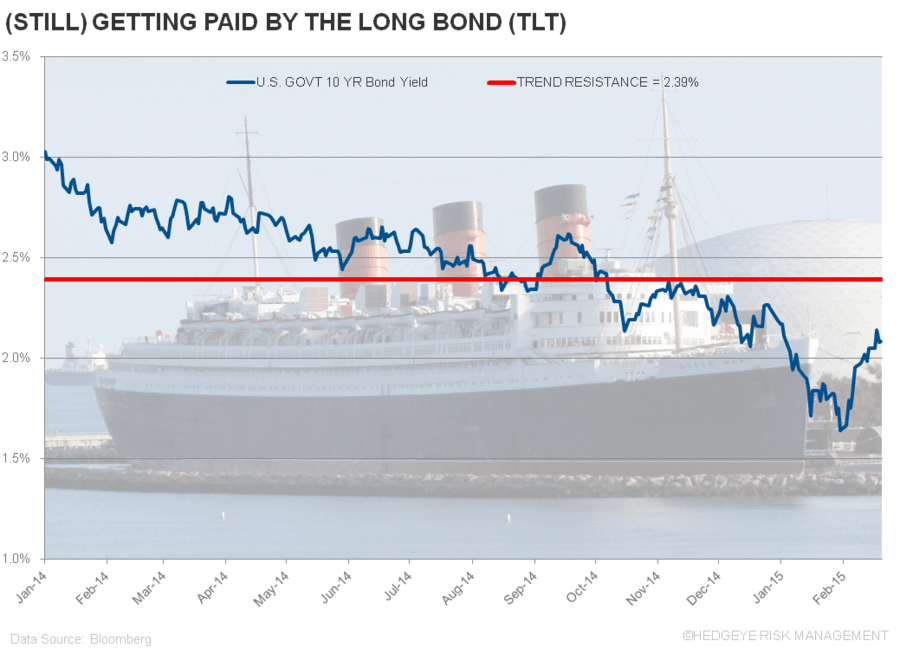

"FOMC voting member Jay Powell’s comment was a real-time one yesterday, whereas the Fed’s “Minutes” from their January meeting were not," Hedgeye CEO Keith McCullough wrote in today's Morning Newsletter. "That said, both helped drop the 10yr US Treasury Yield in a straight line from 2.16% 24 hours ago, to 2.05% this morning. The patient investor has bought every pullback in the Long Bond (TLT) for the last 8 months and made plenty of money doing so."