Conclusion: The reversal in the stock today says it all. Great quarter. But top line trends are decelerating, costs are accelerating, and capital requirements are going nowhere but up. Any form of growth from here on out – in existing stores, new stores, and online, will all come at a lower margin. This year will be a roller coaster (mostly down) but we think next year’s earnings miss becomes explosive. Still one of our top shorts.

Comps:

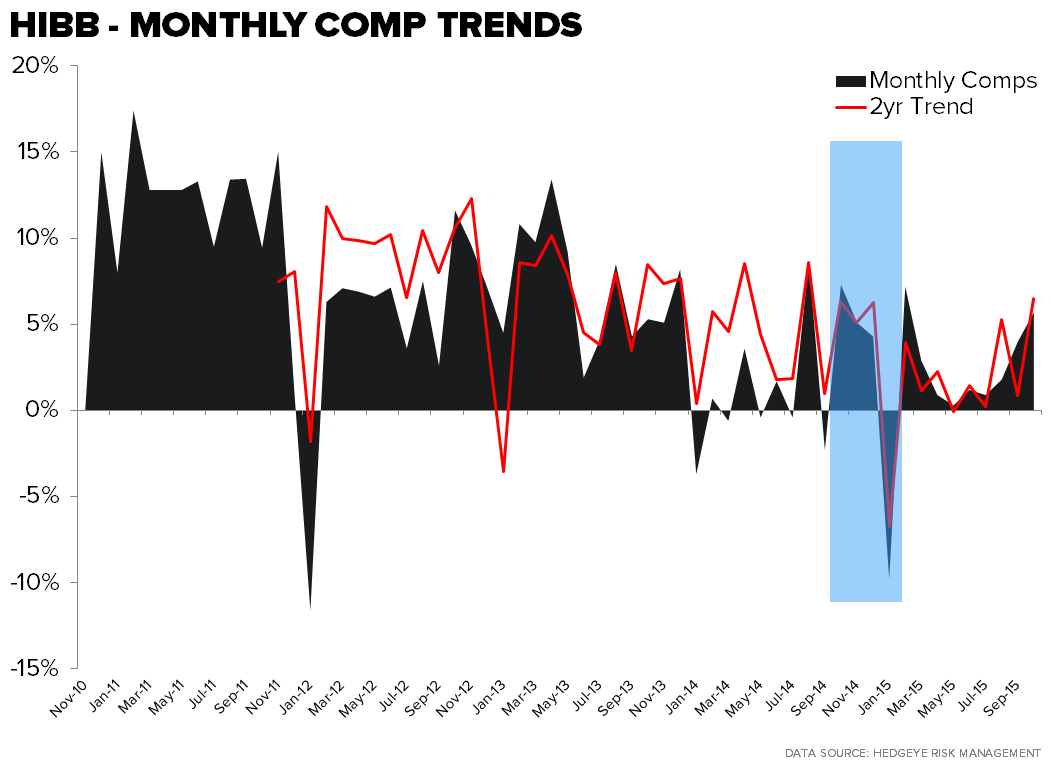

- Comps beat printed Street estimates – which we expected. 5.4% This quarter is literally as good as it can get for HIBB. 1) Wal-Mart, from which HIBB draws traffic in its core market, just printed the first positive traffic comp in nine quarters. 2) Athletic retailers like Dick’s and Foot Locker both printed solid comps in the last two weeks (DKS +3.4%, and FL +10%). 3) HIBB went against its second-easiest comp in over five years in the month of January.

- Comps 1QTD are down MSD. February comps were up against a tough 7.2% comp last year. That month carries the bulk of the volume in the quarter. We think it’s close to 40%, though management indicated it was 35% of the quarter, the math just doesn’t add up. If we look at the numbers from last year it would mean that weights by month were Feb 35%, March 49%, and April just 16%.

- For the quarter, in order to climb out of the hole and get to flat on the year, HIBB would need to average a 3.3% comp in March and April. To get to 1%, the math works out to a 5% comp in March and April. We don’t think that happens.

Costs Accelerating: The $0.12 in cost pressure in FY16 is just the beginning of a multi-year investment cycle for HIBB. Most of that is driven by investment to build an e-commerce operation from scratch. For the year it’ll cost HIBB somewhere in the range of 50bps-60bps in operating margin. That won’t go away in 2017, in fact it will accelerate (more on that below). We also think it’s important keep in mind that the hurdle rate for HIBB at a 3% comp (which the company has been unable to achieve in over 2yrs) makes it very difficult for the company to leverage fixed cost on both the COGS and SG&A lines.

