COMPANY HIGHLIGHTS

February Comps -

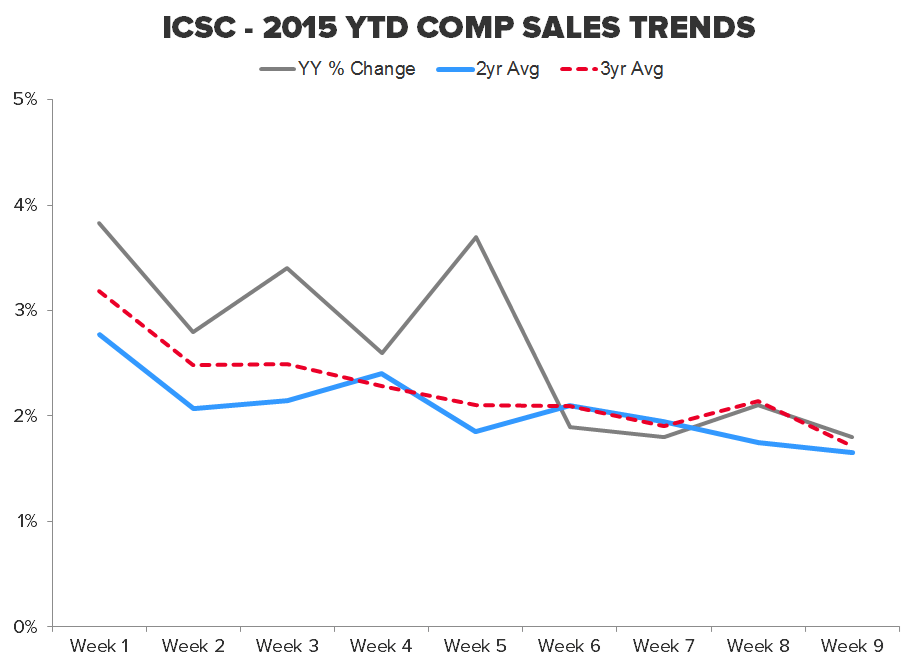

Takeaway: Weather was an issue last year during February, and it's been equally as bad this year. The 2-yr trend in the ICSC has been decidedly negative since the year started drawing essentially a straight line from 3% to 2% over the 9-weeks to date.

That manifested itself in the numbers we saw reported on Wednesday and Thursday where 2/3 of the companies who still report monthly sales numbers missed expectations by an average of 450bps (240bps if you exclude CATO). Not only that, but every company with the exception of BKE and ZUMZ posted a sequential decline on the 2yr trend line. The average decline for the 7 companies equaled 320bps.

We looked at the regional weighting for each retailer to see if there was any geographic areas that made it through February in a healthy position. It's hard to give any part of the country the benefit of the doubt when GPS reported a -4% against a -7% LY, but based on what we found it looks like the South and MidWest were hit hardest. We'd add the East Coast in there as well even though there was no company with a bias to that region because we've been trudging through the snow here in CT for the better part of 6 weeks.

We have 1 more month of easy compares until comps get more difficult starting in April. Cheap gas has been a tailwind YTD, but we should point out that the average price for a regular gallon of gas is up about 12% since the first week of January according to the EIA and the YY growth rate is 460bps behind where it was when January kicked off.

On the positive side, employment numbers looked good this morning and averages wages ticked up another 20bps. That could continue to help especially on the lower end, but it appears for now that weather is winning the battle.

OTHER NEWS

Ports Gridlock Reshapes the Supply Chain

(http://www.wsj.com/articles/ports-gridlock-reshapes-the-supply-chain-1425567704)

Sephora in big omnichannel push: beacons, in-store augmented reality and more

LL - Senator calls for Lumber Liquidators investigation

(http://www.chainstoreage.com/article/senator-calls-lumber-liquidators-investigation)

APP - American Apparel workers create coalition

(http://www.chainstoreage.com/article/american-apparel-workers-create-coalition)

Bonobos to open 4,000-sq.-ft. flagship in Manhattan

(http://www.chainstoreage.com/article/bonobos-open-4000-sq-ft-flagship-manhattan)

COST - Exclusive: Costco working to end use of human antibiotics in chicken

(http://in.reuters.com/article/2015/03/06/us-costco-antibiotics-idINKBN0M201520150306)