Recent Notes

02/17/15 Post-Presidents’ Day Mashup

02/18/15 NDLS: Going In Short

02/20/15 NDLS: Wet Noodles

Events This Week

Monday, February 23rd

- QSR at the JP Morgan High Yield & Leveraged Finance Conference 9:00am EST

- TXRH earnings call 5:00pm EST

Tuesday, February 24th

- DPZ earnings call 10:00am EST

- CBRL earnings call 11:00am EST

- KONA earnings call 4:30pm EST

- BBRG earnings call 5:00pm EST

Wednesday, February 25th

- PZZA earnings call 10:00am EST

- DIN earnings call 11:00am EST

Thursday, February 26th

- TAST earnings call 8:30am EST

- PLKI earnings call 9:00am EST

Friday, February 27th

- DFRG earnings call 8:30am EST

Commodities

Recent News Flow

This Morning

- DRI appointed current Interim CEO Gene Lee as permanent Chief Executive Officer, effective immediately. The company is now turning its attention to finding a replacement for CFO Brad Richmond, who plans to retire at the end of March. The board will consider both internal and external candidates.

Monday, February 16th

- RRGB expanded its finest premium burger line with its first seafood option – The Wild Pacific Crab Cake Burger. It is available while supplies last.

Wednesday, February 18th

- WEN announced a regular quarterly cash dividend of $0.055 per share available to shareholders of record as of March 2, 2015.

Friday, February 20th

- PLAY announced the full exercise of the underwriters’ option to purchase 990,000 shares of common stock in connection with the previously announced secondary public offering. Following the exercise of this option, Oak Hill Capital partners' stake will decrease to 62.1% of the outstanding shares of common stock.

Sector Performance

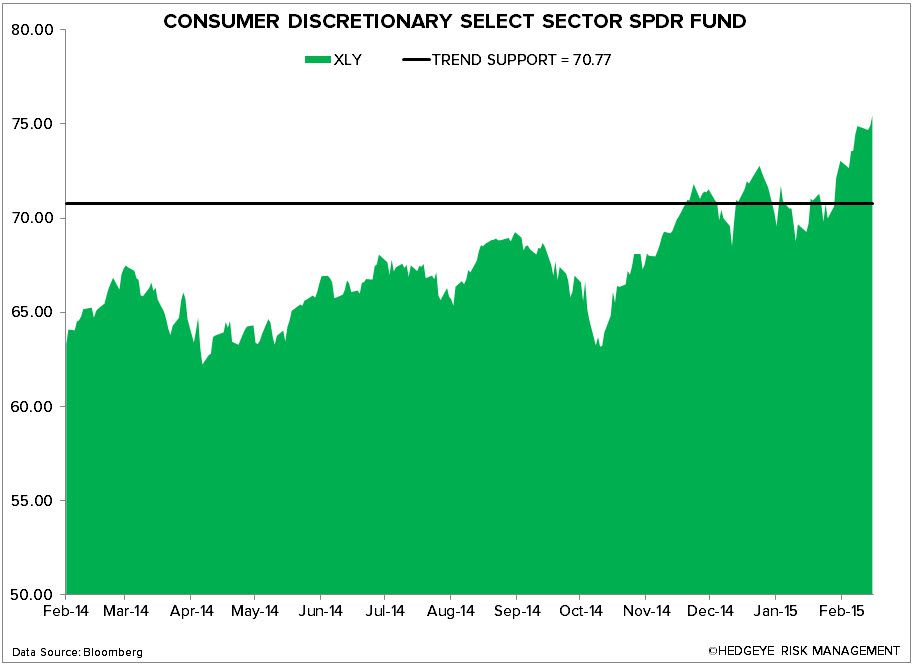

The XLY (+1.3%) outperformed the SPX (+1.0%) last week.

Quantitative Setup

From a quantitative prospective, the XLY remains bullish on an intermediate-term TREND duration.

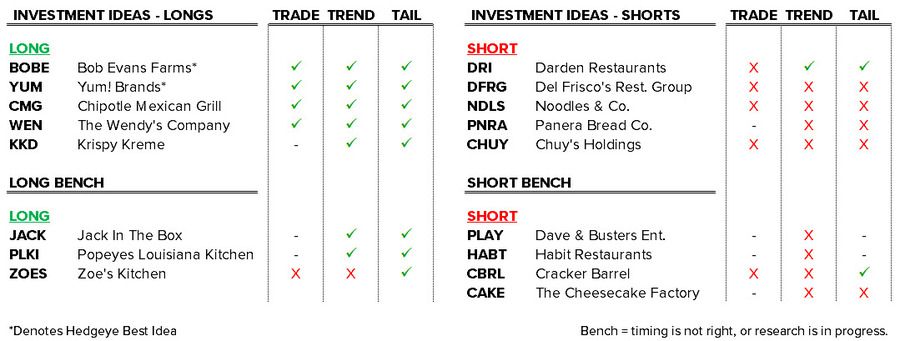

Casual Dining Restaurants

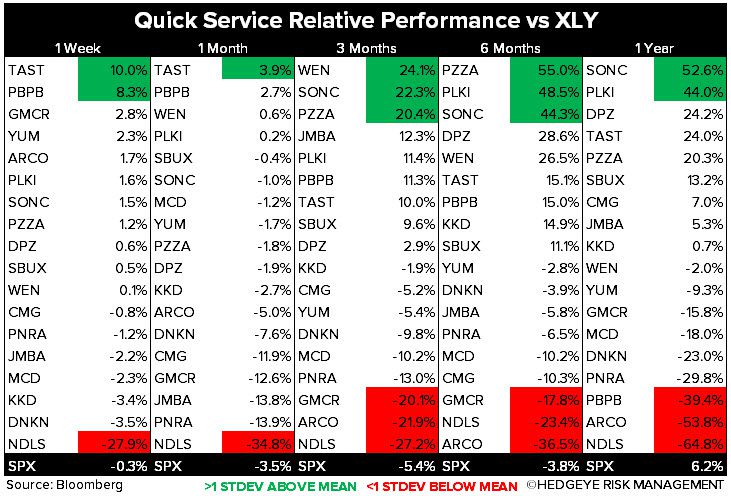

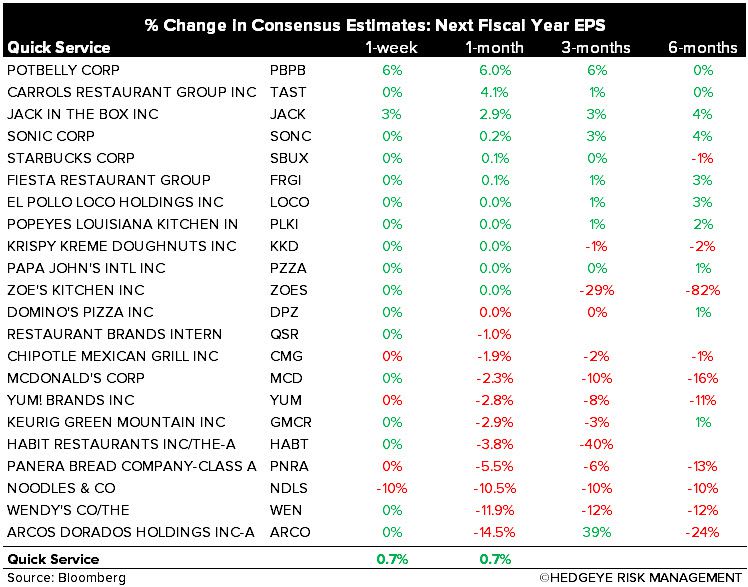

Quick Service Restaurants