Conclusion: We think that KATE should be bought on Thursday’s sell-off, which was spurred by concerns about 1Q comp trends after KATE hosted a meeting with investors. This company has all the credibility in the world executing on its business model, but not in guiding the Street. Quite frankly (and perhaps over optimistically) we’d have thought the market would start to see through the KATE guidance gauntlet. We think its guidance is conservative, and the Street’s interpretation even more so. More often than not, these communication bubbles create a great opportunity to buy a fantastic long-term story. This is one of those opportunities. Though this note focuses almost entirely on the 1Q comp number, the real call (including 1Q) is a roadmap to a $75 stock.

FULL DETAILS

Today KATE did what KATE does, traded down significantly on information that we think is misleading. Specifically, a group of investors visited management, which resulted in a broker issuing a 1Q comp forecast of +3.5%. We don’t think anyone fabricated information out of thin air. Chances are (and we spoke with several people in attendance) the company gave tangible reasons why comps will start of the year soft, and we think that the ensuing report took an even more cautious posture on management’s assertions. We simply don’t believe either of them.

We hate to play the guidance game – and most people who know us know we usually look through most of it as noise. But let’s strap the accountability pants on for KATE management…

- At the beginning of 2014 it guided to 10-13% comp, and ultimately came in at 24% for the full year.

- KATE said it would start out last year comping in the high-teens, and it printed 29% six weeks later in 1Q.

- In 4Q KATE guided to 8-14%, and put up a 28%.

We’re going to go through the puts and takes below, but keep in mind that this is a company where you have to watch what they do, not what they say. They don’t have the communication thing down pat, but the company can execute on a world class business plan with the best of ‘em. That’s what matters.

Also… let’s keep one thing in mind – it was just last week that KATE printed the best comp in all of retail – or 28% on top of a 30% comp in the prior year. And now it is going to slow to 3.5%? Heck, e-commerce alone should get the brand above a 6% comp (it’s about 20% of the business and grew in 4Q at better than 50%). If the company is going to put up a 2,500bp deceleration on the 1 and 2-year comp, then the stock SHOULD sell off – probably a lot more than it did today – and doesn’t deserve its current valuation.

But we think KATE definitely deserves it, and then some. We’re modeling 10% in the upcoming quarter, and 18% for the full year. We’re getting plenty of hate mail for ‘disagreeing with the company’ and setting an unrealistic hurdle rate. But we didn’t just pick 10% out of the air. Below we go through all the puts and takes on factors including e-commerce, flash sales, Japan, FX, Saturday/Jack Spade, and inventory positioning.

Despite all the real estate in this note dedicated to a singular comp number in the seasonally least important revenue quarter of the year, the focus for us is still on the BIG call, which is $3 in earnings power as the brand footprint doubles over 3-4 years and EBIT margins go from 11% to 19% -- and that story plays out starting today.

What’s It Worth? So that begs the question as to what we should pay for KATE. By the end of this year, we’ll be eyeing about $345mm in EBITDA and $1.30 in EPS. When looking at the 50% and 100% growth rates in EBITDA and EPS, respectively, we could definitely argue a big multiple. On the flip side, this is a fashion business, and there will almost certainly be a time (like KORS is experiencing now) where it will see multiple compression as it matures. But keep in mind that KORS has a brand footprint of $6.4bn and EBIT margins of 30%. KATE has a $1.4bn footprint (smaller that Tory Burch at $1.9bn) and margins of only 11%. It will be a long time before we have to ask the ‘is it over’ question. Until then, we think the multiple will continue to defy gravity in the eyes of anyone that’s not a growth investor.

For argument’s sake, let’s keep the forward multiples in place that KATE has today – 50x earnings and 19x EBITDA. We think that there’s upside this year as the company beats. But on 2016 numbers we’re looking at 50x $1.32 = $66, or 19x EBITDA in the mid 50s. Roll ‘em to ’17 and you get to over $2+ in earnings power, or around a $75 stock.

HERE ARE SOME OF THE KEY FACTORS AS IT RELATES TO THE 1Q COMP

E-commerce

The company cites a reduction in flash sales as the main driver of the sales pullback in the year. For the record, management said the same thing last year during the 4th quarter where they turned a flash sale into a theme sale, and dot.com comps were up 45%-55% in the quarter.

We checked the e-mail archives and counted 6 major promotional campaigns during the first quarter of last year. 3 were flash sales, which occurred on: 1/22, 3/18, and 4/4. With one 3 day ‘Friends and Family’ event that kicked off on the 2nd to last day of the quarter.

To date KATE has done one flash sale on 2/10/15, right in line with when it appeared last year. It didn’t repeat the first 1-day bag specific event of the year, but as you can see later, it didn’t have a negative impact on traffic flow. We’ll be tracking each promotional event as the quarter progresses to see if they follow the same March playbook. The thing we don’t know is the velocity or overall product availability. That could cause some fluctuation in overall sales, but we don’t suspect a big divergence from last year.

Lastly, KATE launched its e-comm operation in England during the 4th quarter. That should have positive implications as the business builds and awareness grows into 1Q.

