UA: How Have Expectations Changed?

Expectations are growing less apocalyptic, though the fundamental story is shaping up as it should. The one factor that could derail near-term earnings (SG&A spend around footwear) is the biggest revenue catalyst for 2010.

UA has been one of our favorites for most of 2009. As we do with all of our ideas, we step back daily, re-evaluate the facts, and see how reality does (or does not) synch with expectations. The bottom line is that this is still one of our favorites, and the only thing that has changed since we rolled out our Under Armour Black Book is 1) the price has gone up, and 2) evidence that the story is, in fact, playing out with the company’s fundamentals. As quantified in our report, we still believe that next 2-years’ estimates are low by 15% and 25%, respectively. Looking at this on an EV/Total Addressable Market Value basis, we still think that there’s no cheaper stock in Consumer Discretionary.

But looking into the quarter, what we won’t do, however, is turn a blind eye to changes in near-term expectations. Over the last month, consensus 3Q revenue growth forecasts have risen to 6-7%, about in line with our model. Though we still think that the Street is off with margin estimates, now we’re looking at around 7% EPS upside instead of the 10-12% we had after the last print. Also, while this name remains very much hated (only 2 of 20 Analysts have it rated ‘Buy’) short interest has come down to around 20% of the float (still understated, we think given certain long term holders that won’t sell), Is sentiment ugly? Yes. But it has grown somewhat less apocalyptic as the stock has more than doubled off its low.

So what could UA do or say on Oct 27th to change the thesis? Over an intermediate-term (and certainly a long-term) duration I don’t think there’s much that can slow this beast down. Over the near-term, we’d have to see either a meaningful slowdown in core apparel, or UA back off of footwear goals. We have 13 weeks of POS data under our belt, and the trends look good for UA. Tack that onto in-line inventories at the end of last quarter, and it smells fine by me – especially with 4Q starting off on a positive note as it relates to apparel growth industrywide.

As for footwear, the biggest and baddest thing the company can do is have Gene McCarthy get on the conference call and talk about how he is hiring 50 people to fill out his new footwear organization, which will take up the SG&A base this year.

Is this possible? Yes, very (as stated in our Black Book), and will make my EBIT numbers be too high. But the other numbers it will make unrealistic are my 2010 revenue numbers for footwear – they’ll prove too low. You see… this guy ‘gets it.’ How many times have we heard companies like Columbia Sportswear talk about ‘hiring a new footwear guy’ to solve their ills and capitalize on a ‘great brand opportunity’? Something that is consistently ‘a great brand opportunity’ but is never realized is not really an opportunity afterall…

McCarthy went in to Plank’s org chart with the understanding that he would build out his talent pool. Note that he started to do this with TBL’s Authentic Youth biz – and it started to work immediately. Then they made him Co-President of the company, did not back fill his efforts in the Authentic Youth segment and pulled resources accordingly in that area.

Simply put, the ‘rock star’ approach does not work here. It takes a team, and McCarthy will build it. If people freak out because of higher spending to get this team built – then this will be a gift for a risk manager.

Revenue Analysis

Historically, the correlation between reported UA wholesale apparel revenue and the corresponding Sportscan athletic apparel data (lagged by one full quarter to account for wholesale to retail timing) is 76% based on analysis of the last 12 quarters.

With the benefit of the late 1Q09 launch of running shoes, footwear revenues are forecast to benefit from an incremental $15 million in the quarter. We’re assuming the legacy footwear base (cleats & trainers) will decline by 30% to ~$9 million due in part to difficult comparisons and insight we’re gleaning from the channel. On the whole, we are modeling 85% growth in footwear during Q3. While revenues are still challenging to pinpoint with a high degree of accuracy given the lack of history for running, we believe the directional trends highlighted in the weekly scan data support our estimates.

Furthermore, while running and additional category expansion in footwear remains key to our longer-term thesis, we’ve got to keep in mind that we are still in the very early stages of the footwear maturation curve. Anecdotally, in a recent meeting with Dick’s management, they candidly discussed their surprise that UA’s footwear launch was met with such mixed reviews, and that it met their launch expectations.

Take a look at the chart below depicting the historical relationship (spread) between UA reported results and Sportscan trend data. It’s important to note that over the last four quarters the spread has been within a +/- 5% range, reflecting a fairly high degree of correlation.

Margin Analysis

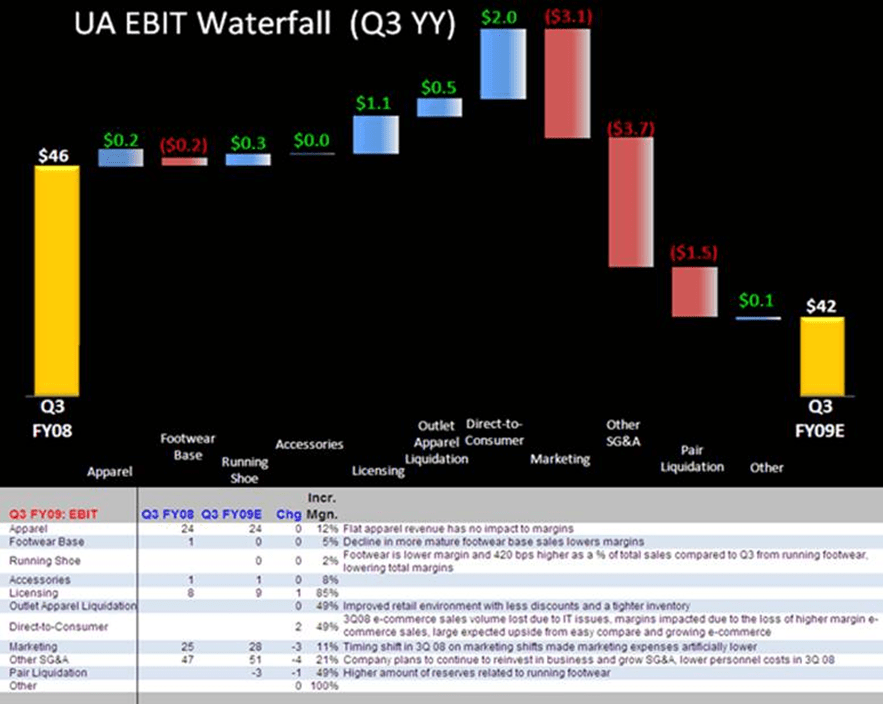

Despite a smaller portion of lower margin footwear sales compared to the 1H, higher reserves, and increased liquidation activity will weigh on margins, which we are modeling down 200bps in Q3. Offsets will include strong higher margin direct-to-consumer sales that were impacted by ~100bps last year related to IT interruptions as well as fewer discounts in the outlets for apparel liquidation due to tighter inventories and a more stabilized retail environment. In addition, product costs are starting to swing the other way, which could lead to upside. At the same time while UA will continue to invest in the brand growing SG&A roughly in-line with revenues, we expect modest deleverage of 90bps in the quarter as the company manages costs while the top-line recovers.