Employment data re-hashing is pretty much ubiquitous across the financial media and there’s little value-add in dog-piling on the data reporting so we’ll keep it tight here.

Immediately below is our summary review of the data followed by a few data points and trends we think are worth highlighting.

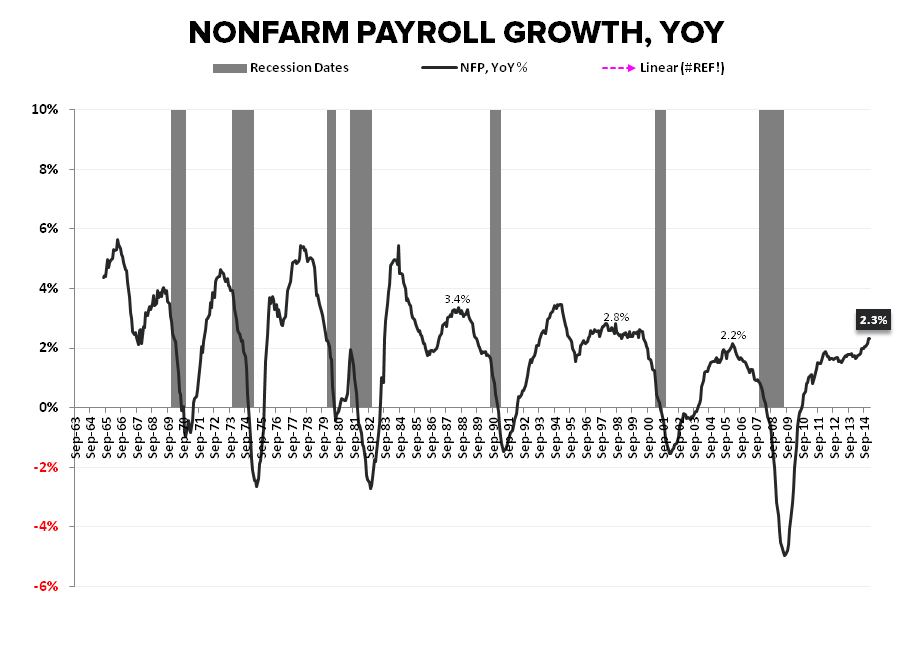

January Employment | Summary Review: Net Payrolls adds were strong on an absolute basis and accelerating on YoY basis, wage growth accelerated back up to +2.2%, hours worked held above trend, the positive balance of hiring at the sector/industry level continued, slack measure extended their slow march southward, revisions were unanimously positive and unemployment rose for the right reasons as participation bounced off multi-decade lows. Manufacturing and Energy employment showed little evidence of ROW demand and Oil-price pressures, respectively.

HOUSING: Residential Construction employment rose +13K MoM, marking the largest sequential rise since November of 2005. On a year-over-year basis, growth accelerated to +8.7% with the trend remaining one of ongoing improvement. After having been bearish on housing in 2014 through October, we continue to think housing outperforms over the intermediate term in 2015. (*Note: if you do not currently receive our housing sector research but would like access please let us know.)

Consumption/Income Growth: Today’s report augurs strength for the Consumption and Income/Spending data for January.

The math is straightforward: Accelerating employment base + an acceleration in wage growth will = accelerating aggregate income growth.

Even if a further increase in the savings rate mutes the translation to actual consumption growth (as it did in December), it’s hard to characterize accelerating income growth and rising savings as fundamentally negative.

Whether increased savings and rising corporate confidence actually translates into an acceleration in business investment – and a support to flagging productivity growth – remains a pretty big “if”, particularly as we traverse the late-cycle period of the current expansion.

Energy Related Employment: The BLS classifies oil & gas related employment within four major subsectors: Oil and Gas Extraction, Oil & Gas Pipeline Construction, Support Activities for Oil & Gas Operation and Mining/Oil/Gas field Machinery. The data is reported on a one month lag so the January release this morning provided December data for the respective industries.

In short, payroll employment directly tied to Oil & Gas extraction, while slowing, has yet to show a conspicuous decline.

We’ll be interest to see if that changes in the February report as the (more leading) initial jobless claims data continues to show a moderate negative divergence in energy state job separations.

Cycle Accounting | Best Before the Crest: It’s our view that we’re currently late-cycle in the current expansion. Employment and wage growth always look best before the crest and handicapping where we are on the slope of the cycle line remains the game.

With the incremental acceleration in employment growth in January, and inclusive of the 2014 revisions, we have now eclipsed the peak rate of payroll growth observed in the last cycle. Whether January represented the trough in Initial Claims (3-mo rolling ave basis) remains to be seen but historical cycle precedents suggest the clock tick starts to get louder following a negative inflection off peak improvement in initial claims

“Patience”: The “tough March decision for the Fed” headlines are in full crescendo this morning. For the sake of taking the other side of the strength in the employment report, the charts below are probably the ripest fodder for the “push out the dots” folks.

