Editor's note: This research note from Hedgeye's Restaurants team was originally published February 12, 2015 at 13:18. The stock is down over -4% since.

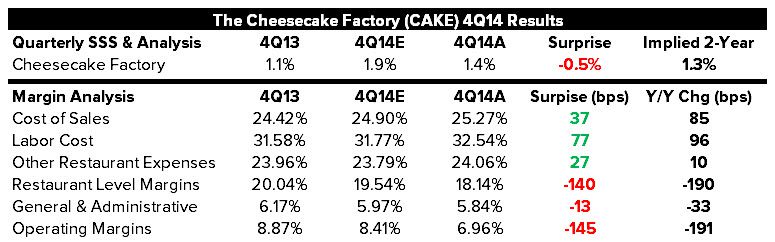

CAKE delivered one of the worst prints we’ve ever seen out of them, missing top line and bottom lines estimates by 177 bps and 2025 bps, respectively. Comps also disappointed, coming in at +1.4% vs the +1.9% consensus estimate. After reading the press release, and seeing the massive level of margin deterioration, we didn’t think it could get much worse – and then the earnings call started.

COST PRESSURES

Management’s commentary on food and labor inflation was critical on a couple of levels: 1) CAKE will be hard pressed to grow margins in 2015 and 2) this is awful news for the small and weak players in the industry.

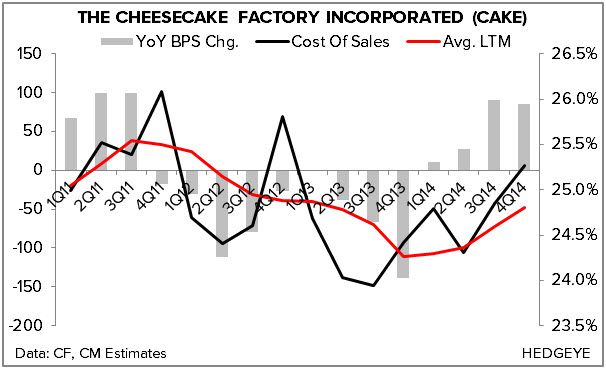

To the first point, CAKE’s food cost pressures in 2014 were widely recognized due to higher dairy and seafood prices. But the degree to which this line de-levered over the course of the year was astounding. Management conceded that it is considering supplementing its contracting with direct hedging, but to what extent this will help is unknown. While many expected CAKE to be one of the largest beneficiaries of the retreat in dairy prices, beef and, to a lesser extent, chicken are expected to drive 2-3% commodity inflation in 2015. They will have a very difficult time leveraging this line further without delivering a 2%+ comp, a feat they haven’t accomplished in over two years.

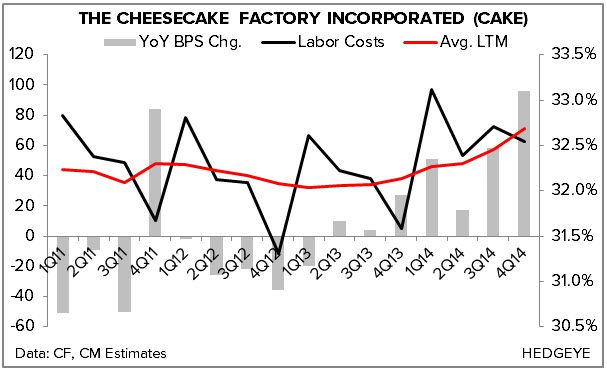

Labor inflation was a much less publicized issue throughout the year that the company mainly attributed to unusually high group medical claims. This pressure, however, is expected to continue in 2015 and could be compounded by minimum wage increases in select states across the nation. All in, management expects $10-12 million in wage inflation. We wrote in a bearish Black Book last January that the margin story was over for CAKE and it certainly appears to be. They haven’t driven labor leverage since 1Q13 and probably won’t anytime soon.

To the second point, and we’ll have more on this in a later post, the pressure CAKE is seeing is not limited to them. If a well-established player in the casual dining industry is struggling to control these costs, what does that mean for smaller, rapidly expanding players in the industry? They’re going to feel a bigger impact – and it’s not going to be pretty. Minimum wages increasing and the restaurant job environment is improving. It’s getting increasingly difficult and expensive to retain employees – an issue that, just today, Panera referred to as the “war for talent.” In the coming days, we’ll unveil a list of companies that we believe will have a much more difficult time operating in this environment than consensus expects. And, yes, we’d short all of them.

ANEMIC TRAFFIC GROWTH

“Holiday 2013 was the first in which many traditional bricks and mortar retailers experienced in-store foot traffic give way to online shopping in a major way.”

-Howard Schultz, Chairman/President/CEO/Founder

Howard Schultz made this remark last year on his company’s 1Q14 earnings call – and we think it’s spot on. If it’s not, CAKE’s traffic isn’t doing much to suggest so. Traffic declined -1.2% in 4Q14, marking the ninth consecutive quarter of negative traffic. Management insists it’s not related to the secular decline in mall traffic but, if that’s the case, they need to prove it. The traffic and margin decline we’re seeing suggests this company is operating a broken model and, if it’s to be fixed, it will take significant time and investment.

UPSHOT

CAKE guided FY15 EPS to a range of $2.08-2.20 on 1.5-2.5% comp growth, a far cry from the current $2.42 consensus estimate. If they want to hit this range, they’ll need to deliver strong comp growth and, with limited drivers in place, we’re not sure how they do that. Speaking to the lack of incremental leverage in the business model, management actually admitted that it needs to either develop or acquire a growth concept in order to deliver long-term EPS growth in the mid-teens. And you probably already know how we feel about multi-concept operators. This brand is in trouble and, if it weren’t down 10% today, we’d short it. In fact, if it bounces meaningfully, we’d likely jump at the opportunity.