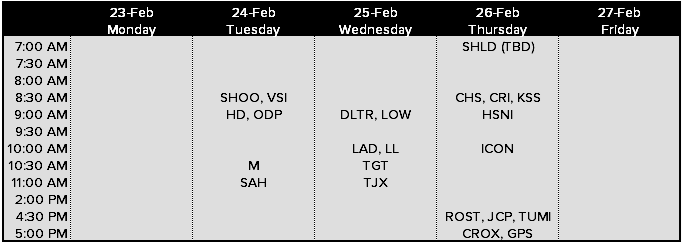

EVENTS TO WATCH

COMPANY HIGHLIGHTS

KSS Callout

Takeaway: DDS put up a very good 4Q, leveraging a 3% comp into 17% EPS growth. This should help put the 3.7% KSS comp into perspective. Since KSS released its sales results for the quarter, we've been barraged with concerns that the company's new strategies like Beauty, National Brands, and new Rewards program will create a 1-2 year period where KSS meaningfully outperforms the group. We simply don't think that's true. We think the results from DDS, and what we saw over the holiday (and should see in upcoming EPS) from fellow mid-tier department stores like Belk and Bon-Ton will show that the lion's share of KSS' strength was definitely not company specific. It remains one of our top shorts, and we think that earnings are ultimately headed closer to $3.00, while the consensus (and current valuation) is eyeing something closer to $6.

ICSC RETAIL SALES (80 General Merchandise Stores)

Takeaway: As brutal as the weather was last year during the polar vortex, this year is not far behind. And it's gotten sequentially worse as the year has progressed which we think helps explain the 2yr trend in the ICSC numbers. It's still to early in this year's first fiscal quarter (3 weeks in) to make sweeping generalizations about impacts from weather, but to date it's been less than an easy compare.

OTHER NEWS

TGT - Report: Target expands app functionality

(http://www.chainstoreage.com/article/report-target-expands-app-functionality)

NKE, ZU - Converse Settles With H&M, Zulilys

BBY - Best Buy opening tech center in Seattle

(http://www.chainstoreage.com/article/best-buy-opening-tech-center-seattle)

AMZN - Amazon wears Prada

(http://www.chainstoreage.com/article/amazon-wears-prada)

GPS - Intermix Taps Former Saks Chief Merchant

APP - American Apparel Further Strengthens its Management Team

(http://investors.americanapparel.net/releasedetail.cfm?ReleaseID=897790)

URBN - Anthropologie expands in France

(http://www.fierceretail.com/story/anthropologie-expands-france/2015-02-23)