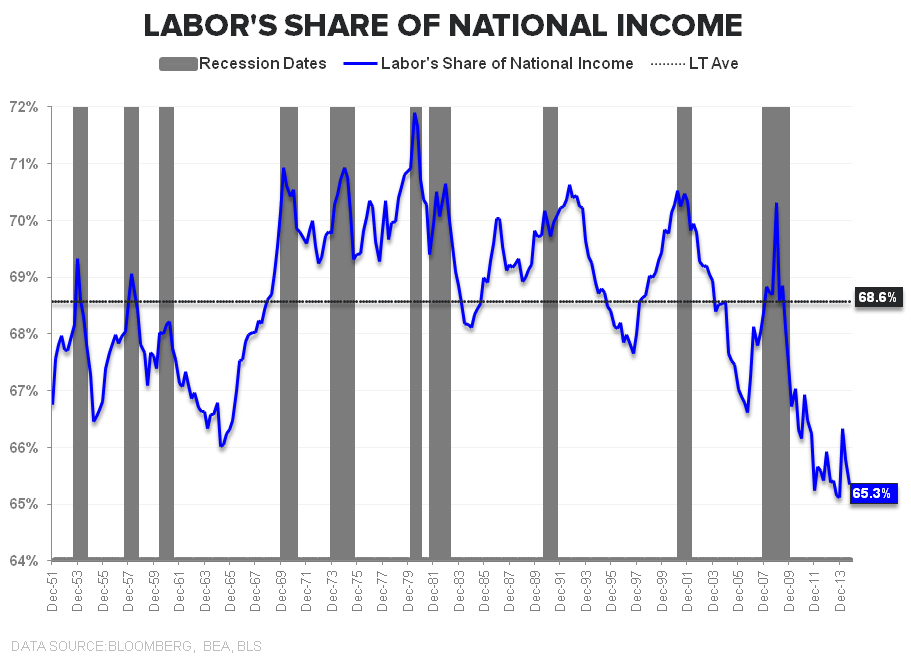

Is an acceleration in wage inflation imminent as slack continues its slow march southward, minimum wage changes take effect and net payroll add mix shifts modestly in favor of higher paying jobs? Perhaps, but that’s been the perennial panglossian talking point for at least the last 18 months. Elsewhere, the employment-to- population ratio, while improving, continues to signal ongoing slack while labor’s share of income remains decidedly depressed as the transmission of policy from financial asset inflation (wall street) to the real Main St. economy remains doggedly slow.

