COH/SKX/DECK: Set ‘Em Up

October 19, 2009

TODAY’S CALL OUT

Here’s a look at the setup headed into this week for some key names in retail. SKX will smoke numbers, but it needs to. COH is teed up for a gross margin beat, but I don’t know if I care. DECK has tanked on every print over 4 quarters, but I don’t think it will this time.

COH (Tues am): Estimates appear reasonable, though those looking to call the bottom will be early. This company has perhaps the best setup of anyone as it relates to going up against easy Sales, GM, and SG&A compares.’ Unfortunately, that approach is as consensus as consensus can be. Increased unit sales due to lower price points sounds great -- but isn’t this a company that had a tremendous 7-year run by taking UP price point? Now why is it a good idea to undo that? Also, if you take price down 10%, guess what you need to do in order to keep revenue even… Coach’s saving grace here is that last quarter ended with its best sales/inventory spread in over 2 years. When I do the math, it sets up for a potential Gross Margin beat.

COH sentiment: The Street likes this one, with short interest in the low single digits, and 64% of ratings ‘Buy.’ The only ones not buying is management, who bought at $10, but has been absent since (stock now at $34).

SKX (Wed pm): Best fundamental setup of the week, but ‘expectations game’ matters big time. Revenue trends both accelerating in their own right as ‘Shape Ups’ continue to gain momentum, and are also going up against easy numbers vs. last year on virtually every line of the P&L and balance sheet. We’re at $0.41 vs. the Street at $0.35. Keep in mind that SKX is second only to PSS as it relates to exposure to China, and should benefit from lower sourcing costs in 2H (i.e. it should start with the numbers about to be reported). The math is working out in a way where net years’ numbers are looking low by as much as 50%. Given my massive aversion to owning this name from a quality perspective, I need to quantify potential downside six ways ‘til Sunday before I really jump on the bandwagon. For those of you that are less risk averse, this one looks good – though you may need to model something in the higher $0.40s to get to upside on the print.

SKX sentiment: With a move from $6 to $22, do you think that just MAYBE the market has figured out what I noted above? Yes, of course. If we use $1.50 in EPS as a 2010 base (Street is just shy of a buck) then we’re at 11.3x EPS today after netting out $5ps in cash. That’s fair to me. Short interest has come down to 9% -- a level not seen since Dec 2007.

DECK (Thurs pm): Let’s face some facts, it has not been fun for any DECK shareholder on the day of each of the last 4 prints – with the stock down every time at an average of -16% despite smoking the quarter every single time. I think numbers are doable, but don’t think this is a quarter where we’ll see a ‘smoke.’ I’m also not sure that’s bearish with short interest having gone from 12% to 22% over 4 months. Another fact to face… UGG is a brand that continues to work. It is not a fad, nor is it a trend. Call any buyer at Nordstrom – not even in the shoe department, but also outerwear and accessories. If you don’t have time, check out the UGG site, and then try to buy things on the site (near impossible given tight allocation and distribution). These guys did it right. It is here to stay.

DECK sentiment: So what are we looking at? A company with $8 in earnings power and $13.50 in net cash trading at $88. That’s 9.3x earnings. It also compares to COH at 15x. I’ll take the over/under on DECK.

COH SIGMA

COH SIGMA

SKX SIGMA

SKX SIGMA

DECK SIGMA

DECK SIGMA

LEVINE’S LOW DOWN

Some Notable Call Outs

- At a time when most companies remain cautious of 4Q expectations, Joes Jeans set the tone stating that it expects to top its 16% top-line growth in Q3 with an even better Q4 sending shares to the moon up 50% on Friday. It looks like Kellwood, which has been vocal about its desire to acquire a denim brand, just missed its chance at the California-based company.

- After years of investing in its online business, AEO reiterated its sales goal of $0.5Bn by the end of 2010, which would account for nearly 20% of sales – among the highest for traditional brick and mortar retailers. The company was also quick to point out its conversion rate of ~3% nearly twice the Internet average. While most retailers are in the early stages of building out their online presence, AEO is realizing double-digit growth and meaningful contributions from its efforts.

