Editor's note: This is an excerpt from today's Morning Newsletter written by Hedgeye Director of Research Daryl Jones.

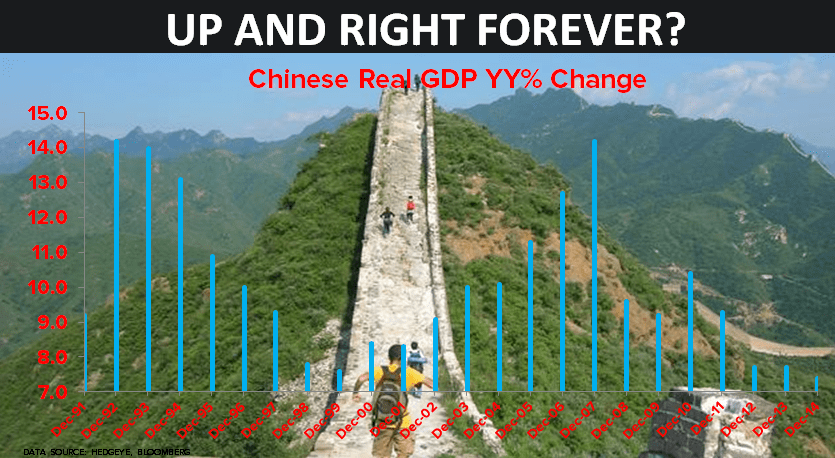

In the Chart of the Day, we show Chinese GDP growth going back 25 years. The clear takeaway from this chart is obviously that last year Chinese growth was at its lowest level in 24 years. In part, the government is actively trying to slow growth, so this makes sense. But even in a command economy like China, the ability of central bankers to manage a slow down in a perfectly orderly fashion is limited.