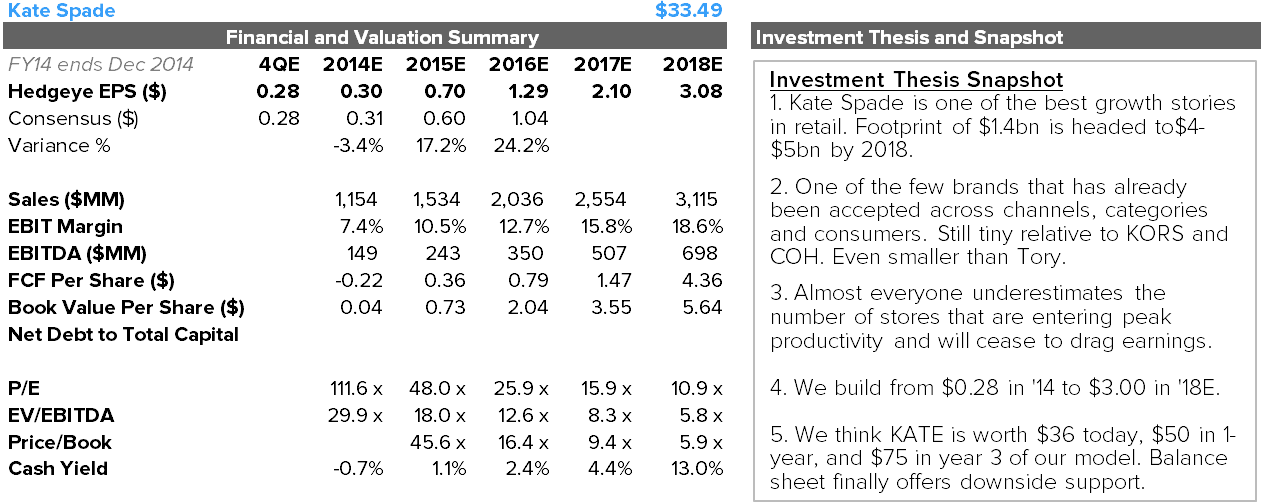

This announcement out of KATE that it is transitioning its watch business to FOSL is bigger than the headline otherwise suggests. We get to a dime accretion by year three for a company that will end up earning $0.30 in 2014, with an even greater impact on cash flow. Here are some key considerations.

1) As it stands today, KATE has about an $80-$100mm watch business, which is about 7% of KATE’s total business at retail ($1.35bn footprint – grossing up the value of wholesale and licenses). But by our estimate, the business is only marginally profitable, with EBIT of around $5mm, or around 3% of total. Accessories like watches should be 2-3x the margin rate of things like apparel, shoes and other core categories.

2) KATE was determined to develop its watch/jewelry business in house. That might work for a sub-$100mm brand, but without the scale of a larger design and sourcing operation it would likely stay a $100mm business forever. There is a reason why KORS, Tory Burch, Marc Jacobs, etc. all have deals in place with FOSL. If KATE wants to take the watch business closer to $500mm over time (no pun intended), which it does, then the deal with FOSL makes perfect sense.

3) Bye bye Adelington. We’ve been wondering for a while now why Adelington (its in-house private label jewelry design company for department stores) still exists as a part of Kate Spade. The brand itself is losing licenses left and right and is now margin dilutive. We can only think that it served some support function for Kate’s Jewelry/Watch design effort, but now that it’s moving over to FOSL we don’t see the need to keep it around. We have it coming off the P&L in our model by the end of 2016.

4) Over the past 3 years KORS watch/jewelry business has grown over 140% to $730mm as of the end of FY13. That’s huge. Let’s say KATE can grow 3x in 3 years. That means we take away about $100mm in consolidated revenue at about a 5% margin, or $5mm. Then in year 1 we take the business to $150mm at a 10% royalty – that’s $15mm at about a 60%margin (could be as high as 80%). That’s $9mm, which is about 80% growth in watch-related EBIT in year 1 – and that’s not to mention the fact that it takes working capital off the balance sheet. The net is $4mm, or about $0.02-$0.03 per share. That might not seem like a lot, but it’s actually about 10% earnings accretion in year 1.

5) In year 2, the math works out to be something like $225mm x 10% x 60% = $14mm, or $9mm net of lost consolidated sales. There’s an extra nickel in earnings. We’ll likely build closer to a dime by year 3.

6) Not only is KATE signing up for FOSL expertise and sourcing power, it will now be able to tap into the brands global supply network. In the past KATE had been signing distribution agreements ad-hoc region by region. This helps simplify that.

7) The only real issue we can think of would be KORS ties with FOSL. The brand currently accounts for about 25% of FOSL’s revenue. That’s the equivalent of UnderArmour starting up a line at a new shoe factory in Asia only to find out that the entire building is otherwise dominated by Nike. That said, KORS and FOSL just signed a 10yr deal which locks in the license through 2024. If KORS were going to have bargaining power it would have been a few months back. In addition, this is not FOSL’s first rodeo. It’s dealt with competition like this before. If it mismanages either of the two brands (KATE, most notably) it will shoot itself in the foot as it relates to reputational risk. FOSL management won’t let that happen.