KEY POINTS

- SALES REP CHURN MAY HAVE ACCELERATED: Management attributed its declining salesforce productivity to a higher percentage of sales rep “rookies” , which YELP defines as reps hired 6-9 months ago. A higher percentage of rookies on decelerating sales rep growth suggests elevated churn (at least in 4Q14).

- IT REALLY WASN’T THE ROOKIES: If it takes 6-9 month for a sales rep to ramp as management suggests, then we should have seen a 2H14 acceleration in new account growth from its 1H14 acceleration in sales rep hiring. Unless salesforce attrition was elevated throughout 2014 (which would be a much bigger issue), then rookies can't explain the decline salesforce productivity that occurred throughout all of 2014. We suspect the bigger issue is Point 3 below.

- PRODUCTIVITY LIKELY IN SECULAR DECLINE: YELP’s salesforce (telesales) is already large enough to canvas its entire addressable market in call volume. Hiring more and more reps to call on the same number of clients is essentially the definition of declining salesforce productivity; only leads to higher call volume for existing prospects. It also means that YELP's "rookie" problem could become a growing issue from escalating salesforce churn (too many mouths to feed).

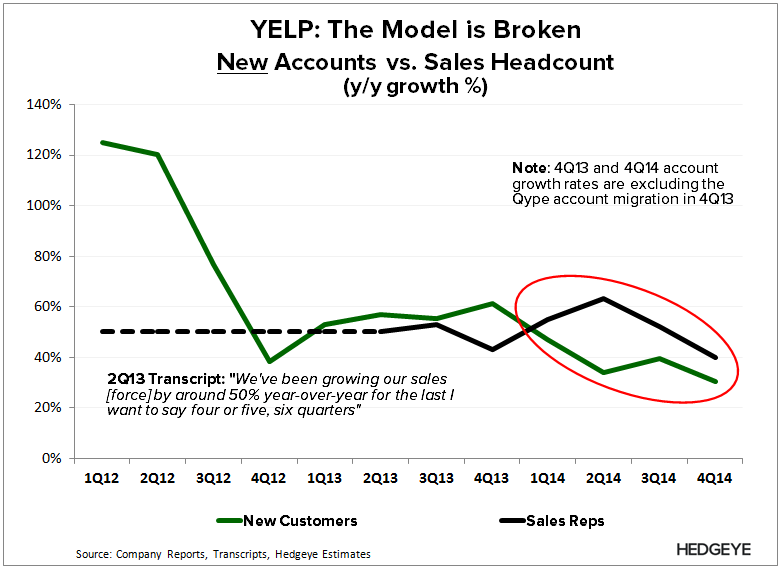

SALES REP CHURN MAY HAVE ACCELERATED

Management attributed its declining salesforce productivity to a higher percentage of sales rep “rookies”, which YELP defines as reps hired 6-9 months ago. We’re not sure what period management’s comments are pointing to (4Q14, or all of 2014), but we estimate productivity has been on the decline throughout 2014.

We suspect the more important takeaway is what that means for sales rep retention. The only way YELP would have a higher percentage of rookies is if its salesforce was growing at an accelerating rate, which wasn’t the case in 2H14 (reps hired in 1H aren’t considered rookies anymore). That said, it’s likely that YELP's sales rep attrition picked up in 4Q14, potentially 3Q14 as well.

