“There’s no ‘I’ in team. There’s a ‘me’ though, if you jumble it up.”

-Dr. Gregory House

Sometimes pretending you’re a cynical, misanthropic drug-addict doctor with deific deductive dexterity is what it takes to stay excited about staring at your screen for 14 hours a day.

The Dr. House metaphor is both apt and easy as it relates to the Hedgeye Housing teams (@HedgeyeFIG & me) inquisition for industry research alpha.

Distilling the convoluted milieu of domestic housing data in the attempt to diagnose and front-run positive and negative dispersions from industry homeostasis holds obvious parallels to the challenges inherent to diagnosing physiological pathology in the attempt to front-run … death.

Plus..you know..it illustrates our marginal cleverness with the whole “House” reference.

Anyway, after being on the right side of the acute housing demand infarction in 2014, we reversed our diagnosis for 2015 in November of last year alongside our expectation for a recession and reversal in many of the industries underlying maladies.

Since much of what we like about 2015 is what we didn’t like about 2014, juxtaposing the two years across a selection of key factors should sufficiently capture the core of our call.

HPI | 2nd Derivative Trends Matter: Housing demand leads home price growth and housing stocks follow the slope of price growth. Since 2008 the correlation between housing equities and the year-over-year rate of change in HPI has been 0.90.

- 2014: Home price growth decelerated sharply in 2014, slowing from ~12% YoY in February to ~5% in October according to CoreLogic data. The housing complex (XHB/ITB) underperformed the market by ~15% alongside that expedited deceleration in HPI.

- 2015: Home price growth stabilized in Oct/Nov across all three of the primary price series (CoreLogic, Case-Shiller, FHFA) and have, in fact, shown modest re-acceleration in December. Performance has again followed suit with the XHB and ITB outperforming the SPX by +12% and +10%, respectively, since the 2nd derivative HPI stabilization began in November. Ongoing inventory tightness, with months of supply on the existing market holding below 5 months, remains supportive of stable to improving price growth trends over the immediate/intermediate term.

Net: In the Chart of the Day below we show the inflection in housing equity performance following the 2nd derivative inflection in HPI.

Credit: Discrete tightening in 2014 gives way to marginal easing in 2015

- 2014 Contraction: The implementation of QM regulations, FHA loan limit reductions and the expiration of the Mortgage Forgiveness Debt Relief Act collectively served to constrict the credit box and capsize housing demand in 2014.

- 2015 Credit Box Re-Expansion: Recognizing the discrete drag on the housing recovery, regulatory policy momentum is shifting away from the over-pricing risk for the current wave of would-be borrowers and towards policy adjustments aimed at improving affordability and modest credit box expansion.

- FHA & Fannie/Freddie: FHA premium cost reductions (from 1.35% to 0.85%) implemented in January along with the re-introduction of 3% down payment loan options from the GSEs for 1st time buyers could boost purchase demand by ~3% over the intermediate term.

- Vantage Scoring: The FHFA is currently considering adoption of Vantage Scoring – a credit scoring system which provides a more comprehensive risk scoring framework than conventional FICO models and is capable of scoring thin file consumers previously locked out by FICO and other conventional models. Vantage Score 3.0 is estimated to score approximately 30-35mm more consumers than conventional models and could bring ~500K more borrowers into the fold in the coming years under conservative assumptions.

Net: Growth by the stacking of marginal easings in 2015, while likely to be modest-to-moderate, stands in sharp contrast to the restrictive QM/Loan limit reductions that headlined the regulatory environment in 2014.

Ball Under Water: The Illusion and the Inflection

- 2012-2014 | False Perceptions: Since the start of 2011 there have been ~5.3mn net, new households formed which, using a historically consistent scalar, require 7.2mn new housing units. However, there have been just 2.97mn housing units started, resulting in a cumulative supply-demand gap of approx 4.2mn units. This math has underpinned the bullish ball-under-water housing demand/construction thesis for the better part of last two years. The misunderstanding has been rooted in the reality that the imbalance has been largely illusory as the number of shared households have increased by over 3.4mn over the same period.

- 2015: Bear Market in Basement Dwelling: The increase in shared households slowed markedly in 2014 and the bottom in “basement dwelling” and headship rates now appears to be in. The implication of an inflection in shared household growth is that what has here-to been a perceived ball underwater becomes, in fact, a real ball underwater and a true support to new housing unit construction.