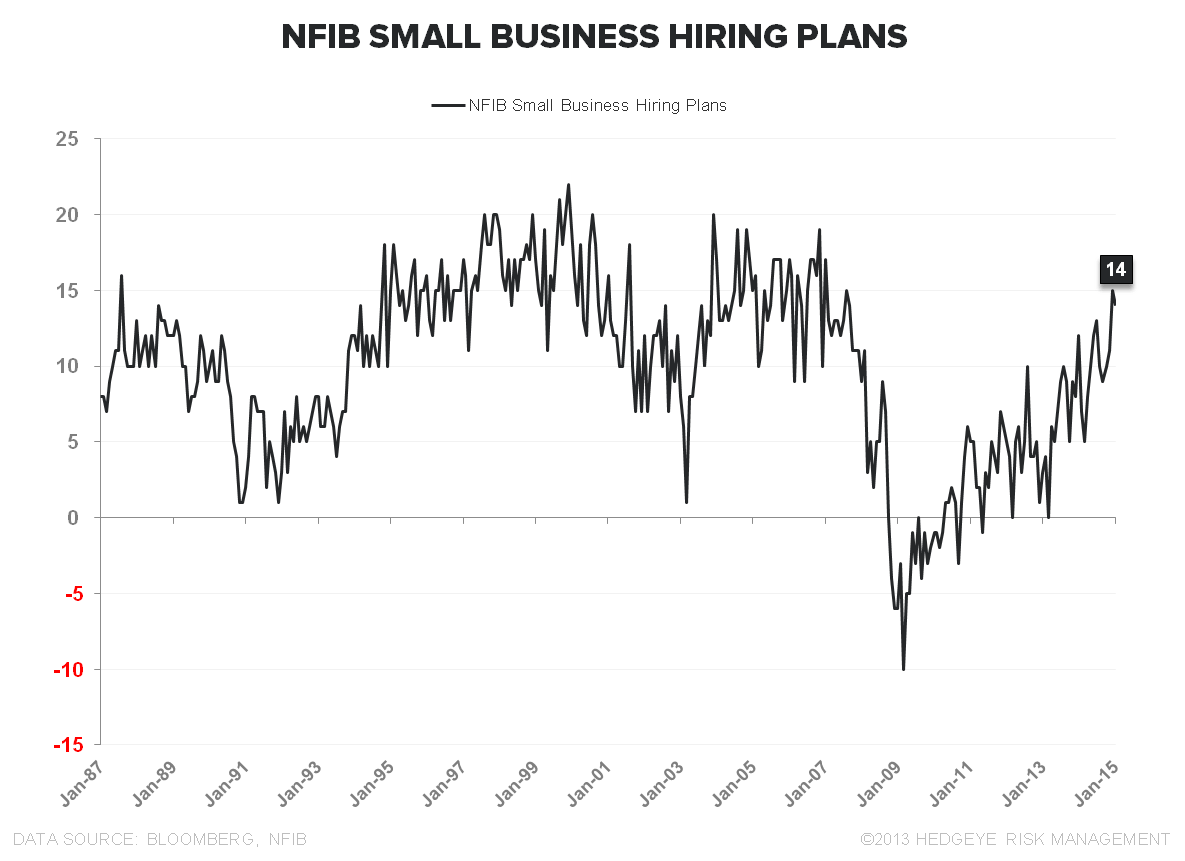

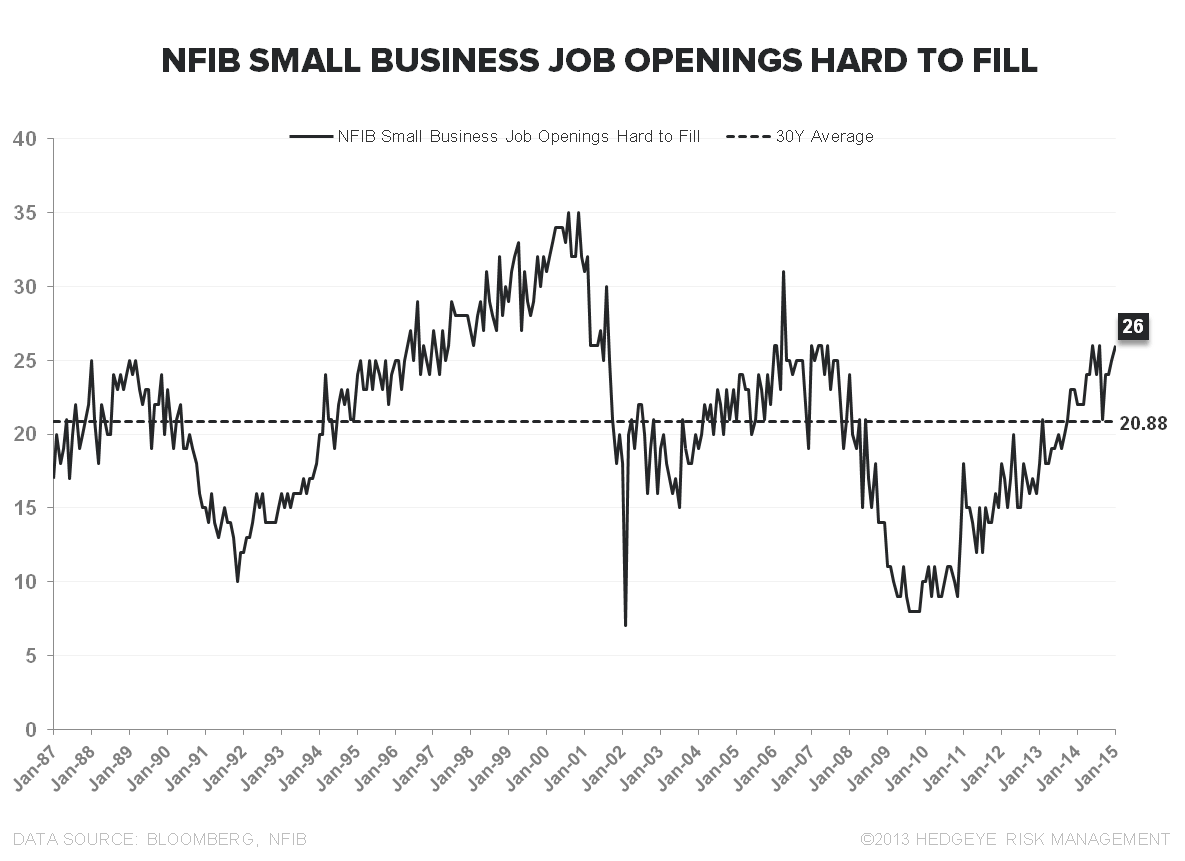

SLACK: The painstakingly sluggish trend towards labor market tautness remains ongoing. Below are the updated charts

Christian B. Drake

@HedgeyeUSA