MORNING NEWS

Kathmandu to Raise as Much as A$375 Million in IPO - Kathmandu, an outdoor equipment retailer in New Zealand and Australia, plans to raise as much as A$374.9 million ($344 million) in an initial public offering, following department-store operator Myer Group in selling equity as stocks rally. Kathmandu, owned by Goldman Sachs JBWere Pty and Quadrant Private Equity, will offer shares at between A$1.65 and A$1.90 each, it said in a prospectus today. The IPO values the stock at between 13 to 15 times Kathmandu’s estimated earnings in the year that ends in July 2010. Myer, Australia’s largest department store operator, plans to raise as much as A$2.34 billion next month, tapping a local stock market that has surged 53 percent from a March low. <bloomberg.com>

Li & Fung Plans IPO For Trinity - based sourcing giant Li & Fung Group is planning to take its luxury menswear retailer Trinity public. Over the weekend, Trinity sent out an invitation to a press conference on Tuesday at which executives will outline the details of its upcoming IPO. Back in August, Li & Fung managing director William Fung declined to comment on speculation that Trinity was preparing to list on the Hong Kong stock exchange. One local newspaper had reported that Trinity was aiming to raise at least $200 million through an offer by the end of this year. Trinity operates over 300 retail stores in Greater China, including more than 30 retail stores operated through joint ventures in South Korea, Malaysia, Singapore and Thailand. <wwd.com>

Europe: Anti-dumping taxes on footwear to continue - The European Commission (EC) is proposing to extend anti-dumping duties on footwear imports from China and Vietnam for another 15 months. According to an EC document, "the anti-dumping measures on leather footwear should be maintained", which has upset many retailers who have been hoping to eliminate all taxes by the end of the year. However, the relevant EU trade committee is going to discussed this proposal before a final vote by all 27 member states in December. If the taxes - 16.5% on Chinese and 10% on Vietnamese leather footwear imports respectively - are adopted, they will take effect from January 2010 and lapse at the end of March 2011. <fashionnetasia.com>

CIT Amends Debt Offer - CIT Group Inc. on Friday amended the debt restructuring offer that began on Oct. 1 to include an acceleration of the repayment of new notes and the shortening of maturities by six months for all new notes and junior credit facilities. The company said the amended plan also increases the amount of equity offered to subordinated debt holders to reflect agreements with holders of the majority of its senior subordinated debt, and the plan now includes notes maturing after 2018 that were not previously solicited as part of the exchange offer. The exchange offers are set to expire on Oct. 29, except for the additional notes maturing after 2018, which have an early acceptance date of Oct. 29 and an expiration date of Nov. 13. <wwd.com>

Walmart Green Push Drives BASF Swapping Crackers for Lab Coats - Wal-Mart Stores Inc.’s new line of food containers made from corn starch also hold the promise of a revolution by global chemical companies including BASF SE. BASF is developing chemicals from bacteria and fungi instead of processing oil derivatives, cutting back on smokestacks that belch carbon dioxide into the atmosphere. Royal DSM NV will start a project by year-end with enzymes to produce succinic acid for car coolants. Mass production may start 2012. <bloomberg.com>

India: Textile industry hopes to create 12 million new jobs - Indian textile companies are going to generate 12 million new jobs for the country by 2010, a recent survey revealed. Generating 27% of the country's foreign exchange revenue, textile exports from India are expected to reach $50 billion by 2010 with continuous improvement in design skills and other factors. The industry is also set to meet international standards by planning to invest $5 billion in new machinery in the near future. <fashionnetasia.com>

Vietnam: New eco-tannery launched trial in Saigon - Atest run has recently been successfully completed at ISA Tan Tec’s new eco-tannery in Saigon, Vietnam. Company founder and managing director Tom Schneider said: "Our planners, technicians and builders have all worked incredibly hard. The test run has already made it clear that the quality of the products we make in Saigon is outstanding. We will more than meet our extremely ambitious targets for energy and water consumption."The leather produced at the new tannery uses 35% less energy and 50% less water than is required compared with the industry average. <fashionnetasia.com>

