KEY POINTS

- THE MODEL IS DETERIORATING: YELP’s business model isn't sustainable; we're already seeing signs that its model is breaking down at a progressively worse rate within its reported metrics.

- HIDING THE BODIES: In response, management is now manipulating its reported metrics to mask what's really happening. In addition, YELP made a very questionable acquisition, and potentially understated its expected revenue contribution (link) to make its core business look better.

- PENDING IMPLOSION: The overriding theme is that these suspect moves aren't any more sustainable than its current business model. Management may buy themselves a short-term reprieve on its stock, but are only raising the sell-side bar on a fading buy-side growth story.

BROKEN MODEL

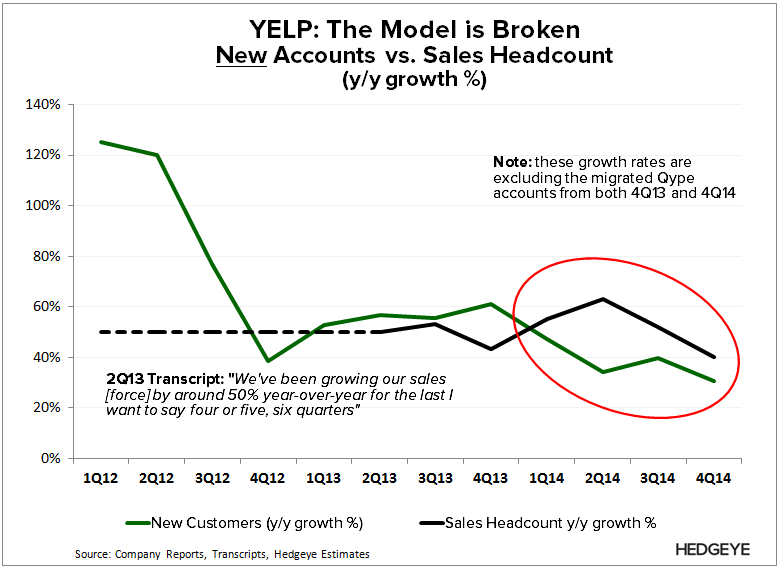

YELP’s Local Advertising segment is riddled by an absurd level of attrition, which is becoming increasingly more challenging to overcome as the company presses up against a limited TAM that can’t support its model. We can already see YELP’s model breaking down in its reported metrics. So in response, management is now manipulating that very data in order to hide what’s really going on.

HIDING THE BODIES

Below are series of suspect moves that management has taken to mask its rampant attrition issues, and overstate the fading strength in its core Local Advertising segment.

- FLUFFING LOCAL ADVERTISING METRICS: Starting in 2015, YELP will be reclassifying the revenues from its SeatMe reservation service from “Other Services” segment into “Local Advertising” Segment. In turn, YELP will be printing an artificial lift through 2015 in both Local Advertising Revenue and its Local Advertising Accounts. The sell-side bulls will confuse that as fundamental strength.

- HIDING THE BODIES: Starting in 2015, YELP will no longer provide its legacy Active Local Business Account metric in favor of a new metric called “Local Advertising Accounts”, which only includes accounts contributing to its Local Advertising Revenue. There are two implications here.

- Pulling the Wool Over Your Eyes: This makes it easier to hide the SeatMe reclassification into Local Advertising since it will be pulling SeatMe from its larger legacy account metric that it will no longer be reporting.

- Buying Some Deniability: YELP’s customer repeat rate is based off the legacy account metric mgmt will be retiring. This means that we can’t explicitly calculate its customer mix (and attrition) moving forward. This gives management deniability, but doesn’t change anything.

- BUYING GROWTH: YELP has a history of making questionable acquisitions to mask weakness elsewhere in its business. With its most recent Eat24 acquisition, there's a good chance that management grossly underestimated Eat24's expected revenue contribution given that associated $36M revenue guidance raise is roughly inline with what Eat24 may have been generating back in 2013 (link).

- SeatMe: Reservation service acquired into 3Q13. SeatMe accounts were reclassified into Active Local Business Accounts beginning 2014, and its revenues are being reclassified in Local Advertising starting 2015.

- Cityvox SAS/Restaurant-Kritik: International competitors acquired in 4Q14 after YELP couldn’t produce revenue growth off its international Qype acquisition from 4Q12.

- Eat24: Food-ordering service acquired in 1Q15. We have no idea how YELP will account for the service, but if it can reclassify its SeatMe reservation service as Advertising business, there is nothing stopping them from doing the same with Eat24.

PENDING IMPLOSION

The overriding theme is that these suspect moves aren't any more sustainable than its current business model. Management may buy themselves a short-term reprieve on its stock, but are only raising the sell-side bar on an a fading buy-side growth story.

This is how we see the progression of the YELP's earnings releases as we move through the year.

- 1Q15: Let's say YELP knocks the cover off the ball on the 1Q15 release and raises guidance. Consensus then raises estimates even higher as they always have (likely 2H15 weighted, with 2016 even higher).

- 2Q15: the bar is now higher. YELP could produce 2Q15 upside, but its 3Q15 guidance release is likely less impressive, if not light.

- 3Q15: YELP can't guide 4Q15 estimates above consensus estimates since the sell-side has raised the bar too high throughout the year.

- 4Q15: Consensus expectations for 2016 have steadily risen throughout 2015 with the sell-side trying to justify their price targets. Now, YELP needs a much bigger acquisition and/or a more egregious accounting maneuver to distract the street...while hoping no one catches on.

In short, the setup for YELP will become progressively more challenging as we move through 2015 into 2016. Even if the stock pops on the 1Q15 release, it likely ends the year lower than it started once YELP doesn't raise guidance above expectations (likely 2H15).

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet