This note was originally published at 8am on February 20, 2015 for Hedgeye subscribers.

"You can’t expect the Fed to spell out what it’s going to do...because it doesn’t know."

-Stanley Fischer, Fed vice chair

The economy is like a pendulum. It oscillates above and below productivity growth but never really falls exactly on center.

“Potential Output” and “NAIRU” (non-accelerating inflation rate of unemployment) are nice theoretical constructs and are helpful in conceptualizing a tractable macroeconomic framework but they can’t actually be measured with precision and can only be approximated after the fact.

Fascinatingly, despite the abject amorphousness and immeasurability of those concepts, the perceived real-time state of the macroeconomy relative to them remains central to the Fed’s policy calculus.

Policy makers often play the role of antagonist in our daily strategy narratives but, in truth, we don’t particularly envy their challenge.

Consider the following middle school riddle:

Q: How far can you walk into a forest?

A: Halfway – after that you are walking out of the forest.

Macro policy making can be similarly enigmatic. Policy makers generally know the correct direction to take (easing/tightening) but don’t necessarily know how big the forest is (the output gap) and the mapping tools (models) used for orienting oneself inside the forest to understand where you are and how far you’ve actually gone are underdeveloped…oh, and the forest isn’t static – it’s dynamic (subject to global/exogenous shocks), reflexive (policy action itself perturbs the system) and changes shape and size as you try to walk through it.

A perennial problem faced by policy makers is determining whether short-run deviations from potential (remember: the macro pendulum is always above/below potential & we don’t actually know the value of “potential”) represent a transient dislocation amenable to policy action and transition dynamics or if potential output/growth itself has changed. Discerning which scenario correctly reflects the underlying reality is critical as the appropriate policy prescriptions can be antithetic.

The post-crisis period has only added an exclamatory emphasis to Fischer’s characterization of the Fed’s limited capacity to convictedly forecast macrofundamental changes over any extended period. Indeed, in the wake of the Great Recession, what were once decreed macroeconomic “Laws” were downgraded to “Guidelines” and then further decremented to something akin to “conceptual guideposts”.

To review some of the notables:

Curve-balls ….

Phillips Curve: The Phillips Curve – which can also be viewed as the aggregate supply curve in the vaunted AD/AS macro model - relates the change in the inflation rate to the level of short-run economic activity. Here, a negative output gap drives a negative change in the rate of inflation and a positive output gap drives a positive increase in the rate of inflation. The idea is compelling, intuitively appealing, and holds up fairly well historically. However, as Larry Summers has been apt to highlight, the relationship has failed to hold more recently: “inflation did not decelerate by much even a few years ago when unemployment was in the range of 10 percent. Nor was there much evidence of accelerating inflation in the 1990s, when the unemployment rate fell below 4 percent. “

This breakdown in the output-inflation link is important. The conventional view is that the level of output drives inflation which, in turn, drives the policy response. A structural break in the output-inflation connection leaves policy without its proverbial North Star.

Law & (Dis)order ….

