Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

The main event remains Greece, where Greek bank swaps widened by 450-692 bps on the week and now stand at 1,416-2,274 bps. In other words, a high probability of Grexit has been priced in. Interestingly, unlike 2011, Europe doesn't really seem to care. The rest of Europe showed very little movement from sovereign to bank swaps and Euribor-OIS was essentially flat. The market seems to be saying that with EU GDP trending positively (+0.3% in 4Q14) and the ECB embarking on QE, Greece's fate just isn't that impactful for broader Europe

European Financial CDS - There's the rest of Europe, and then there's Greece. Greek banks continue to be priced for default as their swaps widened by 450-692 bps w/w and now higher by 966-1,581 bps m/m. Elsewhere in Europe, however, there was relatively little change as the median bank posted a 1 bps tightening w/w and is now 5 bps tighter m/m. Sberbank of Russia finally showed some signs of life, tightening by 47 bps w/w to 672 bps on the news of the Russian cease-fire.

Sovereign CDS – Despite modest growth in Eurozone GDP (+0.3% vs +0.2% Q/Q), sovereign swaps mostly widened over last week. Italian sovereign swaps widened by 17.5% (19 bps to 128) and Spanish sovereign swaps widened by 10.8% (+10 bps to 104).

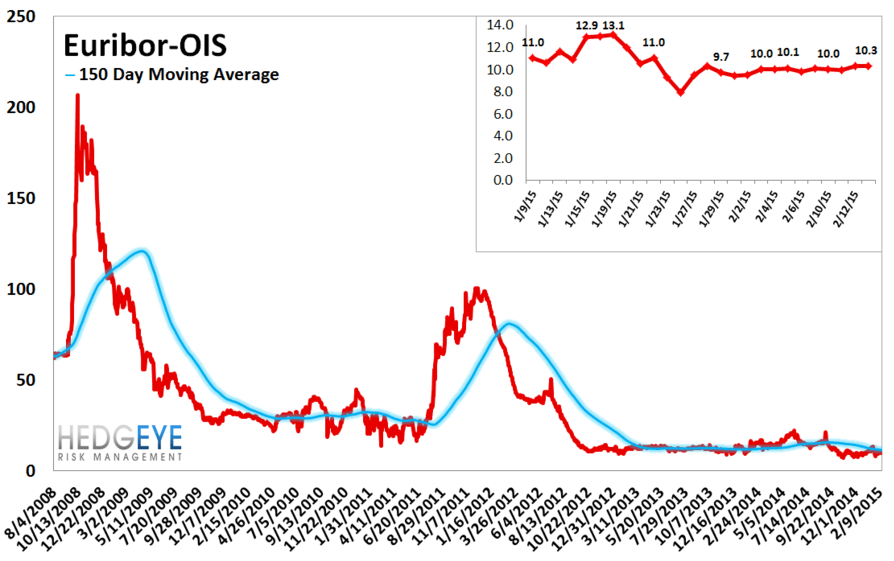

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 1 bps to 10 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst