Below is the detailed breakdown of this morning's initial claims data from Joshua Steiner and the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

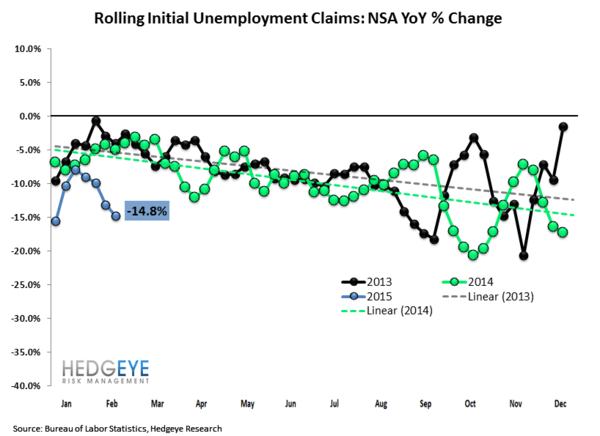

Last week's note (Initial Claims: Cognitive Dissonance & Mice) ran through both a high level and ground level overview of the labor market data. This week we'll keep it tight. After bouncing notably higher last week, claims retreated this week, dropping 21k to 283k. The four week moving average declined by a further 6k to 283k. The Y/Y rate of improvement in rolling NSA claims also accelerated. This week's numbers correspond to the sample period for the February jobs report and the M/M dynamic (4wk rolling) is lower by ~23k jobs vs the prior sampling period.

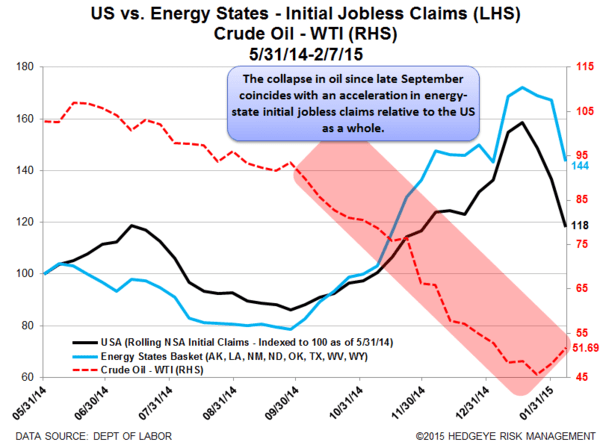

On the energy side, job losses eased slightly as the gap between our energy state basket and the US as a whole tightened in the most recent data. The gap between the two closed by 4 pts to 26 from 30.

Net net, the labor market data continues to hang in there, for now.

The Data

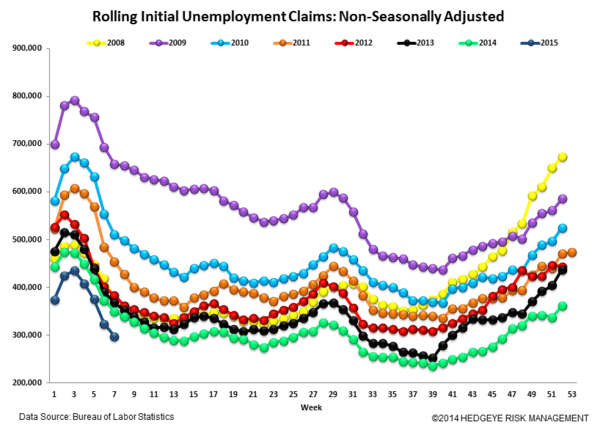

Prior to revision, initial jobless claims fell 21k to 283k from 304k WoW, as the prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -6.5k WoW to 283.25k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -14.8% lower YoY, which is a sequential improvement versus the previous week's YoY change of -13.1%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT