When I was a kid, I used to play this game of chicken. Today, with the Dollar testing its YTD lows, it feels like the SP500 is playing the same…

The USD Index is down -0.29% at $75.90. The 2009 YTD low is 13 cents away from that print. Can the Burning Buck mark a lower-low as the SP500 tries its best to climb above its YTD closing high? That’s the game of chicken that the REFLATON trade wants to play.

In October of 2007 I wasn’t brave enough to stay in it on the long side until the bitter end. Thank God for that. Today, the risk management setup is far from similar, but it is October, and them chilly mornings can wake you up like they did with selloffs like we saw today.

I have only bought and covered positions today (bought Utilities (XLU); covered Darden (DRI). Since my 1054 line held, however low beta my buys may be, I’m definitely a better buyer on today’s weakness. Until this Buck stops Burning, the math will force us to play this US government sponsored game of chicken…

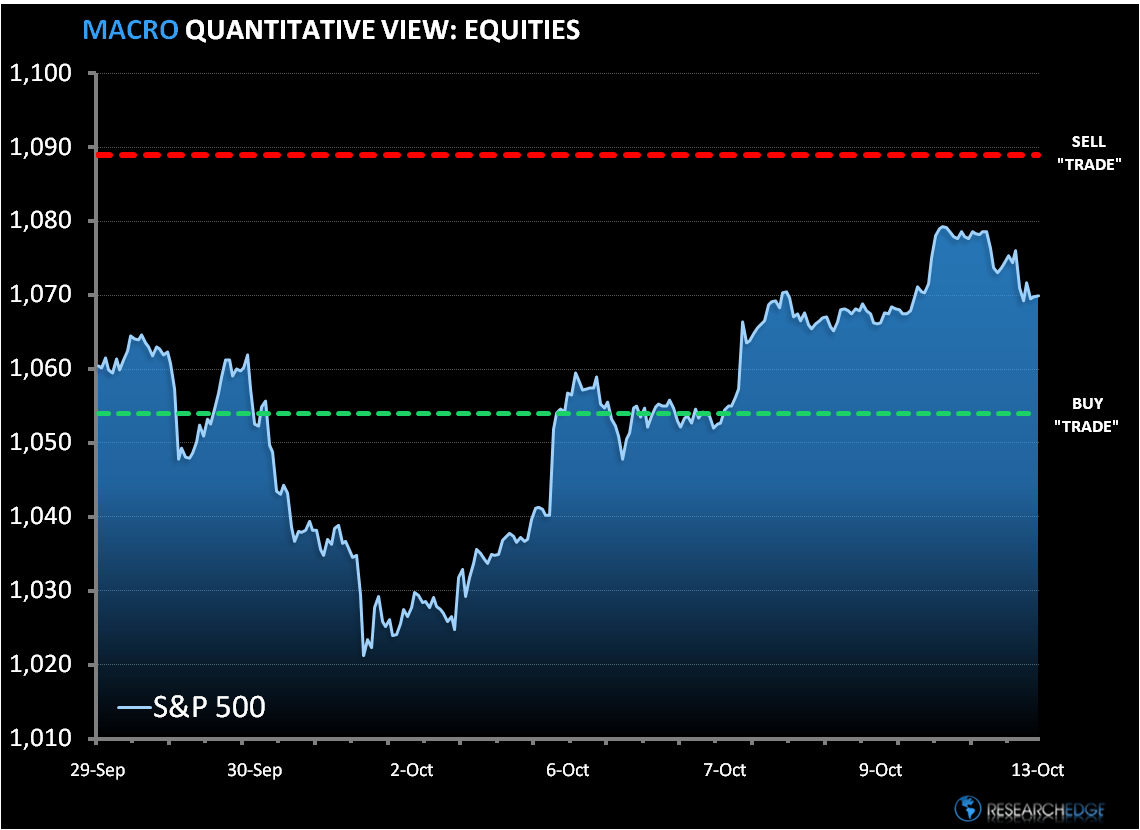

Today’s intraday US stock market recovery puts my refreshed TRADE lines of immediate term support/resistance at 1054 (dotted green) and 1089 (dotted red). In the Virtual Portfolio I now have 20 longs and 9 shorts.

KM

Keith R. McCullough

Chief Executive Officer