The short side of our Investment Ideas list is beginning to grow, despite strong industry sales trends. If there is anything CAKE, PNRA, or NDLS has taught us recently, it is that struggling business models are not participating in what is oft-referred to as the “industry-wide” sales strength. Alas, a rising tide cannot lift sinking boats. DFRG is a name that we see approximately 27-48% downside in over the next twelve months, given our $10-14 fair value range.

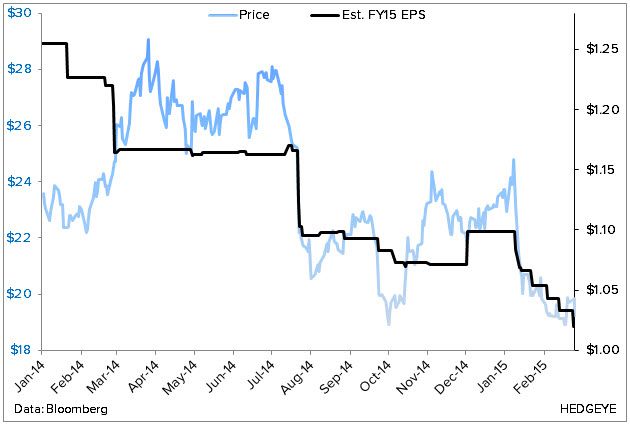

DFRG is a company we referred to last June as “the darling of Wall Street,” when we first tagged it as a short. Since that time, the stock has had a tremendous amount of difficulty staying afloat, as management’s growth vehicle consistently defied aggressive expectations. To wit, fiscal year ‘14 earnings estimates have declined more than 20% since January 2014. Over this same period, fiscal year ’15 earnings estimates have declined more than 23%. Despite these moves, we believe there are incremental negative revisions on tap.

The Bear Case

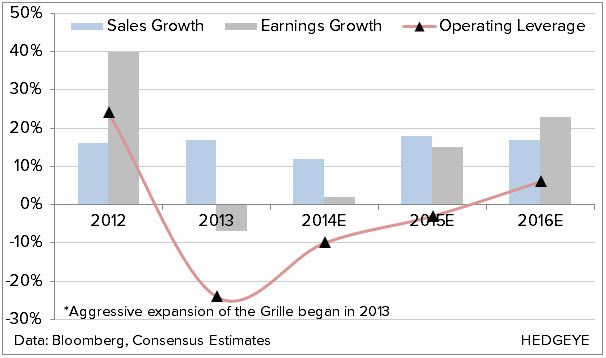

While we believe DFRG will miss estimates when they report 4Q14 earnings on 2/27, this is not solely a call on the quarter. 2014 was a year of pain for DFRG holders and we have little reason to believe 2015 will be any different. The street is looking for 15% and 23% earnings growth, respectively, in 2015 and 2016 after two consecutive years of down-to-flat growth. The leverage assumed in the operating model will prove more wishful than realistic.

To get at the heart of the matter, we have little confidence in the Grille as the company’s only growth vehicle. This concept is proving much harder to grow than most anticipated. The classes of 2012 and 2013 openings have been extremely disappointing; with restaurant level EBITDA in the 10-15% range, well below the 20-25% benchmark. Only the class of 2011, which was only 2 restaurants, has achieved restaurant level EBITDA in this range. This leads us to believe that 1) management is having a difficult time selecting quality sites 2) management’s targeted restaurant level EBITDA range is far too aggressive 3) the Grille shouldn’t be growing by 35-45% a year and 4) it is dilutive to the entire portfolio (leading to lower margins and returns).

Source: Company Filings

Our lack of confidence in the Grille, based solely on reported results, drives our distaste for the stock. Management has successfully framed DFRG as a growth company, but the new unit returns are falling well short of estimates and, if this aggressive new unit agenda continues, will lead to more destruction of shareholder value. The street is currently looking for seven new unit openings in 2015, a number we believe is at risk of being scaled back at some point throughout the year – keep in mind that management guided to 6-8 (one Double Eagle and 6-7 Grille’s). Sullivan’s will not be growing anytime soon; right now, it’s a dead concept walking.

Tough Setup into the 4Q14 Print

- Consensus is looking for an 80 bps sequential improvement in the two-year average of system-wide comps to +2.6%.

- Consensus is looking for 13% EPS growth in 4Q14, after -5%, 0%, and -20% growth in 1Q14-3Q14, respectively.

- Consensus is looking for cost of sales as a percentage of revenues of 30.24% in 4Q14, implying full-year cost of sales of 30.17%. Management guided this line to 30.1-30.4% of sales, suggesting estimates may be too aggressive at the low end of the range.

- Consensus is looking for 29 bps of labor leverage in 4Q14; management has only levered this line once on the past 12 quarters (20 bps of leverage in 2Q14).

- Consensus is looking for 29 bps of restaurant level margin leverage in 4Q14; management has only levered this line once in the past 12 quarters (9 bps of leverage in 2Q14).

- Consensus is looking for 23 bps of operating margin leverage in 4Q14; management has only levered this line twice in the past 12 quarters (301 bps of leverage in 1Q12; 354 bps of leverage in 2Q12).

- Guidance will likely be unfavorable.

Source: Company Filings, Consensus Metrix

Valuation and Sentiment

DFRG currently trades at 21x an (in our view) inflated next twelve months earnings estimate. Neither the sell-side, nor the buy-side, shares our sentiment on the stock, which has a 100% buy rating and only 3.26% short interest.

Source: FactSet