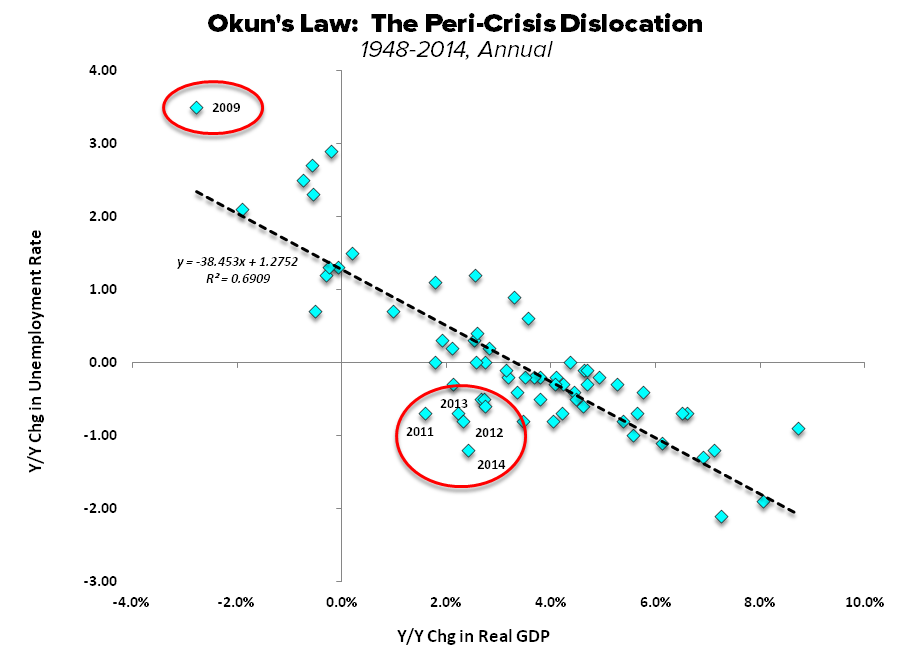

Okun’s Law: Okun’s Law – named for Kennedy economic advisor Arthur Okun - links the growth rate of output to changes in the unemployment rate and says that short-run output needs to grow ~2.25% above trend to reduce unemployment by 1%. Historically, the relationship has been strong with ~70% of the annual change in unemployment explained by the change in GDP growth. In the Chart of the Day below we show Okun’s Law on an annual basis over the 1948-2014 period. We’ve highlighted the large dispersion/break from trend in the peri and post-crises period with unemployment spiking higher than predicted by the model in 2009/10 and subsequently falling faster than predicted over the 2011-14 period.

Secular and structural changes in the economy and labor market have certainly shifted the relationship over the last 65 years and the Great Recession served to bring those changes further into focus. But that’s also largely the point. If the forecast error in a workhouse macro model such as Okun’s Law rises to such an extent that its practical utility is lost when it’s needed most, the conventionalist forecaster’s tackle box gets increasingly bare.

Rules & Tools ….

Conventional expansionary policy works to increase investment (& export) demand by expanding the spread between the marginal product of capital and the real interest rate. This works well over “normal” cycles and particularly well on the right side of an interest rate cycle (think 1983-2008) when decades of lower highs and lower lows in both real and nominal rates support recurrent layering of debt augmented demand and asset price inflation.

Conventional policy breaks down in a demand vacuum perpetuated by the long-term rate cycle reaching its terminal end. In short, no one cares if the real interest rate is below the marginal product of capital if there is no demand for the output you produce using that newly purchased “cheap” capital.

Mo’ Money, Mo’…. Inflation?

But #StrongDollar is sweet, right?... Lower gas prices, higher share of wallet for other discretionary purchases, cheaper imports, stronger intermediate-term domestic consumption. Rising domestic demand, tightening capacity, and a taut labor market should support incremental wage and demand-pull inflation. Viva la Phillips Curve! True, but the inflationary impacts are more likely to manifest over the medium term and provided the domestic labor market remains something of an insular island of strength.

Duration Mismatch ….

In the more immediate term, an expedited appreciation of the dollar, the associated cratering in energy/commodity prices and decline in import prices drives disinflation domestically. Global deflationary pressures only exaggerate that impact.

Keepin’ it Real ….

The other side of lower inflation (besides the simple fact that it’s running at <50% of the 2% target) is rising real interest rates and the goal of expansionary policy is lower – and preferably negative - real rates. That disinflation is predominating globally and fixed investment (still) flagging with most central banks sitting on 0% six years post-crisis is not particularly comforting. Again, there are no good analogues for the current global dynamics and conventional policy efforts have been Sisyphean.

Wet Noodles & Rented Alpha ….

What do you do with this quasi-random redux of post-crisis creative destruction in conventional macro modeling?

Mostly it’s just an incremental noodle to noodle over as you noodle over the Fed’s latest noodling over lagging macro data.

More tangibly, I think it edifies Fischer’s quote above. Effective policy action, even in “normal” times is challenged by the realities of imperfect information, incomplete understanding and structural shifts unamenable to the coarse tools of monetary policy.

Those challenges have only been amplified in the post-crisis period and have only heightened the magnitude of uncertainty facing policy makers and, by extension, market participants.

Uncertainty breeds volatility and volatility breeds market dislocations. Market dislocations, however, are (still) alpha’s breeding ground. We expect the already rampant cross-asset class volatility to persist.

When I was in coaching/bodybuilding, the running punchline for steroid users with no process and marginal work ethic was that they had a “rented physique”. Great moderations, secularly depressed volatility and leverage is like rented alpha.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.79-2.15

SPX 2078-2120

VIX 13.99-18.88

USD 93.70-95.32

YEN 118.16-120.26

Oil (WTI) 49.09-53.99

Gold 1201-1232

To not being “that guy”,

Christian B. Drake

U.S. Macro Analyst