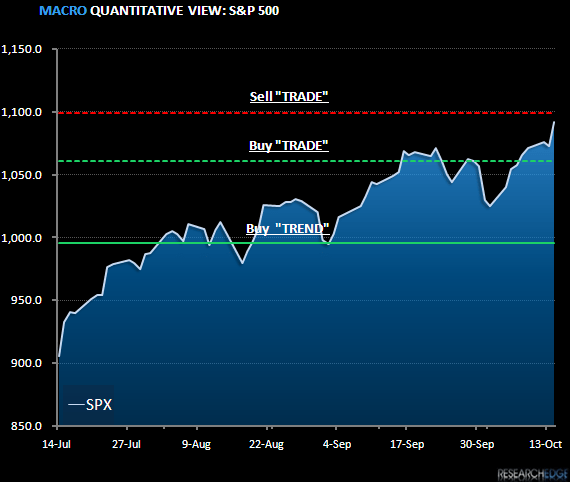

On Wednesday, the S&P 500 closed at 1,092, up 1.8% on the day. Yesterday was a melt up day for the S&P 500 on a big sequential acceleration in volume. This is bullish as trade and TRADE and TREND are positive. Of all the positive dynamics at work yesterday the earnings calendar seemed to take center stage, with JPM, INTC, ALTR and CSX leading the way with better than expected results.

The MACRO calendar also offered a positive tone to the market as retail sales fell 1.5% month-to-month in September vs consensus expectations for a 2.1% decline. The sequential decline is a function of the expiration of the cash-for-clunkers program, as sales at auto dealerships fell 10.4% month-to-month. Excluding autos, sales were up 0.5% vs consensus expectations for a 0.2% increases, while core retail sales - which excludes autos, gasoline and building materials - rose 0.5% last month following a 0.7% increase in August.

Yesterday’s portfolio activity included shorting CCL. Todd Jordan and Keith have been waiting, patiently, on price to re-short this levered name of over-capacity as we head into 2010's consumer spending headwinds. We also shorted NKE; Brian McGough and Keith will take the other side of today's bulled up GS call. For the immediate term TRADE, NKE is a short at this price.

Bell weather investment bank Goldman Sachs’ reported earnings this morning and metrics across the board were broadly better than expected. The stock in the pre-market is down just over three percent, which implies that the “whisper” expectations were higher than consensus estimates. This was to be expected give the massive move Goldman’s stock price in the year to date, and specifically over the last few months. Expectations, as always, are the root of all heartache as the futures and Goldman are now reflecting.

The momentum behind the “currency creditability crisis” continued to weigh on the dollar index, which fell for a third straight session, finishing down 0.7%. The VIX declined for the eighth straight day (0.6%) and is now down 43% year-to-date, which a more rational and tighter ranged market.

It’s being reported today by RealtyTrac that U.S. properties subject to foreclosure filings totaled nearly 938,000 in 3Q09, up 23% year-over-year and up 5% sequentially. Yesterday the FED released the details of the September meeting and the notes "expressed considerable uncertainty about the likely strength of the upturn in the economy once those stimulus supports were withdrawn or their effects waned." In particular, the housing “needs to get back on stronger footing for the national economy to return to full health.” The housing market has firmed up, helped by low mortgage rates and an $8,000 tax credit for first-time home buyers. The remaining question is the fate of the tax credit that is scheduled to expire at the end of November.

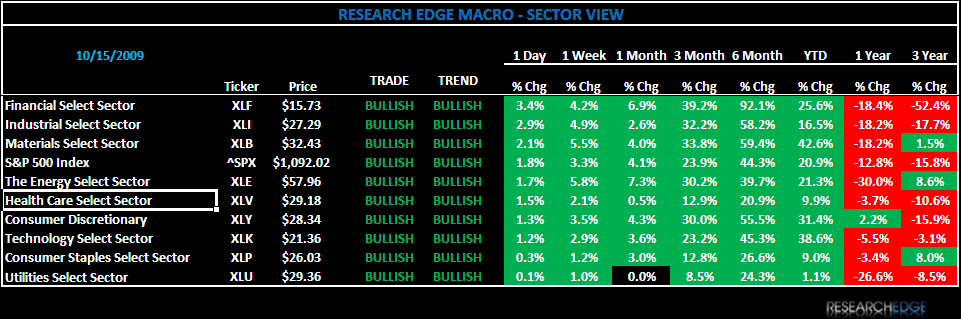

Yesterday, only three sectors outperformed the S&P 500. The three best performing sectors were Financials (XLF), Industrials and Materials (XLB), while Utilities (XLU), Consumer Staples (XLP) and Technology (XLK) were the bottom three.

Today, the set up for the S&P 500 is: TRADE (1,061) and TREND is positive (996). Day 4 of perfection - the Research Edge quantitative models have 9 of 9 sectors in the S&P500 positive on TREND and 9 of 9 sectors are positive from the TRADE duration.

The Research Edge Quant models have 1% upside and 3% downside in the S&P 500. At the time of writing the major market futures in the U.S. were trading down small on the back of Goldman Sachs’ earnings.

The Research Edge MACRO team.