- Distribution – HIBB currently outsources distribution for about 20% of its stores. With only one DC located in Birmingham, AL it’s extremely difficult for the company to efficiently supply its new stores popping up in states like PA, MN, and WI. That means the majority of new growth comes in at an incrementally lower margin. That will compound itself until the company builds a new DC that can service these markets, which has its own capital and margin implications. But, HIBB has to tap new geographies in order to drive the top line – the company’s core southern markets are tapped and competition for consumers in a market that HIBB has historically dominated looks a lot different than it did 4yrs ago. Academy has increased its unit count in the ‘Bible Belt’ by 93% over the past 4 years, Sports Authority and Dick’s Sporting Goods are +45%.

E-Commerce: It appears as if HIBB will finally start making the push towards e-commerce in earnest. Though no concrete timeline was given, it was clear on the call that there is finally a sense of urgency to start competing on the web. Management said it would cost them $0.05 in this upcoming year. That will accelerate as HIBB gets closer to its launch date. All in it equates to about 3-5 percentage points of margin based on what we’ve seen from other companies (to see our Black Book for more detail CLICK HERE).

- The POS system is step 1a in the rollout of an e-commerce channel. Here is how we are thinking about the HIBB’s e-comm needs and timeline. This would of course mean that HIBB decides to build its capabilities in house rather than outsource which would get the company to market faster but come with an extra margin hit.

- 1a) POS – hardware installation, 2H calendar ’15.

- 1b) POS – software and implementation, 1H ‘16

- 2) DC – Pick and pack capabilities, 2H ’16 – 1H ‘17

- 3) Ship-from-store – 2H ’16 – 1H ‘17

- 4) IT and website construction – now – 1H ’17

- All in we are looking at a minimum of 18-24 months of investment needed just to get the e-commerce systems in place before customers even place an order. And that’s while other competing retailers move just as fast if not faster in accelerating their own dot.com business. In other words, HIBB iwill not be gaining share online – just losing share at a lesser rate until its implementation is complete. And again, we think management is in complete denial as to the negative margin impact.

- Then HIBB will be stuck fulfilling orders for a channel with Gross Margins at least 1000bps below the Brick and Mortar business.

Previous Note on HIBB from Thursday 3/12

03/12/15 06:55 AM EDT

HIBB – As Good As It Gets

Takeaway: This quarter should be as good as it gets for HIBB. Don’t get used to it.

We think that HIBB is one of the most structurally challenged retailers out there. But we’re definitely not counting on the company showing its true colors with the print this Friday. This quarter is literally as good as it can get for HIBB. 1) Wal-Mart, from which HIBB draws traffic in its core market, just printed the first positive traffic comp in nine quarters. 2) Athletic retailers like Dick’s and Foot Locker both printed solid comps in the last two weeks (DKS +3.4%, and FL +10%). 3) HIBB went against its second-easiest comp in over five years in the month of January. All-in, the comp for 4Q14 will more likely than not come in ahead of the Street’s 3.2% expectation. Somewhere in the mid-single digits is more likely, with EPS closer to the low $0.70s vs. the Street at $0.68.

So…what does this mean? It means that HIBB is our least favorite type of call. The kind where we say it’s a short, but where estimates in the upcoming quarter are too low. When we hear someone make that kind of pitch, it usually ends up being a really lousy call.

So how and why can we stick with a short call on a name in the face of a likely positive event? A few reasons...

1) Smoking Required. HIBB absolutely positively has to smoke this quarter due to factors above (see charts below). Again, the climate has never been more favorable for a retailer like HIBB. The stock is up 10% relative to the market over the past month. If it does NOT smoke numbers, then it spells big trouble for this company.

2) e-Commerce Hit Inevitable. It’s no secret the company needs to install an e-commerce platform. It should be very expensive – costing 3-5 points in margin over 12-18 months before a dollar in dot.com revenue is recognized. Will HIBB announce that initiative on Friday? We don’t know. It will be some time this year. They’re just prolonging the inevitable.

