CLICK HERE for a free look at Hedgeye's Morning Macro Call for institutional subscribers. Post your questions for Keith and hear him answer live on the air.

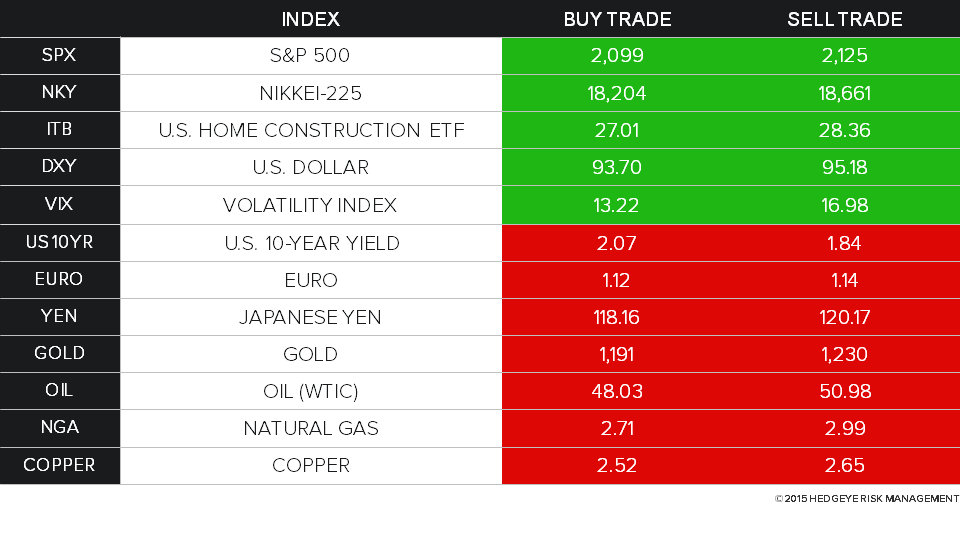

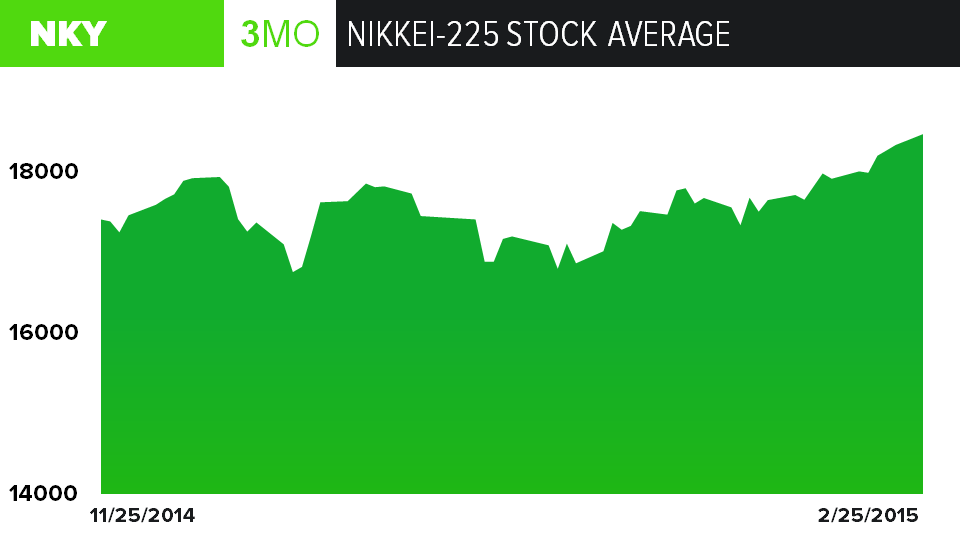

BULLISH TRENDS

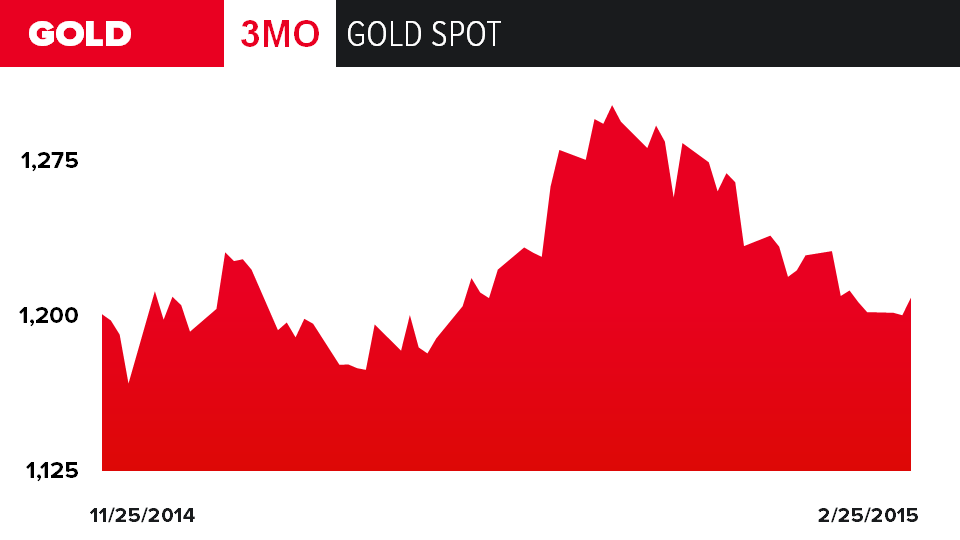

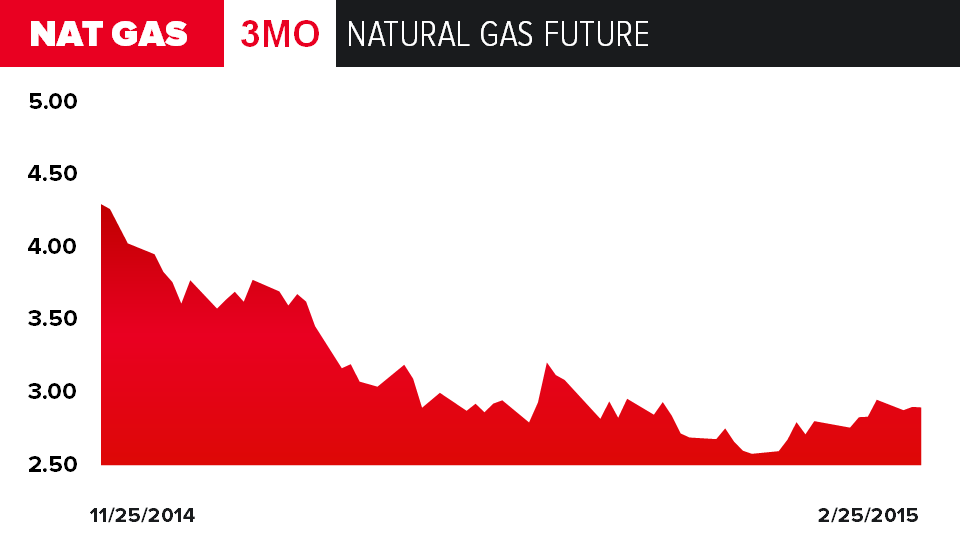

BEARISH TRENDS

CLICK HERE for a free look at Hedgeye's Morning Macro Call for institutional subscribers. Post your questions for Keith and hear him answer live on the air.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.