Room for Growth Seen in China's Smaller Cities - Investment organizations and multinational companies are plotting their expansion in China’s third- and fourth-tier cities, according to a new report from Asian marketing company Bates 141. While the first- and second-tier cities such as Beijing, Shanghai and Guangzhou are over saturated, some 4,000 smaller cities still have plenty of growing room for consumer companies, according to the study. These cities are home to 55 percent of China’s population. According to China’s National Bureau of Statistics, consumer retail spending in China’s regional cities in 2008 stood at 3.48 trillion yuan, or about $511 billion at exchange rates at that time. That figure compares to 1.84 trillion yuan, or $223 billion, for 2004. Bates 141 conducted interviews with consumers in eight regional cities throughout 2008 and 2009 to better understand their buying habits. According to the report, those living in rural areas evaluate and identify brands by quality assurance, reputation and real life experience. <wwd.com>

Jimmy Choo to Accessorize H&M - Fond of glamorous, oversize sunglasses and sky-high stiletto boots, Tamara Mellon is not a person one would associate with the word “bargain.” And dressed head to toe in an ultraviolet suede minidress and strappy sandals from the Jimmy Choo for H&M capsule collection, Mellon, founder and president of the luxury shoemaker, admitted: “It was a challenge for us to create high-quality pieces at an H&M price point.” The Jimmy Choo for H&M line, which hits some 200 H&M stores Nov. 14, is the first time the fast-fashion retailer will collaborate with an accessories brand after doing successful one-off apparel collections with the likes of Karl Lagerfeld, Stella McCartney, Viktor & Rolf, Roberto Cavalli and, most recently, Matthew Williamson. <wwd.com>

Dick's SG to Open Oregon Stores - Dick's Sporting Goods announced plans to open six new stores in Oregon, including the new Eugene location in a former Joe's Sports location in the Delta Oaks shopping center on November 8th. It will be Dick’s SG's second store in Oregon. Dick's SG will also open stores in Hillsboro, Gresham, Lake Oswego/Tualatin, Bend and Salem. It currently has one store open in Tigard, OR. <sportsonesource.com>

Gap to Open in China, Web Shop in Canada, U.K. - International expansion plans for the U.S. clothing chain Gap are in the works. The retailer will open its first store in China next year, as well as e-commerce sites in Canada and the U.K. Glenn Murphy, the company's chief executive officer, told investors last week that the chain also plans to expand its outlet store presence. Gap will return to TV in November with a new U.S. advertising campaign. A 1 percent decline in September same-store sales were reported for the Gap. The Old Navy brand, which saw a 13 percent increase in September same-store sales, will see the unveiling of a new store design in nearly 50 stores by the end of the year. In September 2008, Old Navy had seen a 24 percent decline in same-stores sales <licensemag.com>

U.S. Retail Sales Rebound Into Xmas as Shares Show Consumer Not Dead - From Intel Corp. to TJX Cos., it’s beginning to look a lot like the retail holiday season will be happier than forecast. Intel, the world’s biggest chipmaker, cited stronger consumer demand in projecting Oct. 13 that its sales in the fourth quarter would be $9.7 billion to $10.5 billion, compared with a $9.5 billion average prediction in a Bloomberg News survey. TJX, the Framingham, Massachusetts-based operator of clothing-store chains T.J. Maxx and Marshalls, raised its fourth-quarter comparable-sales estimate Oct. 8 to a gain of 3 percent to 5 percent from an increase of 2 percent to 4 percent. <bloomberg.com>

London September Retail Sales Rose the Most in a Year, BRC Says - London retail sales rose the most in more than a year in September as warmer weather encouraged people to go shopping, the British Retail Consortium said. Same store sales gained 7.5 percent, the group said today in London. Middle Eastern investors returned after Ramadan, and the pound’s weakness against the euro continued to attract western Europeans, the BRC said in a statement. <bloomberg.com>

Hugo Boss in Union Talks Over Cleveland Factory - Six months after union officials said Hugo Boss intended to close its Cleveland suit factory, and with it cut hundreds of jobs, the company has reversed its thinking and confirmed it is negotiating with the plant’s union, Workers United. A new contract could extend the jobs for the factory’s 400 workers, 320 of which are union members. The facility, which has served as the center of Boss’ American suit production for 20 years, produces 150,000 sleeves annually.

