Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

Last week saw two notable events on the Macro risk front: 1) The ongoing game of bailout-chicken being played by Greece and the EU and 2) the labor market report on Friday. The favorable U.S. jobs report lifted domestic markets, as, apparently, good news has become good again. On the other hand, with the announcement that the ECB will stop accepting Greek bonds as collateral, spreads on EFG Eurobank Ergasias blew out by +626 bps. Interestingly, investors still perceive Greek risk as isolated to that country; European swaps at the median tightened by -2.6%.

European Financial CDS - Swaps mostly tightened in Europe last week. The big news for the week was that the ECB will stop accepting Greek bonds as collateral. Given that announcement, EFG Eugobank Ergasias swaps widened by a massive +626 bps.

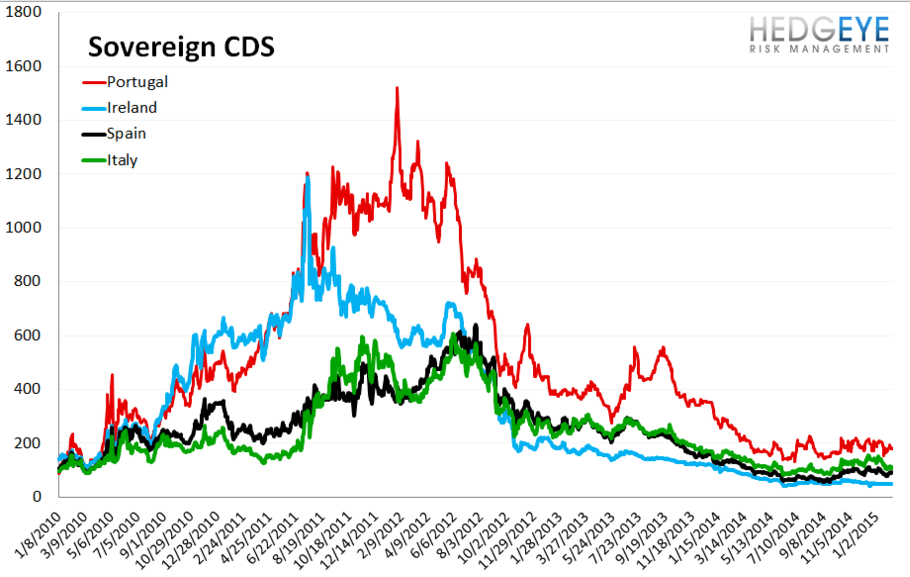

Sovereign CDS – Sovereign swaps were little changed on the week with the largest moves coming from Portugal (-4 bps to 180 ) and Spain (+7 bps to 94).

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 10 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst