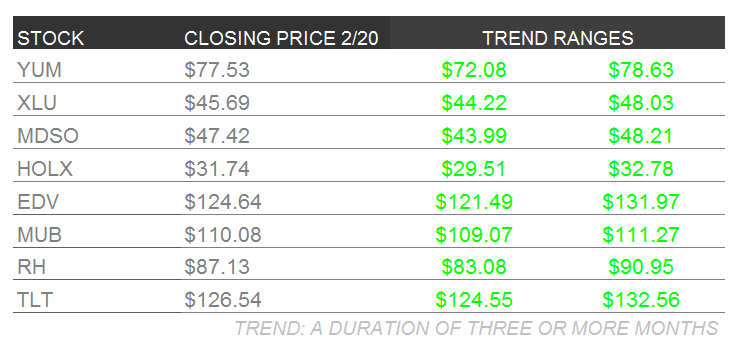

Below are Hedgeye analysts’ latest updates on our eight current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

We also feature two additional pieces of content at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

YUM

Shares of Yum! Brands are up ~7.5% over the past month and have plenty of room to run.

The street’s reset earnings estimates are calling for 12% EPS growth in ’15 after 4% EPS growth in ’14. China continues to be the wild card in the name, as a strong 2H15 would propel shares higher. Any negative development would be viewed quite unfavorably. If China recovers in ‘15, the stock will work. If China doesn’t recover, management will be forced to de-risk the business – an event that the public market would immediately reward. Remember, China has been a huge drag on the stock, making YUM a perennial underperformer over the past five years.

Here’s why it would make sense for management to de-risk the business from China:

- YUM China is worth approximately $49 per share to YUM

- YUM China represents a nasty mix for YUM – the business is under pressure and it makes up a significant part of YUM’s financial performance

- The board must do something to evolve the business model and reduce its exposure to China in a meaningful way

- The board can de-risk the business by selling off company-owned stores

- The board should focus on selling assets in Shanghai and Beijing; operating stores in these regions is equivalent to operating stores in Manhattan (who would want to do that?)

- It has recently been rumored that YUM is looking to sell its company-operated KFC business in India in order to avoid real estate costs that are corroding its profitability (why not in China?)

- The board should create a Yum China tracking stock; we suspect there would be significant demand for the largest consumer company in China

- Allowing the Chinese to own a part of KFC could help consumer perception of the brand and, ultimately, benefit same-store sales

- The Chinese government may put less pressure on the company if Chinese nationals own it (it certainly wouldn’t make the situation any worse)

YUM remains one of our favorite longs in space.

MDSO

Medidata Solutions is the eClinical market leader with an estimated 40% share. MDSO has been successful in gaining share due to a superior product offering and Oracle’s botched acquisition of Phase Forward (major competitor) in 2010. Those short the stock argue that Oracle is beginning to compete more effectively on price, and more broadly, that EDC is a commoditized business. However, anecdotes from the field suggest otherwise:

Clinical Trial Data Manager (Top CRO)

- “Oracle is so large and they lack customer focus and support. Medidata is more customer friendly”

- “It’s a 24-hour turnaround with Medidata, and with Phase Forward it is 48-72 hours”

- “[EDC] not viewed as a commodity, absolutely critical”

VP of Business Development (Major Competitor)

- “…Medidata has made it difficult for new entrants to come in. EDC market is still going to be relevant and is still growing”

- “Both Medidata and Oracle are taking an aggressive stance in Asia and trying to cement their share”

Former Medidata Salesperson

- Customer not price sensitive for EDC – “I don’t want the cheapest brain surgeon”

HOLX

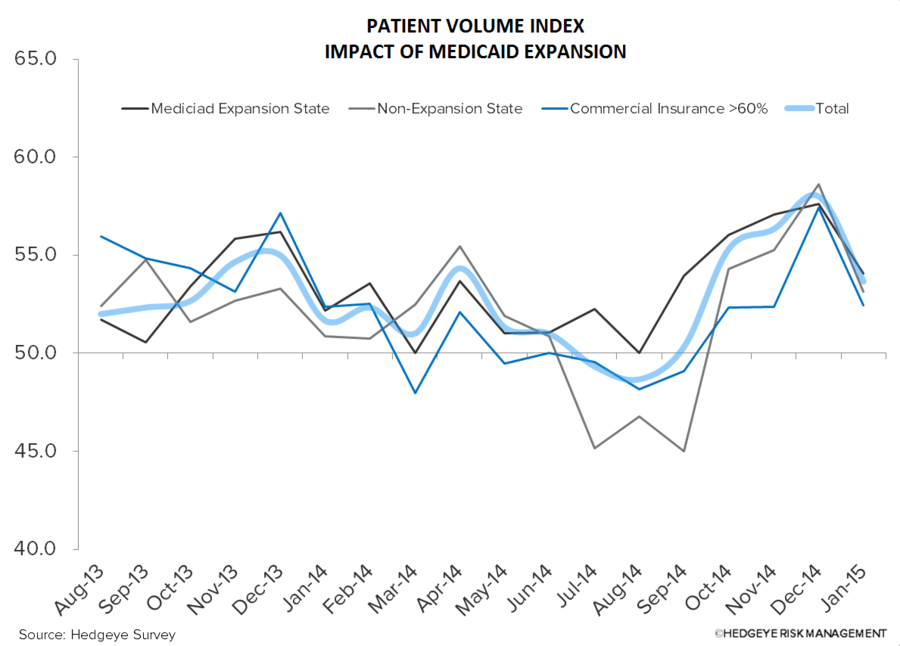

The U.S. Supreme Court will hear the case King v Burwell to decide the fate of of subsidies for individuals buying insurance through federally run exchanges. According to the Urban Institute, upwards of 10M people will lose their insurance, or a reduction of 69%, should SCOTUS rule that subsidies must flow through a state run exchange.

