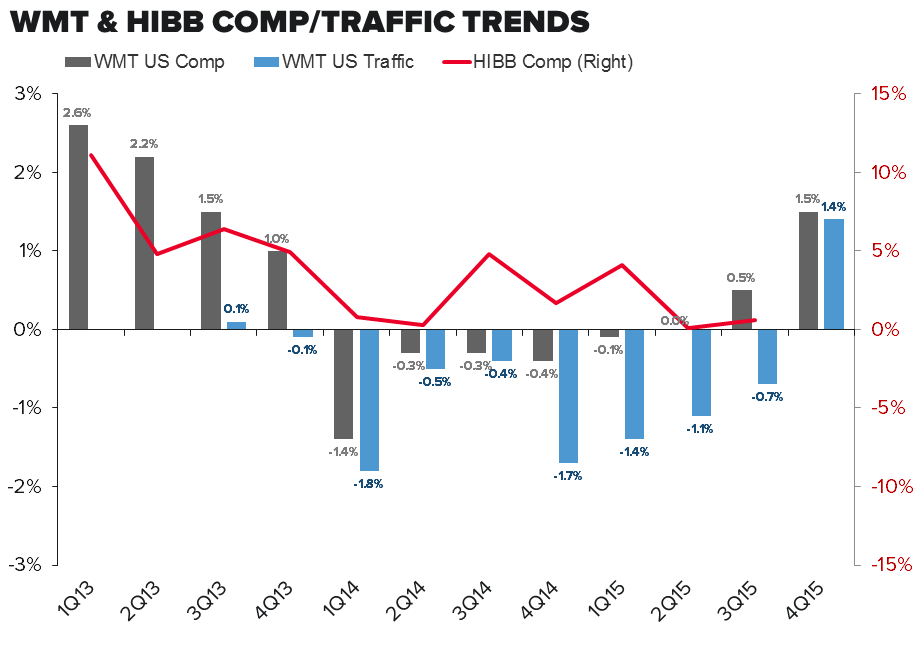

We think that HIBB is one of the most structurally challenged retailers out there. But we’re definitely not counting on the company showing its true colors with the print this Friday. This quarter is literally as good as it can get for HIBB. 1) Wal-Mart, from which HIBB draws traffic in its core market, just printed the first positive traffic comp in nine quarters. 2) Athletic retailers like Dick’s and Foot Locker both printed solid comps in the last two weeks (DKS +3.4%, and FL +10%). 3) HIBB went against its second-easiest comp in over five years in the month of January. All-in, the comp for 4Q14 will more likely than not come in ahead of the Street’s 3.2% expectation. Somewhere in the mid-single digits is more likely, with EPS closer to the low $0.70s vs. the Street at $0.68.

So…what does this mean? It means that HIBB is our least favorite type of call. The kind where we say it’s a short, but where estimates in the upcoming quarter are too low. When we hear someone make that kind of pitch, it usually ends up being a really lousy call.

So how and why can we stick with a short call on a name in the face of a likely positive event? A few reasons...

1) Smoking Required. HIBB absolutely positively has to smoke this quarter due to factors above (see charts below). Again, the climate has never been more favorable for a retailer like HIBB. The stock is up 10% relative to the market over the past month. If it does NOT smoke numbers, then it spells big trouble for this company.

2) e-Commerce Hit Inevitable. It’s no secret the company needs to install an e-commerce platform. It should be very expensive – costing 3-5 points in margin over 12-18 months before a dollar in dot.com revenue is recognized. Will HIBB announce that initiative on Friday? We don’t know. It will be some time this year. They’re just prolonging the inevitable.

3) Huge Estimate Gap. The gap in margin between our estimates and the Street’s are simply colossal. This year, we’re 7% below. That’s not huge. But in ’16 we’re at $2.06 vs the Street at $3.33. By the time we get to year 5 of our model, we have HIBB earning $1.35 vs the Street at $4.74. The point here is that if we’re calling for estimates to come down next year by nearly 40%, we’re hardly going to be spooked by a few pennies on the upside.

WMT Traffic – Key For HIBB Comp – Positive For The First Time In Nine Quarters

FL Comp Trends Are Off The Chart. Not Identical Businesses, But Close Enough.

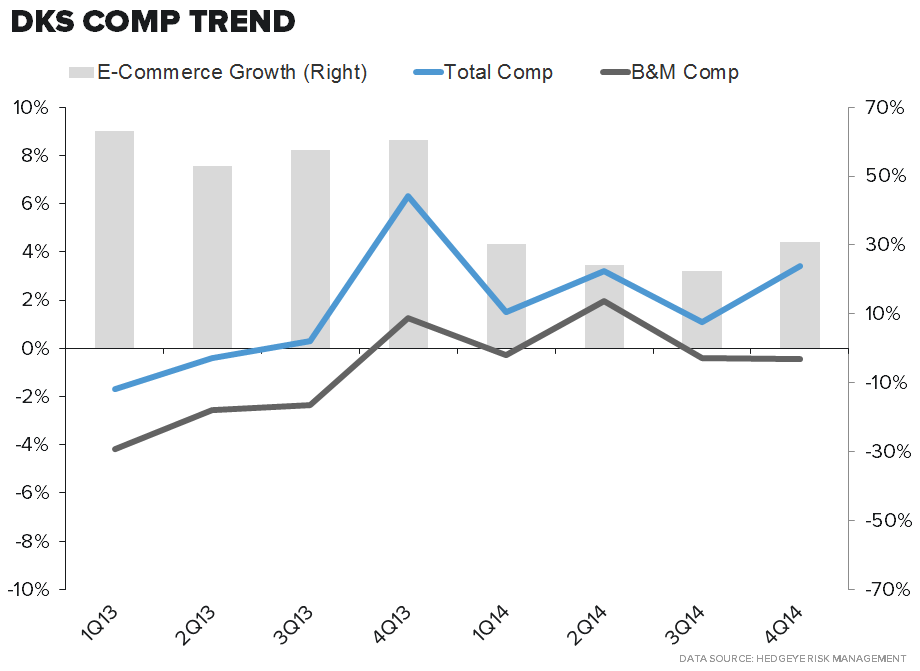

Ditto For DKS – Though Less Positive Than FL. Comp Driven By e-Comm (which HIBB does not have), Brick&Mortar Down

HIBB Monthly Comp Trend Shows The This Quarter Goes Against Second Easiest Comp In Over 5-Years

HIBB – Hedgeye Financial Summary