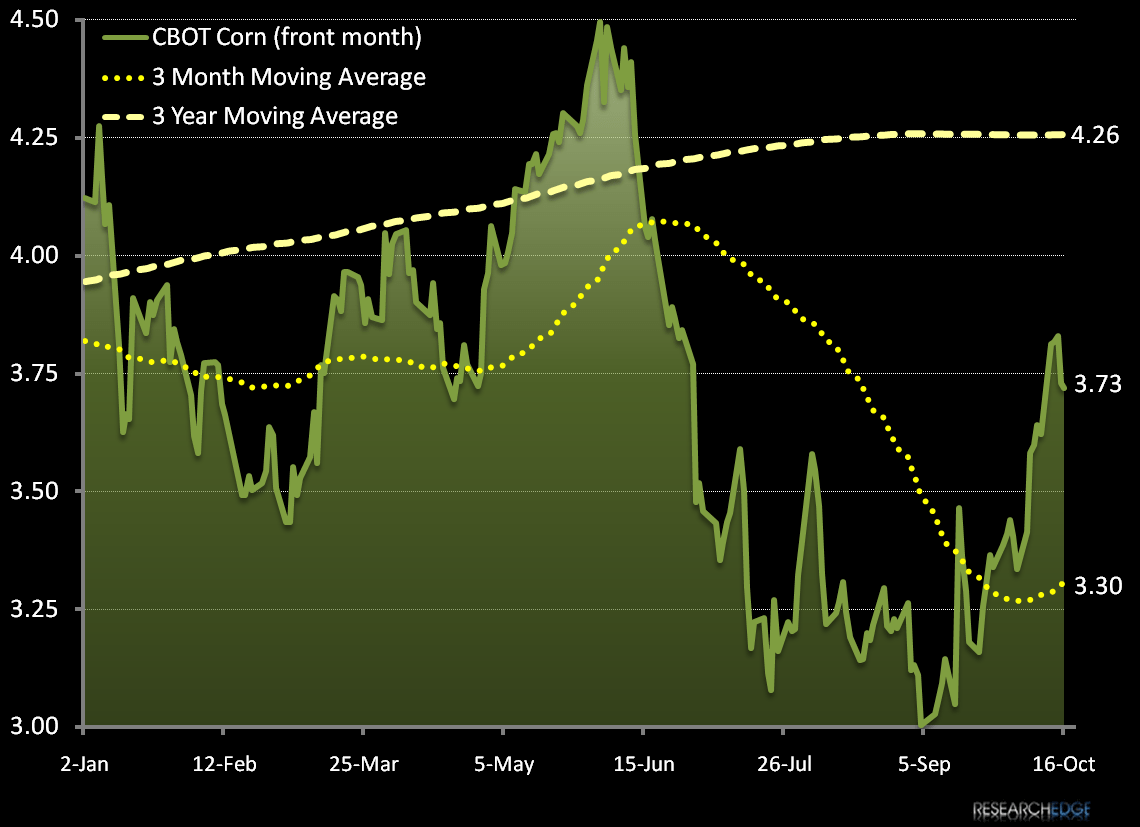

The cold wet weather that has dogged the Midwest this year has caused projected harvest start and completion times to be delayed for staple grains, with Corn and Soybean harvests off to the slowest start in decades. As of October 11, the USDA estimated that only 13% of the total corn crop had been harvested versus an average of 35% by that time in the past five harvests. Although the harvest is seriously delayed, in absolute size it’s anticipated to be a bumper crop: The USDA estimates a 13 billion bushel season for 2009, which would make it the second largest harvest on record.

Futures markets ultimately function as insurance markets however, and despite the size of the yield, anticipated prices have risen sharply as more time in the field creates further risk of weather damage and other unknowns. With the harvest expected to drag into late November, the price of December delivery corn has bounced back from last month’s low close of $3 per bushel on September 4th to almost $3.85 per bushel in today’s session.

Sanderson Farm (SAFM) is trading lower after being downgraded at KeyBanc. The thesis is that rising corn prices make feed costs more expensive. As the story goes corn prices will continue rising due to a declining U.S. dollar boosting exports and expectations that ethanol producers will use more corn.

Keith bought SAFM today on the downgrade. At research edge we do not agree that corn is headed much higher. At the current prices for crude oil, Ethanol is not a concern and the bumper crop for corn will ultimately dictate the future of corn prices, which is likely lower. In two weeks, SAFM will be holding an analyst meeting updating the investment community on where the company is headed and the state of the industry. Notwithstanding a slight uptick in the price of corn, the industry outlook is positive and SAFM is one of the best managed companies in the space.

Our bottom line: Corn has a broken TAIL and a bullish TREND… within an industry that’s been wrecked/consolidated, broken TAIL prices are positive for producers.

Andrew Barber

Director

Kerry Bauman

Senior Analyst