Visitation

The first chart below shows the year over year change in traffic rank. Directionally we’ve found it to be a very good indicator of the overall health of a company’s online business. It takes into account 2 metrics (unique visitation and page views/user) and tracks each URL in relation the internet in aggregate. KATE’s rank has pulled back over the past few weeks, which is what we expected (as business slows seasonally after holiday and before Easter), but still sits +38% YY. For reference the trough in the chart below corresponded with 3Q when dot.com put up its lowest growth rate of the year at 21%.

![]()

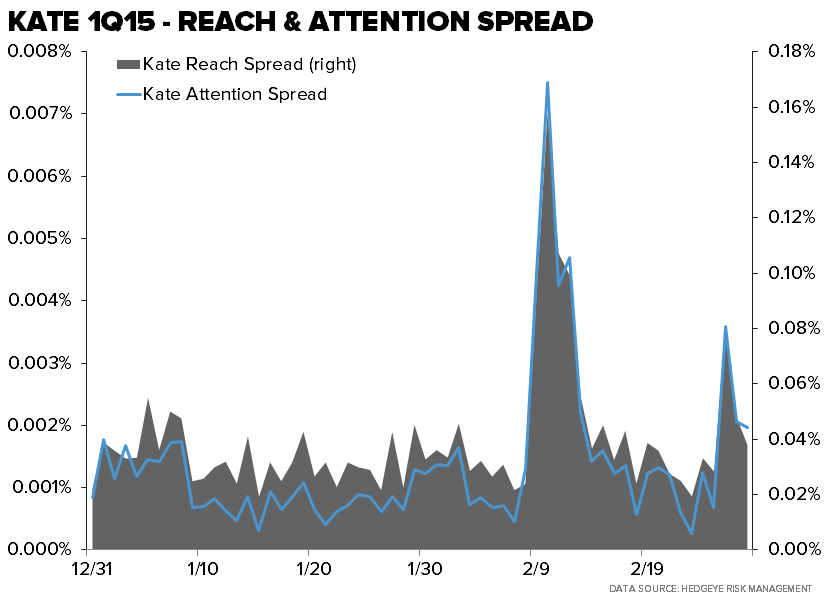

If we look at visitation at a much more granular level, we see the same type of trend. Chart below looks at the reach spread and attention spread from 12/31/14-2/28/15. Here reach is defined as the percent of total users on the internet visiting a site on a given day and attention is the amount of time spent on the internet dedicated to a specific URL on a given day. The spread is calculated by taking this year’s reading minus last years, each day corresponds with the appropriate calendar day from LY. Anything North of the x-axis is positive. Anything south is negative. Overall the trend has been decidedly positive. With the big spike in February corresponding with the ‘Flash Sale’.

If we compare that to what we saw during the 4th quarter where there was 2 ‘Flash Sales’ and 1 ‘Theme Sale’ the trend looks very healthy.

Japan

Japan is one of the moving parts to the comp story here. Overall it is about $135mm-$165mm in revenue, or 12-15% of total. There are some puts and takes as it relates to the impact on comp that should be considered.

Japan was added to the comp base in the 1st quarter of last year. And it came out of the gates hot comping +37% (44% if you include the impact of the extra week). Some of that was driven in part by the nation-wide hike in consumption tax from 5-8%. But if we look at the trend in that business, comps accelerated to +25% in the 4th quarter on top of a +19% last year. Currency could be a headwind, but management noted on the call that the a) inventory is 75%-80% hedged for the year, and b) the Yen has only deprecated 200bps since the end of last quarter.

- Let’s say that comps in quarter are flat, which would imply a 300bps deceleration on the 2yr trend line, and sales growth for the rest of the company was 20%. We are looking at 360bps of headwind to the company average. Or, bear case, Japan is down 10% we are looking at 540bps of dilution.

- Realistically, let’s assume that the 2-year run rate stays even with 4Q levels – even though it is actually trending higher. A 6% Japan comp would imply a 22% 2-year trend. That suggests 250bps of sequential headwind on a consolidated basis.

Kate Spade Saturday could cause a slight disruption, but guidance doesn’t assume any effect from the closure. Relative to the size of distribution in the country (KSS and Jack Spade represent about 15% of the distribution in Japan assuming wholesale and retail doors increased by 15% this year) Saturday could curb some demand. But we think it’s important to remember a) these stores are in their infancy with the majority of doors still within a year of the open date, b) brand recognition is still extremely low, and c) there is a reason management shuttered the retail operation.

Inventory

KATE inventory was up 16% to end the year compared to +46% last year. The consolidated balance sheets don’t reflect that because of the divestitures of Juicy and Lucky. But, a lot of that was due to excess inventory in the Jack/Saturday lines. The company took a 240 basis point hit to liquidate the 2013 Kate Spade Saturday launch year inventory in the 2nd quarter and cost the company ~$6.4mm. And it took another $8.6 million hit in 4Q from. Adjusting for that, inventories should be in-line to support the top-line growth we are modeling. Port closures are an issue, but KATE who will do just north of $250mm in the quarter should be nimble enough to accommodate.

Easter

Due to the calendar last year, Easter was pushed back to 4/20/14, compared to 3/31/13. It’s likely that some of the sales that would have been pushed into 2Q of last year were pulled forward due to targeted promotions. We think that’s extremely hard to quantify, but we’ll give them the benefit of the doubt. This year’s Easter falls on 4/5/14. One day after the quarter closes and should be good for a point or two of comp.