COMPANY HIGHLIGHTS

HIBB - As Good as it Gets

Quick thoughts on the HIBB Print...

- Comps beat printed Street estimates – which we expected. This quarter is literally as good as it can get for HIBB. 1) Wal-Mart, from which HIBB draws traffic in its core market, just printed the first positive traffic comp in nine quarters. 2) Athletic retailers like Dick’s and Foot Locker both printed solid comps in the last two weeks (DKS +3.4%, and FL +10%). 3) HIBB went against its second-easiest comp in over five years in the month of January.

- Gross Margins were down 30bps on a 5.4% comp. There are some added cost pressures this year due to the new DC in Birmingham, but this isn’t the HIBB of old where it could leverage occupancy on flat to down comp numbers. 1) Occupancy is going up, 2) distribution costs in non-core markets (where most of the growth is coming from) is done by a 3rd party vendor, ie more costly solution, and 3) merch margins which have been down in the past 3 quarters don’t appear to have helped in the quarter.

- Guidance – The company guided to LSD to MSD comp growth for the year. Reading between the lines on February, it appears the quarter is off to a slow start. Comps get easier for the rest of the Month going up against a 2.9% in March and 0.9% in April, but February (due to the NBA All-Star Game) carries the bulk of the quarter.

- Inventory – Inventories came in the lightest they’ve been in 7 quarters with the sales to inventory spread at 3.8%. We read nothing in the press release to indicate that the company has seen any disturbances in product flow due to the West Coast port issues, but we don’t see how HIBB walked through that unscathed. We’ve seen it cited from a number of companies to-date including BGFV, and think it contributed to HIBB’s cleaner inventory position.

For our prior note on HIBB from 3/12 CLICK HERE

KATE - KATE SPADE & COMPANY ANNOUNCES NOMINATION OF JAN SINGER FOR ELECTION TO BOARD OF DIRECTORS

(http://phx.corporate-ir.net/phoenix.zhtml?c=82611&p=irol-newsArticle&ID=2025414)

Takeaway: This is a big win for KATE. Singer has one of the best resumes in the business and gets how to take a powerful brand/product and scale it across an international platform. We'd argue with anyone that KATE's share of voice is much higher than its actual share of wallet. Now the brand needs to grow into a footprint to capitalize on its wide consumer acceptance. Bernard Aronson and Kay Koplovitz (the two outgoing Directors) have been with the company for 17yrs and 23yrs respectively. They both have impressive resumes in their own right, but KATE is a much different animal than LIZ was 20 years ago. We think the company will benefit from some new blood, especially with Singer's pedigree.

OTHER NEWS

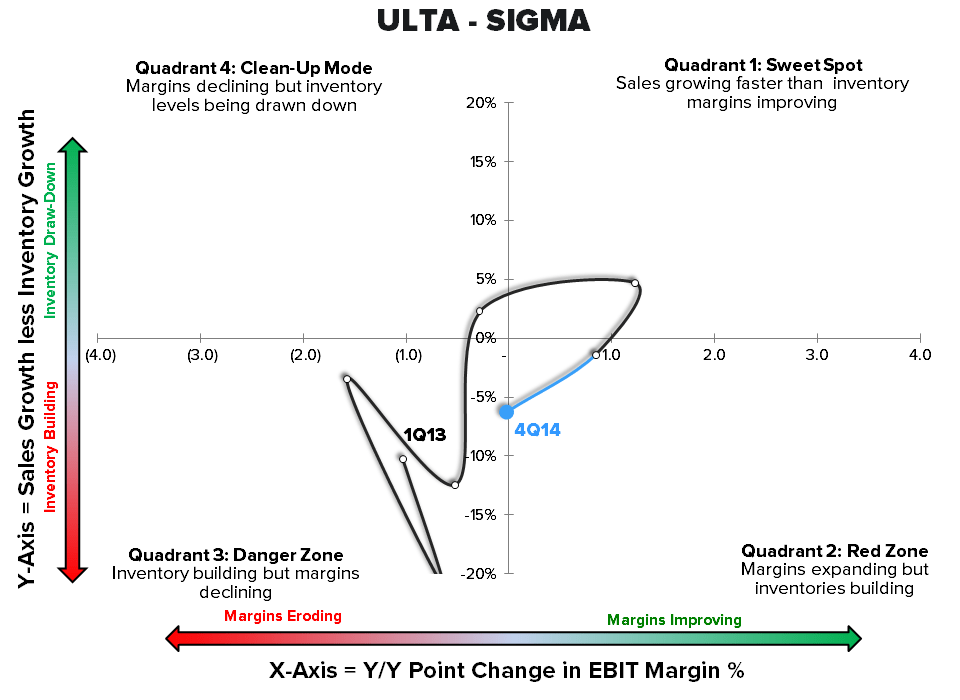

ULTA - 4Q14 Earnings

ARO - 4Q14 Earnings

ZUMZ - 4Q14 Earnings

Sir Philip Green Sells BHS to Retail Acquisitions Ltd.

AMZN - Amazon Has Quietly Acquired 2lemetry To Build Out Its Internet Of Things Strategy

PLCE - Children's Place increases store closures

(http://www.retailingtoday.com/article/childrens-place-increases-store-closures)

COLM - Columbia Awarded $3.3M for Faulty Heating Technology

(http://wwd.com/business-news/legal/columbia-awarded-3-3m-for-faulty-heating-technology-10095154/)

Metro on the lookout for acquisitions