Editor’s note: This is a brief excerpt from Hedgeye morning research. Click here for more information on how you can become a subscriber.

* * * * * * *

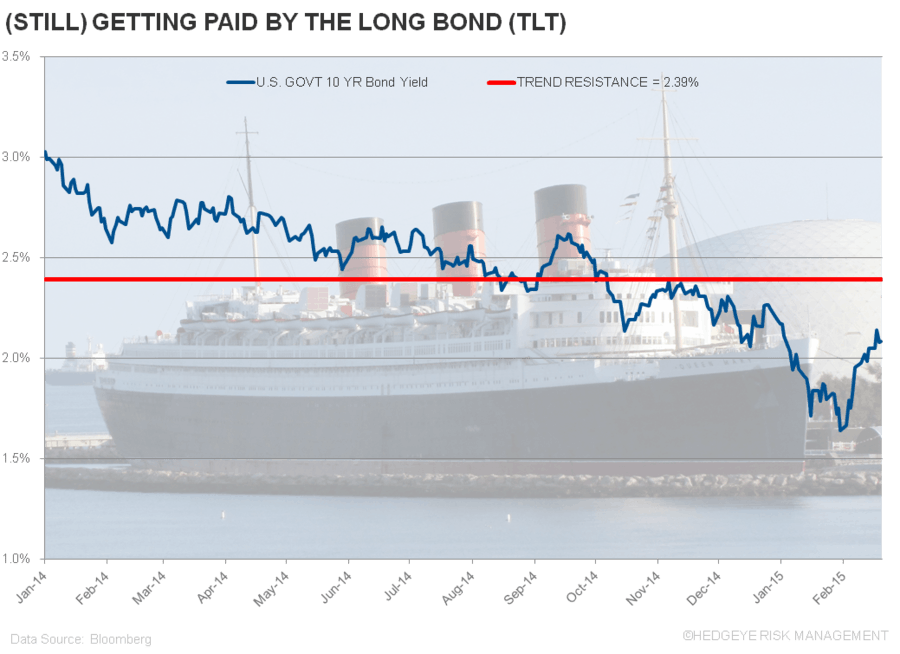

What a difference 24 hours in the bond market makes…

The 10-year Treasury yield drops -11 basis points in the last 24 hours from 2.16% to 2.05% after:

A) The data (PPI -0.8% vs consensus expecting ½ that decline) and

B) Fed Minutes effectively suggesting that a hike in June could be “premature” (Powell, a Fed voter, cautioned on the rising expectation of dropping the word “patient” too)

Expect volatility in the bond market to continue to rise.

Bottom line: The patient investor has bought every pullback in the Long Bond (TLT) for the last 8 months and has made plenty of money doing so.