Our short thesis is predicated on our belief that management does not have a feasible growth algorithm. This is vital because, if we are right, an aggressive growth agenda will only come at the expense of shareholders. To get to the heart of the matter, we specifically asked the company about this seven months ago on the 2Q14 earnings call. Though we had our doubts, the answer, at the time, seemed legitimate:

Q – Howard W. Penney: Thank you for taking my question. As Matt was sort of pressing you on the performance of the current store base, can you go through what the economics are, given sort of the small number of stores in the comp store base and the total number of stores? Can you go through the economics of how you envision this unfolding – the Grille, excuse me -- how you envision this concept rolling out in terms of volumes, margins, and when you think you'll get to a fairly consistent performance? Thanks

A – Thomas J. Pennison: Sure, Howard. This is Tom. From the time we laid this out, we looked at the prototypical Grille was between $4.5 million and $6 million and we really saw a target in that $5.25 million is what our prototype was. So we target internally to be within that $5 million to $6 million AUV.

Within that AUV, we're looking to have a restaurant level EBITDA between 20% and 25%. Now, while we do have more favorable food costs, our cost of sales that our Grille gives us that was spoken to, we give a little bit of that back on our restaurant operating expenses because the lunch day-part has the labor to be a little bit higher as well as some of the premier spots we're utilizing, occupancy can be a little bit higher on that lower base, but that 20% to 25% is – we have been achieving that with the class of 2011 and 2012.

Unfortunately, we had such a large component of the Grille today is relatively new restaurants in a non-comparable group that's not fully visible yet, but we are between that 20% and 25% target for both 2011 and 2012 as well as already approaching that on a run rate with some of the 2013 openings.

Source: Bloomberg

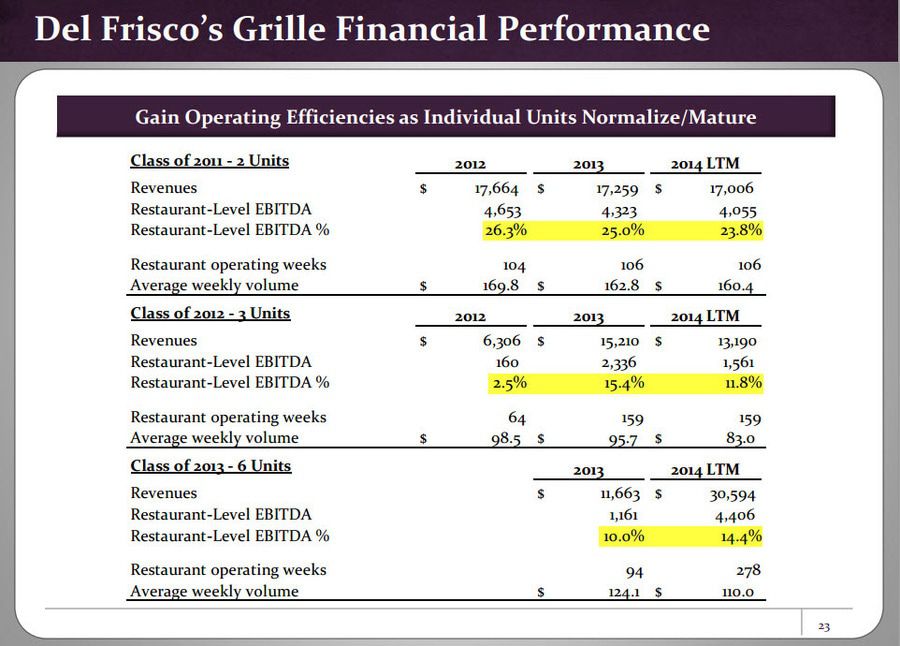

At the ICR conference this past January, management unveiled Grille margins – and they weren’t close to what they’d depicted on the 2Q14 earnings call.

Oftentimes management will say what they need to until they no longer can. If anything, this is further proof of that. But our point is – and this should be the biggest takeaway – that Del Frisco’s growth algorithm is broken and the Grille is not ready to grow at such a rapid pace. We’re trying to call out what no one else will. The facts are in the chart above. You can be the judge.