<wwd.com>

Martha Stewart, Kmart Part Ways - Sears Holdings and Martha Stewart Living Omnimedia have ended their long-standing relationship. Martha Stewart issued a statement late Friday, indicating that the Kmart deal, which ends in January, was unable to be renewed.In September, Stewart landed a deal with Home Depot for a line of Martha Stewart Living-branded home improvement products. The line will hit U.S. Home Depot stores in January, followed by Canada in February. <licensemag.com>

JJB shareholder sells 22 million shares - Crystal Amber Fund, one of JJB Sport’s largest shareholders, has divested over half of its shares in the sportswear retailer but will support the proposed capital raising.

Crystal Amber sold 22 million JJB Sports shares on Friday. It now has a 5.45% stake in the company.

Crystal Amber chairman William Collins said: “We have been actively involved with recent developments at JJB and welcome the proposed fundraising. <drapersonline.com>

Lotte Said to Acquire Control of China’s Times, Beating Wumart - Lotte Shopping Co., South Korea’s biggest department-store owner, agreed to buy control of Times Ltd. to gain 66 outlets in China, beating Wumart Stores Inc., two people with knowledge of the matter said. In a deal valuing Times at about $625 million, Seoul-based Lotte Shopping will purchase a 72.3 percent stake in Times from Chairman Kenneth Fang for about HK$5.50 per share and will make an offer for the rest of the company, the people said, asking not to be identified because the talks are private. The offer is 19 percent higher than Times’s last traded price. <bloomberg.com>

RESEARCH EDGE PORTFOLIO: (Comments by Keith McCullough): KR

10/16/2009 03:28 PM

SHORTING KR $24.70

See Levine's notes on the SWY quarter. It looks like someone has (or thinks they have) material information on KR that we definitely don't have! Shorting that speculation high. KM

TRADING CALL OUTS

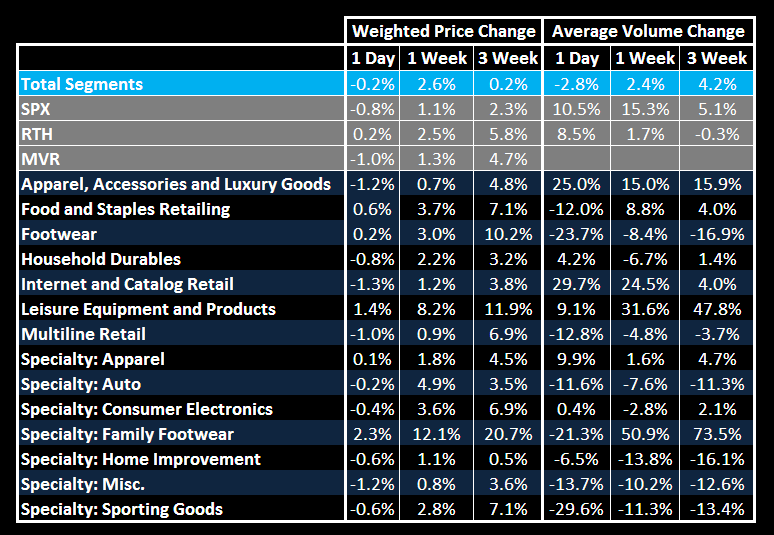

As we often say at Research Edge, prices don’t lie. The market is always telling us something. Here are some names that are showing outside movements relative to the market, peers, and volume trends...

- Apparel, accessories, and luxury goods and internet and catalogue retailers underperformed the market on positive volume.

- Family footwear and leisure equipment and products outperformed the market.

- DSW led family footwear retailers up with strong volume for the week after preannouncing earnings double that of the street's expectations, BWS got a free ride.

- SKX has been making significant gains over the last three weeks on positive volume leading into earnings on Wednesday which are expected to best the street by a significant margin.

- ZQK and CMRG took losses across all three durations on positive volume.

- The top losers of Friday were dominated by apparel companies and household durables.

- COLM is trading up into Thursday's earnings on strong volume indicating that the quarter could be better than expected.