Position: Long Germany via EWG

Although rear-view, it’s worth looking at today’s Eurozone trade balance release as a preview of the impact that a strong Euro is having — exports were down 5.8% in August month-over-month, with imports declining 1.3%, dropping the trade balance to 1 Billion EUR from 6 Billion EUR in the previous month when exports rose 4.7% sequentially.

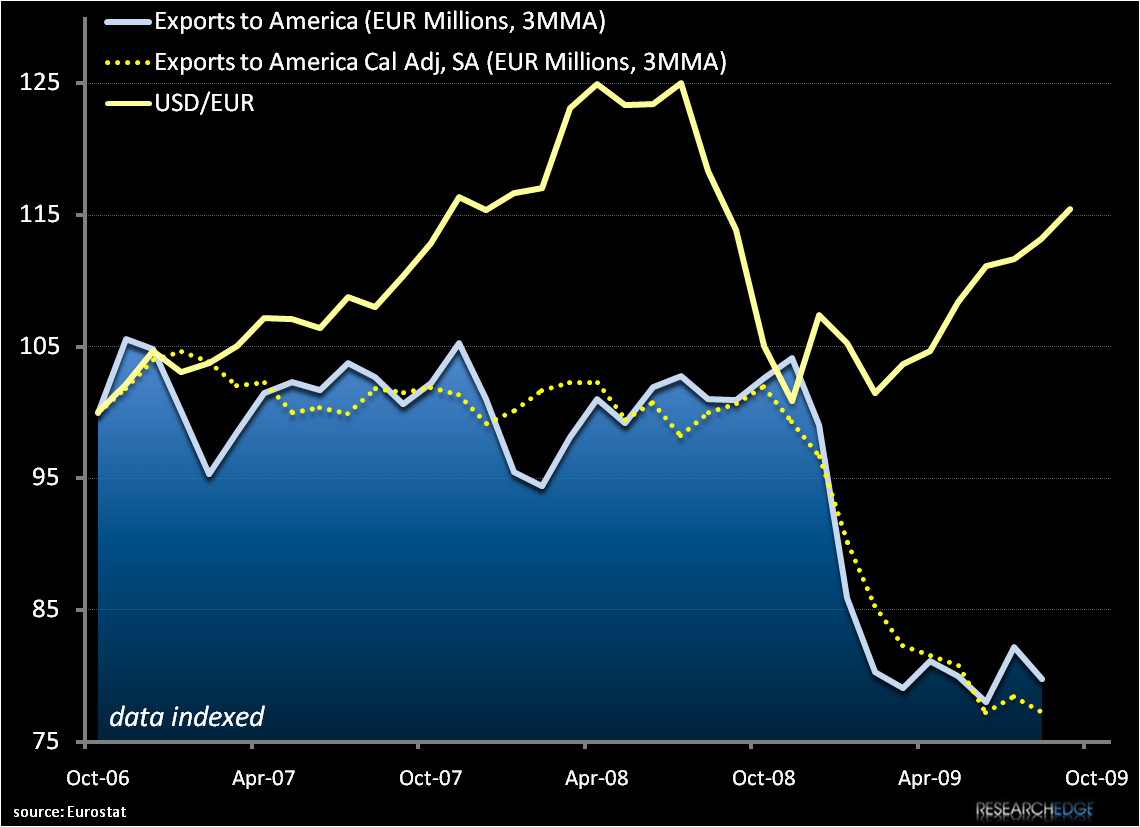

We’ve been hitting on the implications of currency strength in our European posts. With the Euro trading at an increase of +6.3% YTD versus the USD or +15.4% over the last 7 months, the impact on trade will be pronounced. As noted in yesterday’s post, ECB President Trichet has recently signaled his displeasure with a strong Euro, yet has not made explicit comments on raising rates in the near term.

In order of absolute EUR of trade, exports from the Eurozone in the first seven months this year versus a year earlier declined to the UK by 26%, followed by a -20% contraction to the US, and declines of 10% and 4% to Switzerland and China respectively, according to Eurostat.

We continue to monitor the Euro versus major currencies. Certainly for Germany’s export-led economy, a strong Euro is a major headwind. Today’s report shows that from January-July 2009 versus a year prior Germany far exceed any other country in the EU with a trade surplus of 73.4 Bill EUR, followed by Ireland (+23.3 Bill EUR) and the Netherlands (+20.9 Bill EUR). Conversely the UK far exceeded any other country with a trade deficit of -54.4 Bill EUR over the same period, followed by France (-30.4 Bill EUR) and Spain (-26.9 Bill EUR).

We’ll have our EYE on the Euro and its impact on trade, especially as it relates to Germany, which we’re currently long in our model portfolio.

Matthew Hedrick

Analyst