Editor's note: This is an excerpt from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. Click here to subscribe today.

To review why I kept these “SELL” ideas on versus others:

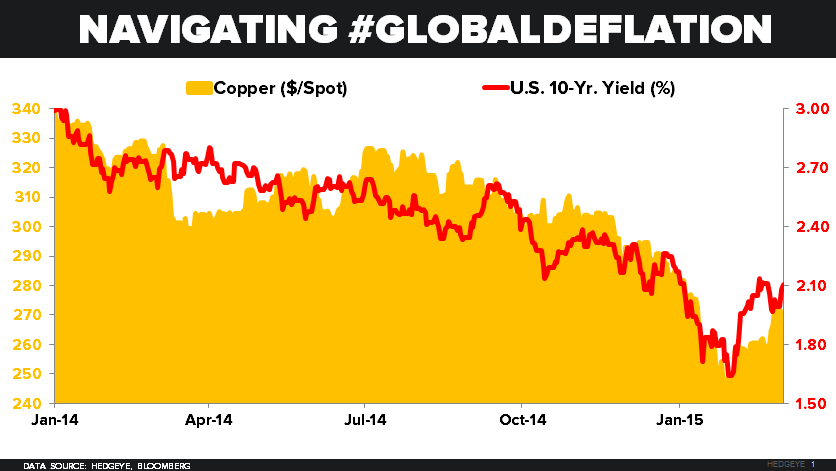

- Copper – down -1.6% this a.m. (-6.4% YTD) remains one of the most obvious ways to play our top theme, Global #Deflation

- JPM – down -1.3% YTD is in 1 of the 2 US Equity Sector Styles I like the least (Financials – sector ETF -0.8% YTD in an up tape)

- FL – down 2 cents YTD is on our Best Ideas SELL list (Brian McGough is the analyst, ask our team for his deck for details)