KEY POINTS

- WHAT THE BULLS ARE BANKING ON: BABA will "close the gap" and mobile take-rates (Mobile Revenue as % of Mobile GMV) will rise to comparable desktop levels over time. That will be largely dependent on its Mobile Marketing revenue, which we believe is the most misunderstood part of the BABA story, and will be the focus of this note.

- WHY THAT WON'T HAPPEN: Mobile take-rates will be under pressure from secular pricing pressure in its Marketing segment. As more lower-income consumers join the BABA platform, vendors will experience worse ad conversion, and bid less for the ads they run on the mobile platforms. Since mobile is the low-cost device to internet access in China, this is where the pressure will occur. This is already happening today.

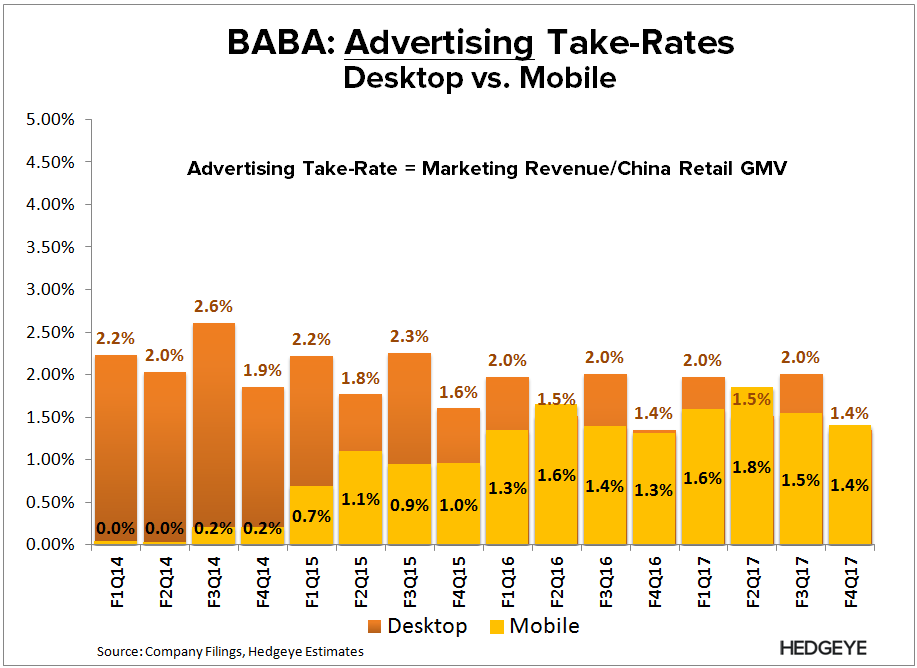

- THEN WHY ARE MOBILE AD TAKE-RATES RISING? BABA's reported metrics suggests the answer is traffic, specifically mix. We believe a higher percentage of traffic is moving over to mobile, so ad-click volume is rising there is well. The corresponding y/y decline in desktop take-rates would suggest as much.

- WHAT SHOULD WE EXPECT MOVING FORWARD? Mobile take-rates may plateau within the 1-2 years, and potentially decline thereafter. Mobile can only grow so much as a percentage of traffic, and mix is likely higher than BABA's reported metrics suggest. That means the trajectory of takes-rates will be dependent on user growth and ad pricing; two factors that are working against each other (see point 2).

WHAT THE BULLs ARE BANKING ON

BABA will "close the gap" and mobile take-rates (Mobile Revenue as % of Mobile GMV) will rise to comparable desktop levels over time. However it's important to note that Mobile Revenues are a function of Both Commissions & Marketing Revenue. We believe the latter is the most misunderstood part of the BABA story, and will be the focus of this note.

WHY THAT WON'T HAPPEN

Mobile take-rates will be under pressure from secular pricing pressure in its Marketing segment due to an influx of weaker consumers on to the BABA platform. That user growth will likely favor mobile as the low-cost device to internet access in China, so mobile is where we expect this secular pressure to occur.

In short, as more lower-income consumers join the BABA platform, vendors will experience progressively worse ad conversion, and bid less for the ads they run on the mobile platform. This has already happening today.

For more detail, see the note below

BABA: Model Facing Secular Pressure

12/04/14 09:17 AM EST

THEN WHY ARE MOBILE AD TAKE-RATES RISING?

We suspect the answer is traffic, specifically mix. Roughly 75% of BABA's marketing revenues are P4P (Pay for Performance), which require users to click the ads in order to generate revenue for BABA. We believe a higher percentage of traffic is moving over to mobile, so ad-click volume is rising there is well. The corresponding y/y decline in desktop ad take-rates would suggest as much.

The chart below also illustrates this dynamic, with Mobile MAUs (Monthly Active Users) rising as a percentage of Total Active Buyers (TTM metric). Naturally, this is an as an apple-to-oranges comparison; however, mobile mix is likely higher than the below metrics suggest.

Mobile User Mix (quarterly calculation notes)

- Mobile MAUs: only includes mobile shoppers using BABA's app that made a purchase in the last month of the quarter. This metric doesn't include mobile web shoppers, and may not include any mobile shoppers from the prior two months of the quarter. So the numerator is likely understated.

- Total Active Buyers: BABA only provides active buyers on a TTM basis (not quarterly). So unless every one of its reported Active buyers made a purchase within the associated quarter, the denominator is likely overstated.

WHAT SHOULD WE EXPECT MOVING FORWARD?

Mobile ad take-rates may plateau within the next 1-2 years, and potentially decline thereafter. Mobile can only grow so much as a percentage of traffic, and BABA's actual mobile mix is likely much higher the 79% that we calculated above for F3Q15. There's no way of telling whether that's 80% or 90%, but what we do know is that it can't exceed 100%.

In essence mobile mix is already topping out, which means the trajectory of mobile ad takes-rates will become increasingly dependent on 1) user growth and 2) ad pricing: two factors that are working against each other. BABA's next consumer will always be weaker than the one that came before it, and ad conversion/ROI will continue to see growing pressure from a weaker consumer.

Note: We will be hosting a call outlining our Short thesis on BABA tomorrow at 1pm EST.

Hesham Shaaban, CFA