Rates: Rates are currently running ~40bps below their 2014 average, providing an approximate 4% boost to affordability. With global growth slowing, disinflation/deflation predominating and DM yields anchoring the long-end, we don’t see acute upside risks to bond yields in the immediate/intermediate term.

Elsewhere Across Housing Macro: Residential Construction Employment in January saw its largest sequential gain since November of 2005, employment growth across the key 20-35 YOA demographic continues to accelerate and Consumer Sentiment around housing – as measured by the University of Michigan’s “Good Time to Buy a Home” index – continues to advance alongside the broader rise in Consumer Confidence and ongoing improvement in the domestic labor market. Further, the latest CPS/HVS survey estimated that the total number of households grew by 2.0MM in December vs a year earlier, the largest yearly change since July 2005 and the first material acceleration in year-over-year growth in 8 years.

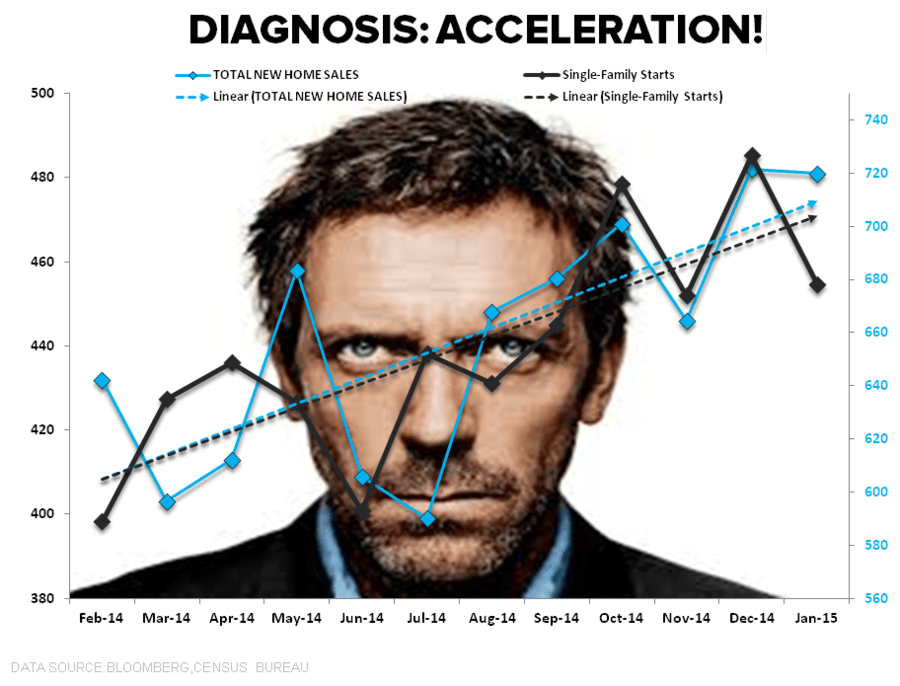

The 2015 Score | RoC Solid: Mortgage Purchase Applications were up +9.8% in the latest week marking the fastest rate of growth since June of 2013, Pending Home Sales accelerated to their fastest rate of growth in 18 months in December (we’ll get the January data this morning), New Home Sales in January held at 7 year highs, single-family housing starts were up 16% YoY in the latest January data and home price growth is reflecting a fledgling re-acceleration.

In short, our expectation for improving rates of change across the preponderance of housing metrics in 2015 is finding positive confirmation in the early year data. Of course, cheerleading a call that’s already worked is generally a great way to top tick yourself, but we still like the intermediate term fundamental outlook. We’ll continue to let Keith risk manage the exposure in RTA.

Was any of the above analytically ingenious? Probably not, but having a process for effectively capturing, curating and contextualizing the monthly torrent of shifting housing dynamics in real-time is more than trivial for resource and time-constrained investors.

As Sherlock Holmes (the figure on which Dr. House was based) characterized his investigatory process:

“You know my method. It is founded upon the observation of trifles.” ….”It’s quite exciting, he said with a yawn”

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.84-2.08%

SPX 2091-2120

RUT 1

VIX 13.08-16.65

USD 94.01-95.45

Oil (WTI) 47.61-50.97

The risk of heart attack rises by 20% on Mondays, Enjoy the weekend.

Christian B. Drake

U.S. Macro Analyst