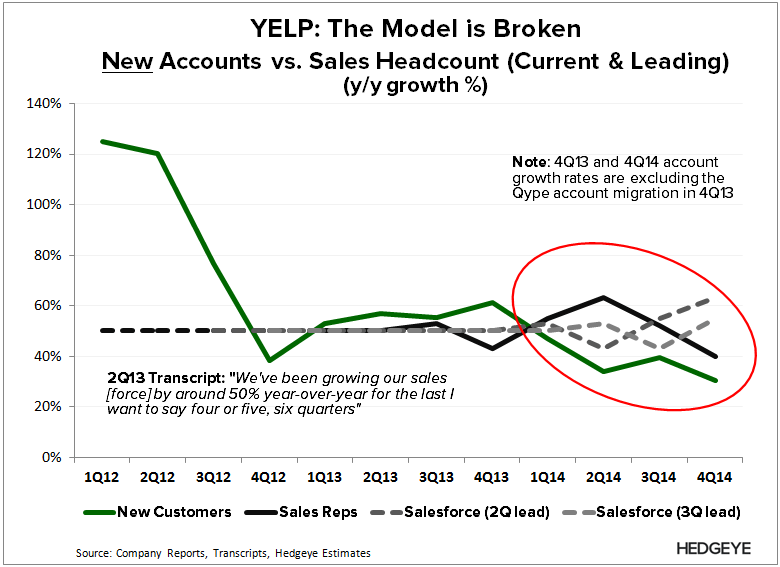

IT REALLY WASN’T THE ROOKIES

Management suggests that it takes 6-9 month for a sales rep to fully ramp. If that is the case, then we should have seen a 2H14 acceleration in new account growth following its 1H14 acceleration in sales rep hiring. In the chart below, we’re comparing YELP’s new account growth against its growth in sales headcount on both a direct and leading basis (e.g. 2Q lead is showing headcount growth from 1Q14 in 3Q14, 2Q14 in 4Q14).

Another explanation could be that YELP did experience a heightened level of sales rep attrition at some point in 2014. But unless that occurred throughout all of 2014 (which would be a much bigger issue), it couldn't explain the decline in salesforce productivity that occurred throughout all of 2014. Either way, it doesn't change the fact that YELP hasn’t been able to generate new account growth in excess of the rate that it’s hearing sales reps at any point in 2014.

If there was ever an admission that YELP’s TAM isn’t large enough to support its model, it would be this persistent decline in salesforce productivity (see note below for our TAM analysis).

YELP: Debating TAM

06/30/14 01:10 PM EDT

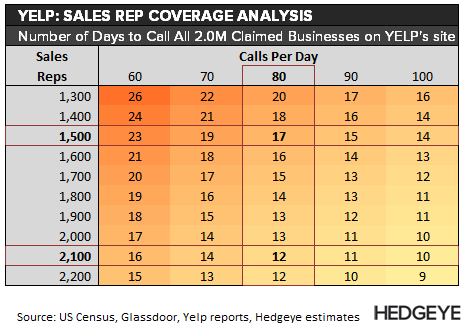

PRODUCTIVITY LIKELY IN SECULAR DECLINE

Hiring more and more reps to call on the same number of clients is essentially the definition of declining salesforce productivity. YELP’s salesforce (telesales) is already large enough to canvas its entire addressable market in call volume.

We illustrate this point in the two tables below, which we are flexing by total sales reps and required daily call volume (note: the recurring theme from employer reviews at glassdoor.com suggests the salesforce is required to make at least 80 calls a day).

In the first table below, we’re calculating how long it would take YELP's salesforce to call all 14.4M B2C business in the US (see TAM note above). Based on YELP’s ~1,500 reps making 80 calls daily, YELP’s salesforce could call every B2C business in the US within 120 days. YELP guided to growing its salesforce by 40% (to 2,100), which will only shrink that window to 86 days.

However, we suspect the primary focus of YELP's salesforce is the 2.0M businesses that have claimed a page on their site (since 2008). YELP probably doesn’t have the current contact info for all 14.4M B2C businesses in the US (YELP licenses business lists from third-parties). Repeating our analysis above for claimed businesses, the call window shrinks to 12 from 17 days.

In short, adding more and more reps just means increasing call frequency, which naturally has a waning benefit. We suspect this is the reason why salesforce productivity is on the decline, and why we believe the issue is secular. We also suspect this will exacerbate YELP's "rookie" problem in the form of escalating salesforce churn (i.e. too many mouths to feed).

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet