What has been a gas price tailwind vs. last year is going the other way. Further, California is posting the biggest (unfavorable) spread in recent history. There are implications for retail.

We’re in an interesting position right now as it relates to gas prices. As consumers, we see prices going up sequentially, which has been the case for almost this whole year. We’re now looking at prices near 12-month peak levels. But relative to last year, we’re still looking at prices nearly a buck lower. As it relates to share of wallet, that’s big. But by late November, we’re at a point where the yy positive delta goes away due to the precipitous decline in oil we saw around this time last year. In other words, this has been a tailwind for most of ’09, and it’s about to turn into a headwind.

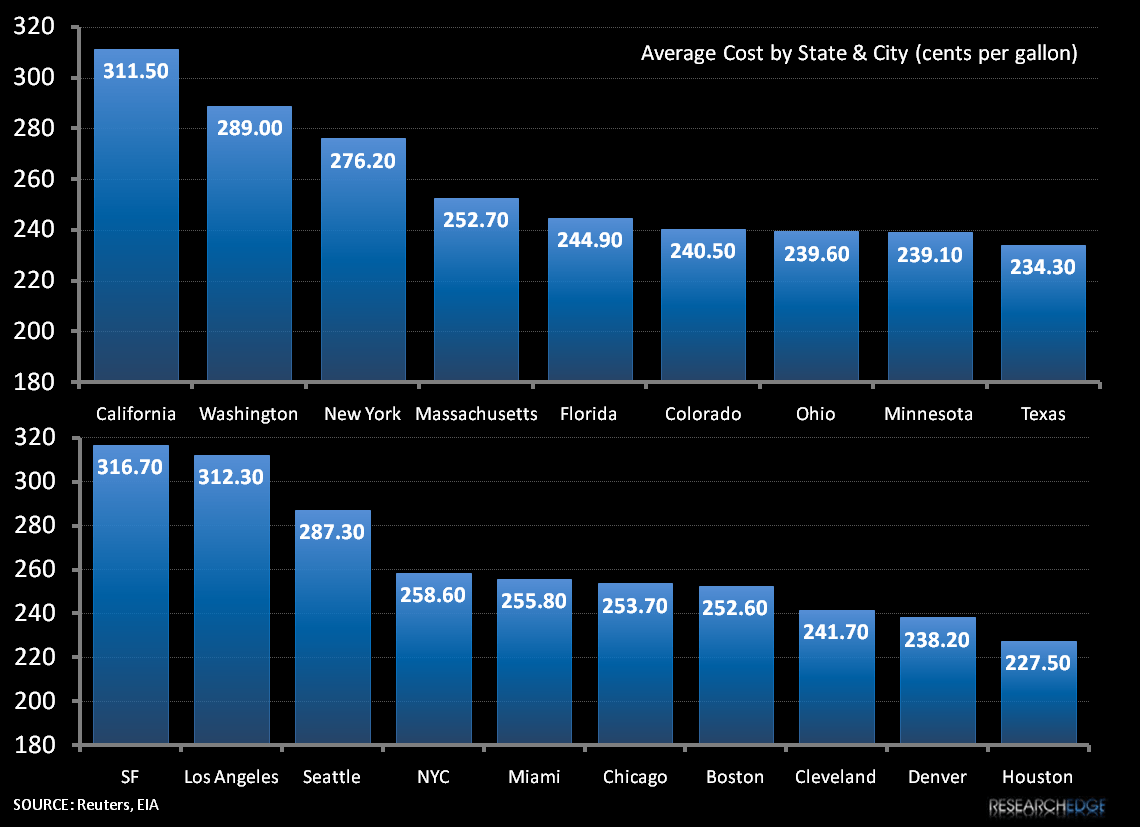

My colleague Andrew Barber brought something to my attention that otherwise slipped right past me. That’s the relative trajectory of West Coast prices. Simply put, over the past month, we’ve seen a divergence in West Coast prices vs. the National Average that we’ve not seen in over 15 years. In effect, National prices are rolling and California prices are going the other way.

We can speculate all day about how this will negatively impact players like Ross Stores (which is on my short bench), but the bigger impact, I think, will be on smaller (mostly private) regional players that are hanging by a thread. They have visibility on cash flow today – like the rest of retail – but as holiday approaches, that visibility goes punk. My sense is that accelerates the rate at which players like Dick’s will step up and acquire real estate as incumbents go bust.