Hologic has certainly benefited from the ACA. The OB/GYN patient mix is primarily under the age of 65, commercially insured (70%), with a significant Medicaid population (15%), and lines up well with the ACA population. However, quantifying the impact is an indirect measure at best.

Using our survey data we compared the Patient Volume Index (>50 is expanding) across Medicaid expansion states, non-expansion states, and practices with a high percentage of commercially insured volume. Exchange based volume had a modest impact overall while the Medicaid expansion drove much of the patient volume benefit, particularly in the middle part of 2014.

Bottom line: Most of HOLX's benefit from the ACA has come through Medicaid expansion. SCOTUS can hurt, but impact looks modest.

TLT | EDV | XLU | MUB

In this granular, deep dive report written late last night, Hedgeye macro analyst Darius Dale details our intermediate-term scenario analysis for rates and rate-sensitive equities. We remain bullish despite rising volatility.

Click here to read the note in its entirety.

RH

The chart below shows Restoration Hardware's stock price and score on our sentiment monitor. Our sentiment monitor triangulates short interest, Sell Side ratings, and Insider activity. The lower the sentiment score, the more bullish it is for the stock, the higher the sentiment, the more bearish. Over the past few months, sentiment on RH has been treading water at or near all-time lows (which we think is extremely Bullish for the name).

We think that’s the case for a couple of reasons.

1) RH is a name that investors love to hate. Short interest as a percent of the float is sitting at 29%, off slightly from the 34% peaks heading into the 3Q print.

2) That would concern us if we didn’t see the type of raw earnings power locked in the model which will add 1mm sq. ft., $3bil in revenue, while taking margins from high single digits to the mid-teens. Add all that up and you get to $11 in earnings power.

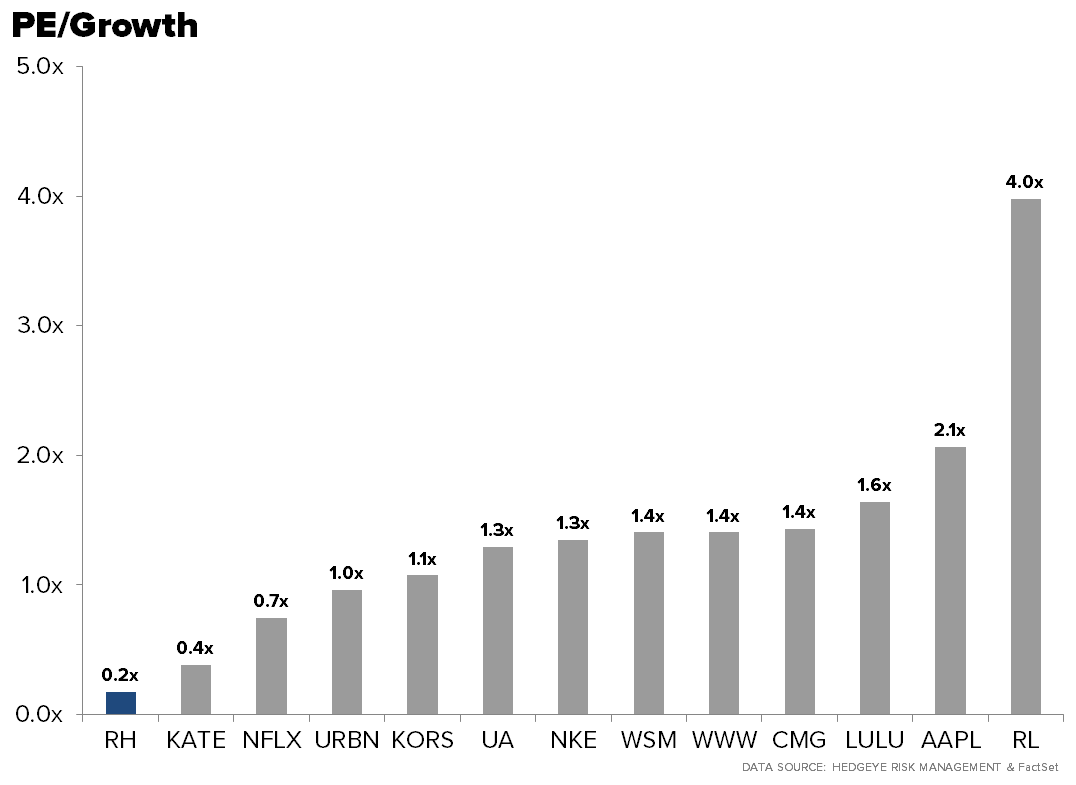

3) Valuation – The stock is currently trading at 24x our ’15 Earnings number and 28x the Consensus number. That may look expensive, but if we adjust it for growth it’s among the cheapest names in the consumer space.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

what are your competitors thinking?

Our macro team was on the road in sunny California earlier this week meeting with myriad funds. Here are the key notes from some of the key meetings (fund names removed).

cake: a troubled concept

Despite strong industry trends, restaurant stocks are not immune to looming cost pressures.