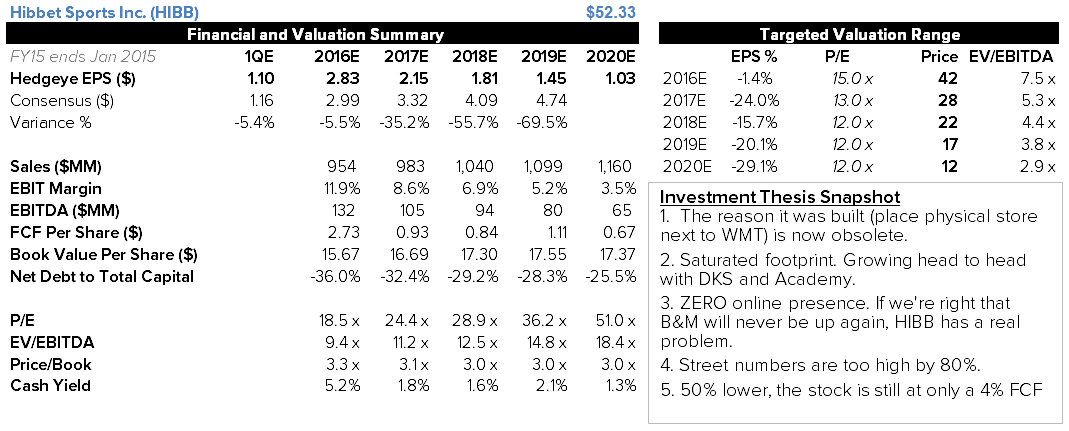

3) Huge Estimate Gap. The gap in margin between our estimates and the Street’s are simply colossal. This year, we’re 7% below. That’s not huge. But in ’16 we’re at $2.06 vs the Street at $3.33. By the time we get to year 5 of our model, we have HIBB earning $1.35 vs the Street at $4.74. The point here is that if we’re calling for estimates to come down next year by nearly 40%, we’re hardly going to be spooked by a few pennies on the upside.

WMT Traffic – Key For HIBB Comp – Positive For The First Time In Nine Quarters

FL Comp Trends Are Off The Chart. Not Identical Businesses, But Close Enough.

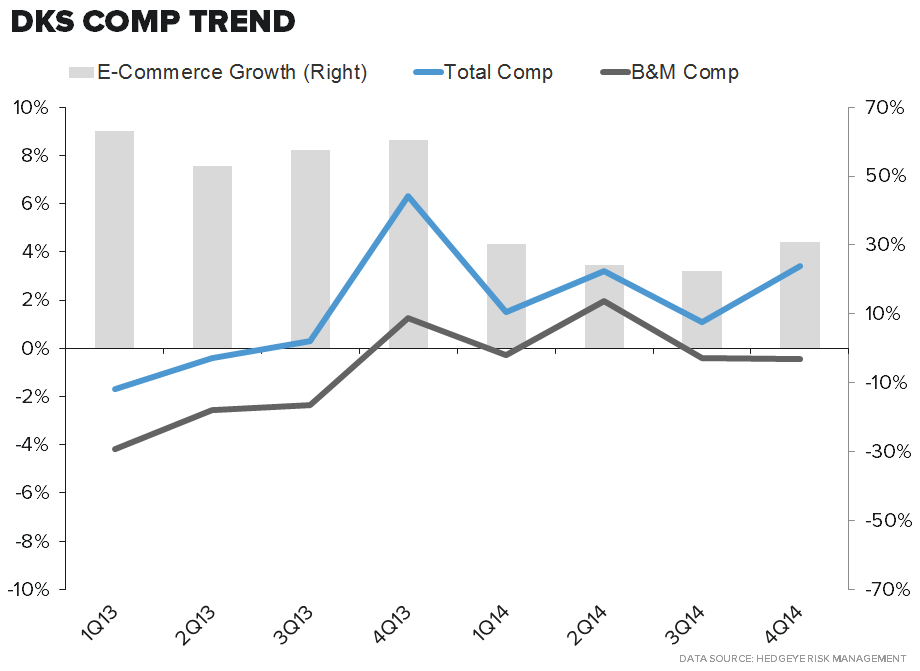

Ditto For DKS – Though Less Positive Than FL. Comp Driven By e-Comm (which HIBB does not have), Brick&Mortar Down

HIBB Monthly Comp Trend Shows The This Quarter Goes Against Second Easiest Comp In Over 5-Years